8/27/2021

Milk production has come down slightly, cheese production still strong, and domestic and export demand is good. With futures moving down this week the class 3 market is still looking for a bottom.

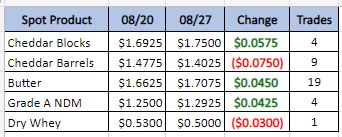

Spot Market Recap

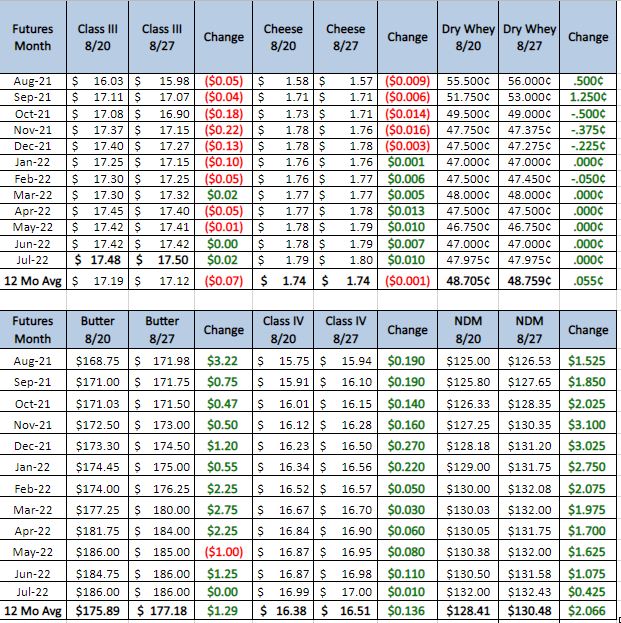

Futures Market Recap

Cheese market this week; spot milk availability has tightened up in the Midwest, but milk supplies on the East and West Coasts are steady. Trucker shortages have thrown a wrench in some manufacturers production schedules with slowing the transfer of milk from producer to plant. The Trucking shortage has also limited cheese sales and manufactures have had to employ other means to get there product to market. When possible rail cars have been used to clear warehouse space. Demand is steady in both the retail and food service market. Inventories have remained mostly steady week over week. Export interest is good but freight costs and hurdles at the Pacific ports have limited actual sales. The cheese market tone is mixed.

Butter: Cream availability has tightened. With the Western butter plants a little tighter then the central butter plants. Butter production has slowed in the east as trucking shortages have thrown off production schedules. Plants are getting yearly maintenance done with the down time. Inventories are healthy. Retail and food service demand are growing. Bulk butter prices ranged from 1 to 8 cents over class this week. Butter market tone is supported to a little bullish this week.

Dry whey prices slid this week. With producers looking to move whey loads below the 50 cent mark. End users are buying the dips but not will to pay more for spot loads. Trading has been active as more dry whey has become available. Demand is steady in both the domestic and international markets. Loads intended for export are facing delays at the ports and warehouse space is becoming limited. Dry whey production has been limited with labor shortages and plants are focusing on higher protein concentrates. The market tone is steady.

Grain Recommendation August 27 , 2021

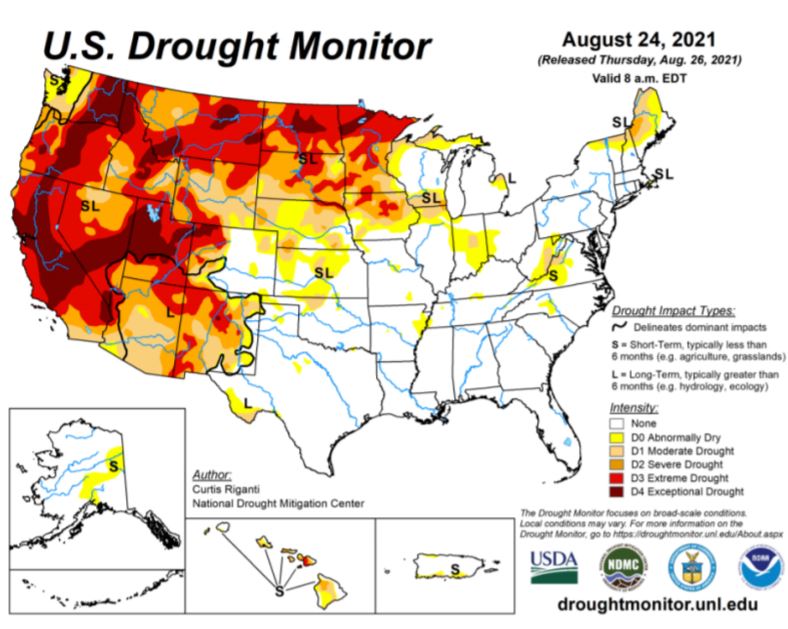

Long term weather forecasters are calling for a continuation of “The Drought years”. Our Fall weather predicts to be dry, this will keep soil moisture at lower levels, Wheat farmers usually soil test down to 4 feet to determine enough moisture to plant in August September, winter wheat crop. I don’t think they will take the risk unless we get some western states soakers soon. This all sets the stage for more volatility in the Grain markets. In normal years we see market lows in the August , September time period. Consider buying December 22 corn futures at 5.00 (currently trading at 5.16 ) Start with 25% of your corn needs for the dairy. Each contract is 135 tons of corn. Soybean Meal December 22 is trading at 347/ ton buy a at 342/ton (100 ton contracts).

The class 3 future have not quiet found their footing this week as the market moved lower again. I am still looking for a rally this fall as domestic and export interest is strong. This is all going to hinge on if the dairy products can get to where they and need. Shipping delays and port congestion are backing up product in warehouses. This is forcing manufactures to sell into markets where they can use alternative forms of transportation, such as rail cars. This concentration of product into a limited number of buyers has forced the prices lower. For some hedges in the last quarter of 2020 and the first quarter of 2021 look to buy some puts or put spreads. Buy 1650 put sell the 1550 put for a total 30 cents. Give us a call and we can tailor a hedge plan to your operation.