8/21/2021

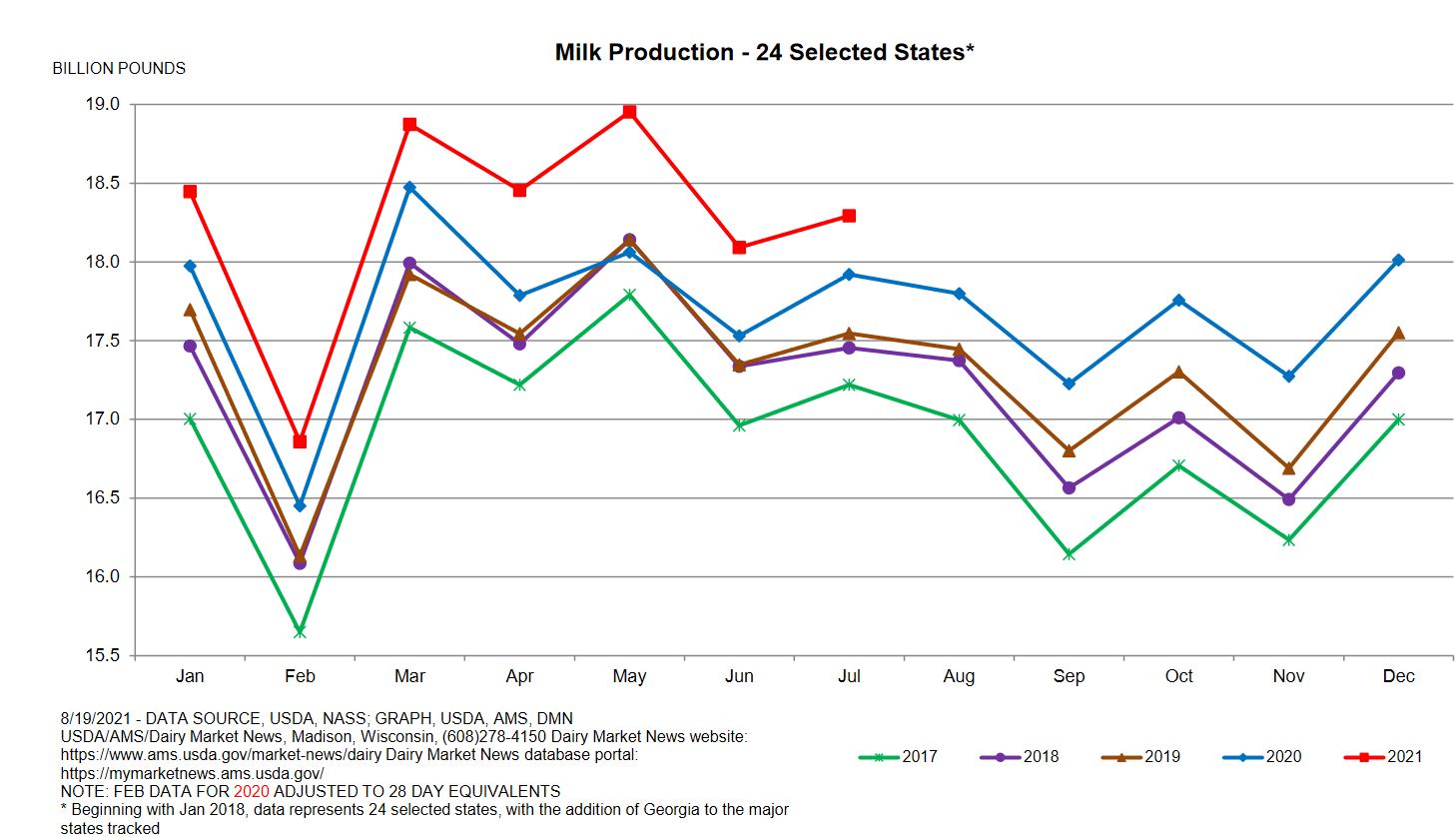

Milk production moved back slightly higher in July after the big drop in June, even though there was 3000 fewer cows than in June. Year over year milk production was up 2.0 percent. Cold storage will be out Monday and that will give us a good snapshot on how the supply versus demand is looking.

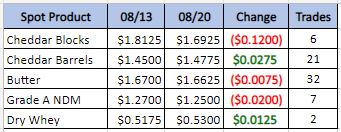

Spot Market Recap

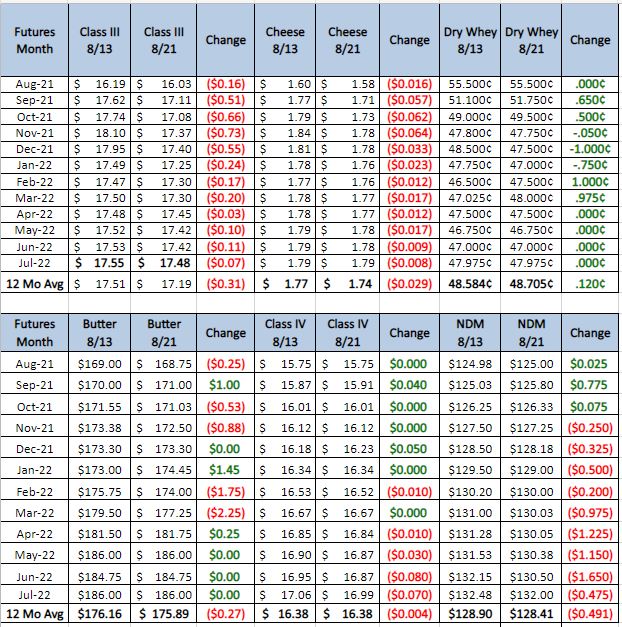

Futures Market Recap

Cheese Producers in the Northeast are running full production schedules with plenty of milk for manufacturing. Inventory levels are stable with good domestic demand. Food service orders are strong as restaurants continue to order cheese supplies to meet customer needs. Retail cheese orders are moderate for the summer season. In the Midwest cheese makers report strong sales. As milk supplies have tightened, cheese makers have turned to fortifying cheese vats with nonfat dry milk. Spot prices have gone from discount to class 3 to now slightly over. In the West both food service and retail demand have held steady. Export demand for cheese is strong, but loads intended for exports continue to face delays. There is a decline in milk production on the West coast but cheese makers report that there is still enough milk to run plants at full schedules. The overall cheese market tone is stable.

Butter: Cream availability varies as Eastern manufacturers are selling surplus cream. While Midwestern manufacturers report a supply tightness. In the West cream is available but trucking delay are causing problems. Food service orders are unchanged from last week and retail orders are steady. Inventories are reported to be in good shape heading into the fall. Excess bulk butter is selling for 2.5 to 8 cent above the market. Butter market tone is supported.

Dry whey: The prices have narrowed – some with the lows in the 50 cent range and the highs in the 60 cent range. End users are starting to take on extra loads heading into the fall. Inventory is available. Domestic demand has picked up some as export demand has soften. Dry whey market tone is stable.

A couple bumps in the road on this week. Even with milk production coming off compared to the first half of the year, cheese production has not slowed. There is good demand domestically but the market has not fixed the shipping problems which has left exports lack luster. There is still a good chance for a rally, but I would not sit on the fence too long for contracting for 2022. If the grain yields come out close to what Pro-farmer’s numbers are and China backs off their buying, gains could tumble. Lower feed costs more in line with the 10 year average would put many dairy farms cost of production bellow next years class 3 futures numbers. For the first half of next year I like buying the $1700 put and selling the $1900 call for somewhere in the 30 cent range. Make sure you have enough margin money to hold on. Give us a call and we can tailor a hedge plan to your operation.