7/29/2022

Doom and gloom until Friday. This week we saw class 3 crash as September dipped below $20. As cash came down with the biggest drop on Thursday pushing blocks to a new low on the year at 1.85 and barrels to 1.8450. With cash now pricing in the low $19s and cost of production well over $20 in many parts of the country I do not think it will take long before we start to see more dairies close up shop.

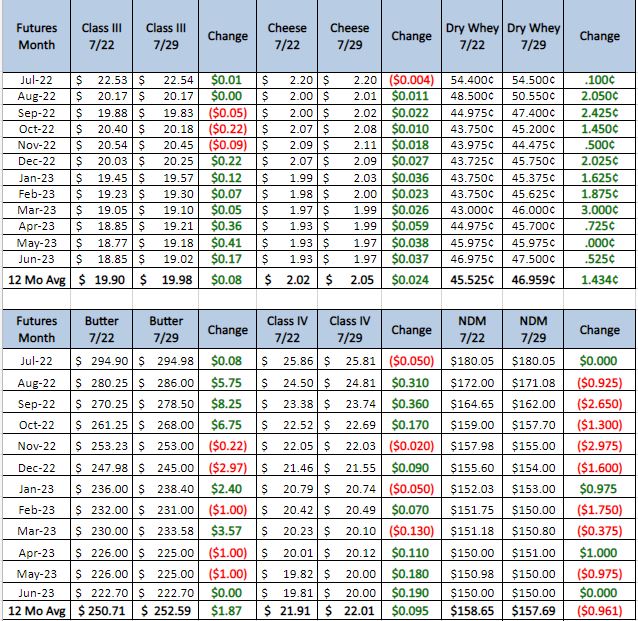

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk is available for active cheese production throughout the country. Some contacts in the Northeast and Midwest are wary of taking on additional milk loads and potentially building inventories. Retail demand for cheese continues to soften in the Northeast, as weaker consumer demand is causing some grocers to reduce cheese orders and/or limit the number of products offered. Food service demand is also declining in the Northeast; some restaurants in the region are reducing their menu offerings and limiting their operating hours. In the Midwest and West, domestic demand for cheese is steady this week. Some contacts in the West note that domestic sales are below forecasted levels and cite higher prices as contributing to reduced consumer purchasing. Contacts in the West say that international demand for cheese remains strong. Cheese inventories are available in both the Northeast and West. (USDA Cheese Highlights)

Butter: Cream availability is tightening throughout the country. Contacts in the West say milk output and cream production are decreasing due to seasonally higher temperatures in parts of the region. New butter production is limited in the Central region. In the Northeast and West regions, butter output is declining as labor shortages are curtailing some production facilities’ operating capacity. Butter inventories are tight in the Northeast and Central regions. Some Central region contacts say they are sourcing loads of butter from the West. Retail demand for butter is softening in all regions, and food service sales are slowing in the Northeast and West. Meanwhile, contacts in the Central region have reported a spike in food service sales this week. Stakeholders say bulk butter sales are strong in the West, as some purchasers are concerned that inventories will tighten in the coming months. Bulk butter overages range from 2 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry whey price range expanded as the bottom slid lower and the top moved higher this week. Meanwhile, the mostly price series for dry whey was unchanged. Demand for dry whey is steady in domestic markets. International demand for dry whey is lackluster as exports are down compared to 2021. Contacts report sales of dry whey to Asia remain below some expectations. Spot purchasers say dry whey inventories are available. Production of dry whey is steady, though plant managers continue to focus their schedules on the production of higher whey protein concentrates and permeate. Some regional drying operations are running lighter production schedules due to labor shortages and delayed deliveries of production supplies. (USDA Dry Whey updates)

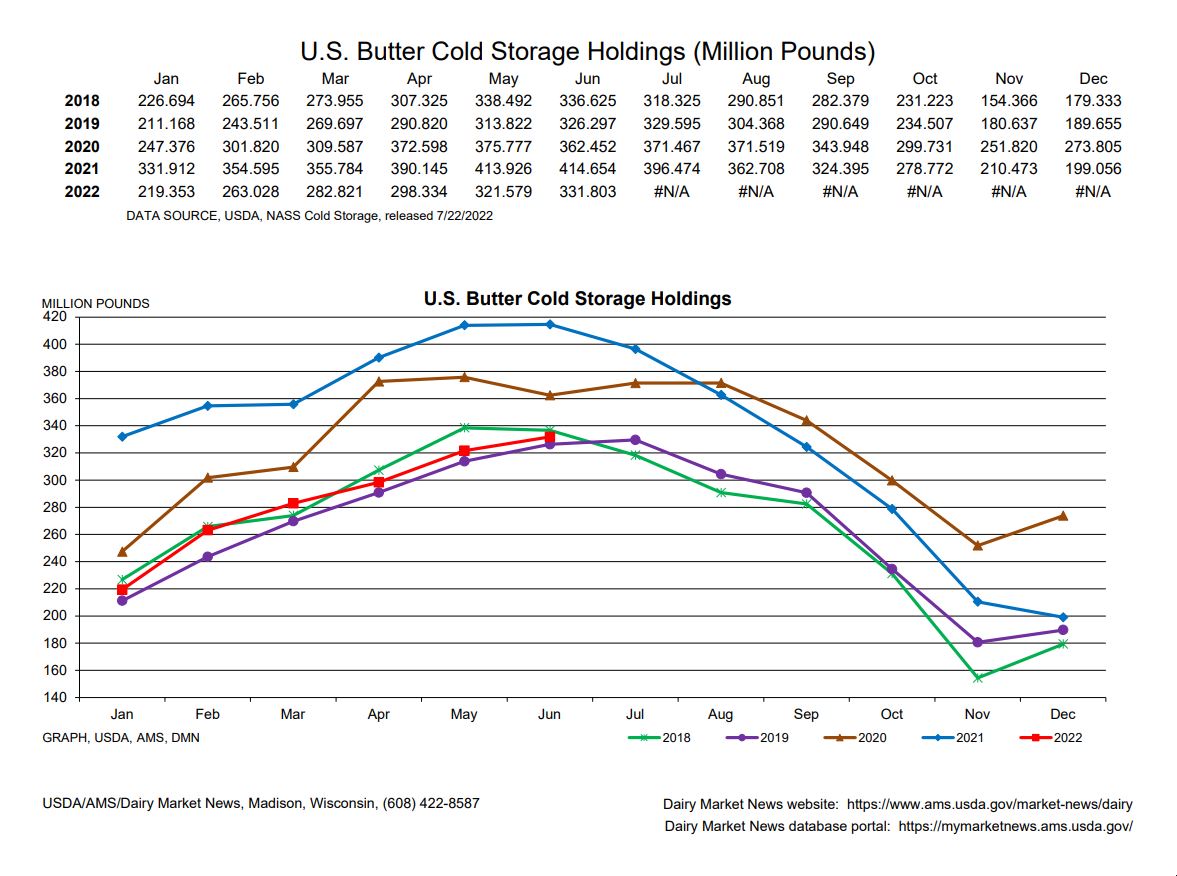

With class 3 dropping we are continuing to see good prices in class 4. So even though we see class 3 sliding below $20, class 4 is holding above $24. This should help some of the areas that took the biggest pull backs in cow numbers last year as these were generally butter powder heavy areas. As the graph above shows this has kept the Butter inventories near the 5 year low. This has kept the butter price hovering just under $3. On the NDPSR the drop on class 3 has not been as fast, and July is going to finish around $22.50. This is still a good number for most producers and I do not expect much change in cow numbers for July. With that said there could be another $1 to $2 drop, depending on demand. Recommendation, buy the 20.00 put sell the 22.00 call for an average of 30 cent through the end of the year.