2/4/2024

A good rally this week in cash which push the futures up a dollar. This is the first life we have really seen on the buy side in the last month. With cow numbers dropping and not very many replacements out there at some point there will be a sustained rally. The biggest question is when. Demand is still a little lack luster and interest rates are still high so there has not been much interest in taking on extra loads. If buyers foresee a 30 to 50 cent jump in the cheese price that may change. The question for producers, is this rally just another head fake that they should get some protection or should they sit back and let it go.

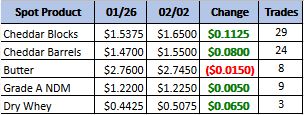

Weekly Spot Prices

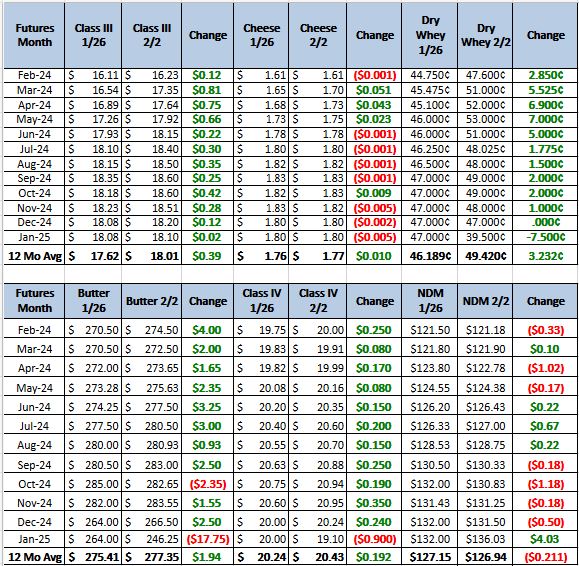

Weekly Future Prices

Cheese: Plant managers relay steady production schedules in the East. Some contacts reported overages for Class III spot milk loads. Cheese inventories are noted to be comfortable. Foodservice demand is seasonally strong. Retail demand is steady to stronger. Milk availability has tightened for cheese processors in the Midwest. Spot milk prices were reported at Class to $1 above Class III. Cheese plant managers relay active production schedules, with some reporting an extra day of manufacturing per week. Spot loads of cheese are available for purchasers. (USDA Cheese Highlights)

Butter: Retail demand varies from strong in the Western region to steady in the Central and Eastern regions. Food service demand is stronger throughout the country with minimal weather-related disruptions in the Pacific Northwest this week. Although stakeholders note slightly tighter cream volumes in a few parts of the nation, spot loads are readily available overall. Loads are moving into southern butter plants at multiples ranging from .90 to 1.10. Manufacturers relay steady to strong production schedules. However, some stakeholders indicate unsalted bulk butter loads are tighter. Bulk butter overages range from 1 to 8 cents above market, across all regions.(USDA Butter Highlights)

Dry Whey: Prices moved slightly higher on both ends of the range. Stakeholders note domestic demand as steady to lighter. Export demand is moderate. Although stakeholders indicate inventories are tighter, spot loads are available to meet immediate needs of most buyers. Cheese making is providing ample amounts of liquid whey for drying needs. Manufacturers relay mixed production paces. A few manufacturers note February production schedules are heavily focused on contractual obligations. (USDA Dry Whey)

That little bit of bullish sentiment from last week turned into a bullish rally this week. Looking at the day graph from March, class 3 futures rallied more the a dollar in the last 7 days. This broke our bearish trend that has been pushing the market sense the middle of October. Most producers need at-least $18 class 3 for a break even so if the market does not break into those ranges I expect the herd to continue to shrink. For anyone that does not have enough protection on; I would take this opportunity to buy some puts, as there is still plenty of cheese in the warehouses and demand does not seem to be tightening that up.