7/24/2022

Big report week in dairy with both Milk Production and Cold Storage out this week. Unfortunately for producers both came out on the negative side for class 3 prices. Milk production was up 0.3 percent from last year after being down 0.6 percent last month. This is not all that surprising after milk prices surpassed prices form 2014 and put in the highest average prices ever for the first half of the year. Cold storage with up 5 percent from last year but down slightly form last month. This does mean that there is plenty of Cheese out there but it is not all that bearish in that we are using up a little more then we are making. With the draw down from last month. With both reports, production going up, and cold storage staying at a high level these reports are going to weigh heavy on the market.

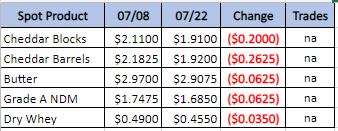

Weekly Spot Prices

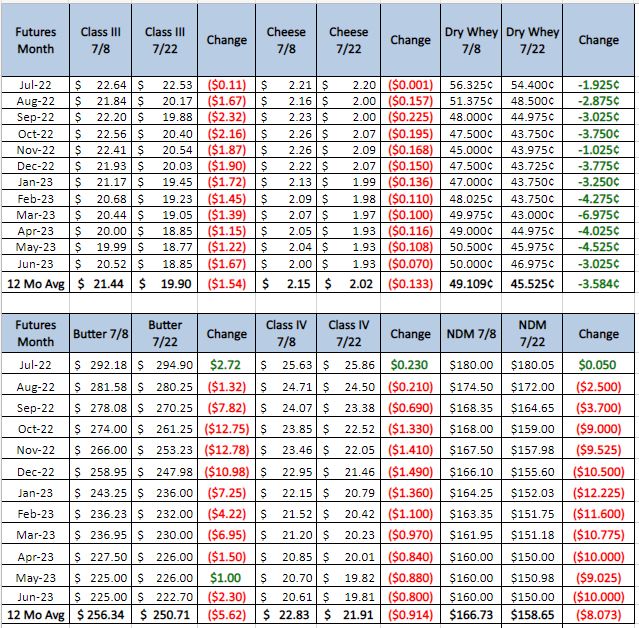

Weekly Future Prices

Cheese: Throughout the country, milk production is declining, but Class III milk remains available for cheesemaking. In the Central region, spot loads of Class III are being traded for as low as $4 under. In the Northeast and West regions, cheese production is steady. Meanwhile in the Midwest, plant updates/maintenance, along with employee and supply shortages, have contributed to some production setbacks. Cheese inventories are available in the Northeast and West, but curd and barrel inventories are tight in the Midwest. Some Northeastern contacts are, reportedly, concerned about supplies outpacing demand amid soft retail sales and steady to lower food service demand. In the Midwest, cheese sales are mixed, with contacts reporting seasonally quiet demand for American style cheese, but strong demand for barrels and curds. (USDA Cheese Highlights)

Butter: Cream is available in the Central region, though contacts report inventories are tightening in the Northeast and West. Butter and ice cream makers are keeping demand robust, in the West. Plant managers in the Central region say labor shortages may be a new normal. Some butter makers in the Northeast are running active schedules, while others are running below capacity due to labor shortages, high cream multiples, and softening domestic demand. Meanwhile, some contacts in the West say labor shortages are causing them to run below capacity. Butter inventories are tight in the Northeast. Inflationary pressures are affecting some grocery shoppers in the Northeast and West, who may be reducing their consumption or utilizing some butter alternatives. Demand for butter is seasonally steady in the Central region. Throughout this week, CME market prices for butter have been in the low to mid $2.90s. Bulk butter overages range from 2 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry whey prices moved lower after a steady previous week. End users are not in a rush to move on loads during a bearish cycle, as a majority of prices are trading hands below the $.50 mark. Some feed end users who opt for edible grade found some deals in the low/mid $.40s this week. Production, although not without delays, is busy with spot milk remaining at discounts week in, week out. Animal feed whey prices moved lower. Like with other dairy commodities, buyers are currently in the drivers’ seat. Market tones are bearish. (USDA Dry Whey updates)

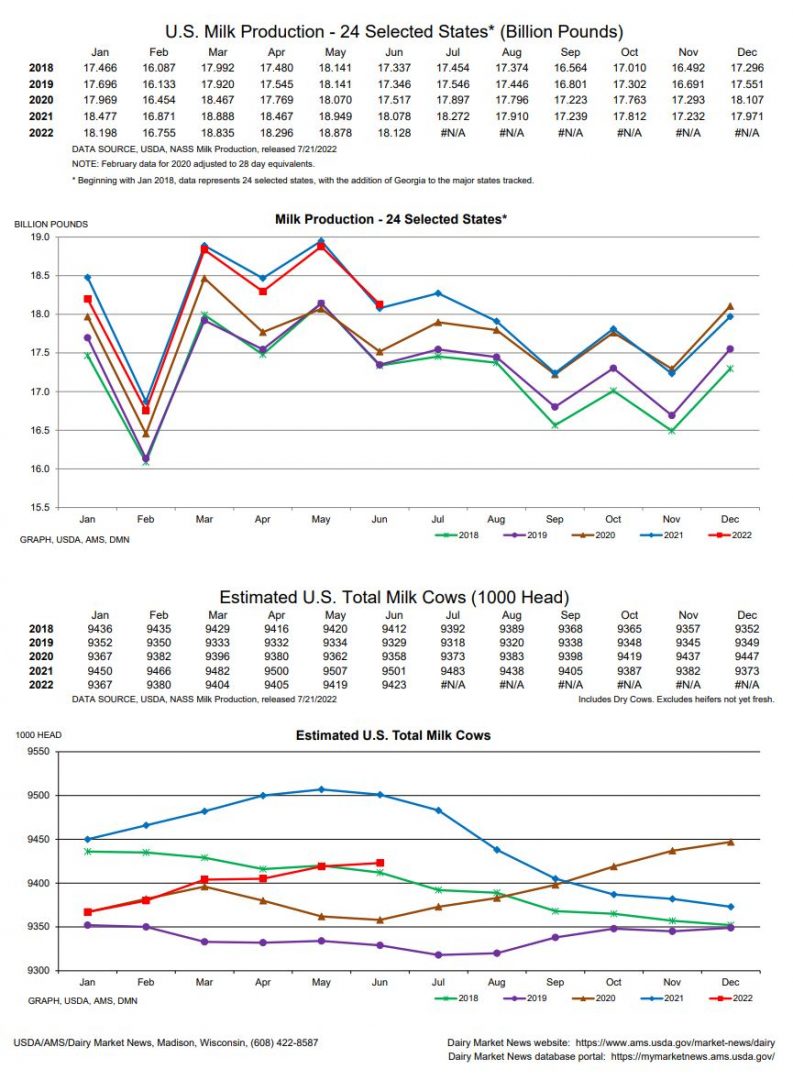

There are two graphs this week because there is an interesting comparison of number of cows to milk production. Every year farmers produce more milk per cow and you can see this pretty clearly from the comparison of 2021 and 2022. The milk production graph is relatively overlapped where the cow numbers are clearly lower in 2022. Which means unless there is a big drop in cow numbers, like there was in the second half of 2021, milk production is going to gap higher. This would push cow numbers below where they have been for the last 5 years. This is only half the story, as production may not matter if demand is good enough. Exports have been good, while domestic demand has slipped a little bit. As prices come down I would expect domestic demand to rebound. Recommendation by calls or call spreads to sell into on a rally.