03/20/2020

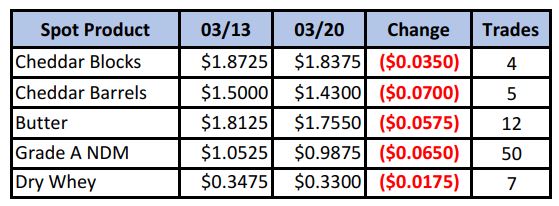

Mass school closings, social distancing and the dramatic reduction in the movement of people across the country were enough to accelerate another sell-off this week. Spot prices for all components were lower, with NDM crashing through the $1.00 level, into levels it has not seen since last March.

Spot Market Recap

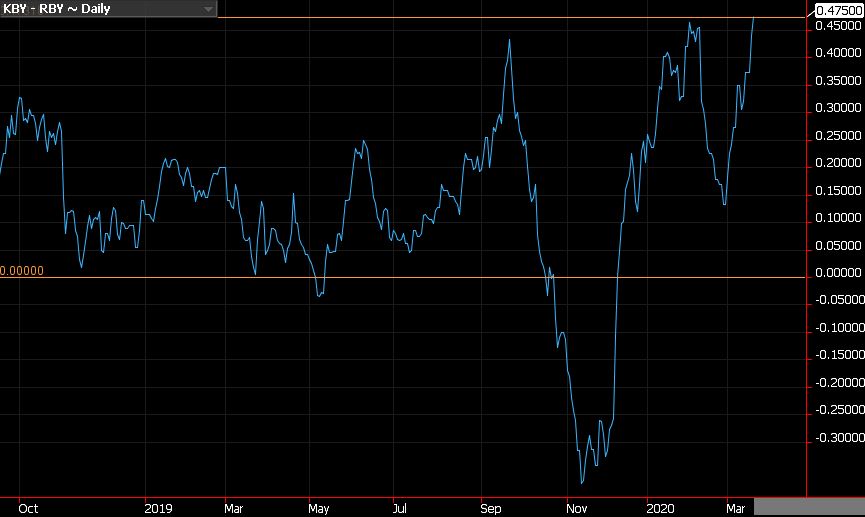

Meanwhile, the block/barrel spread reached a new record high on Thursday at 47½¢ before narrowing down to 40¾¢ on Friday.

Block/Barrel Spread

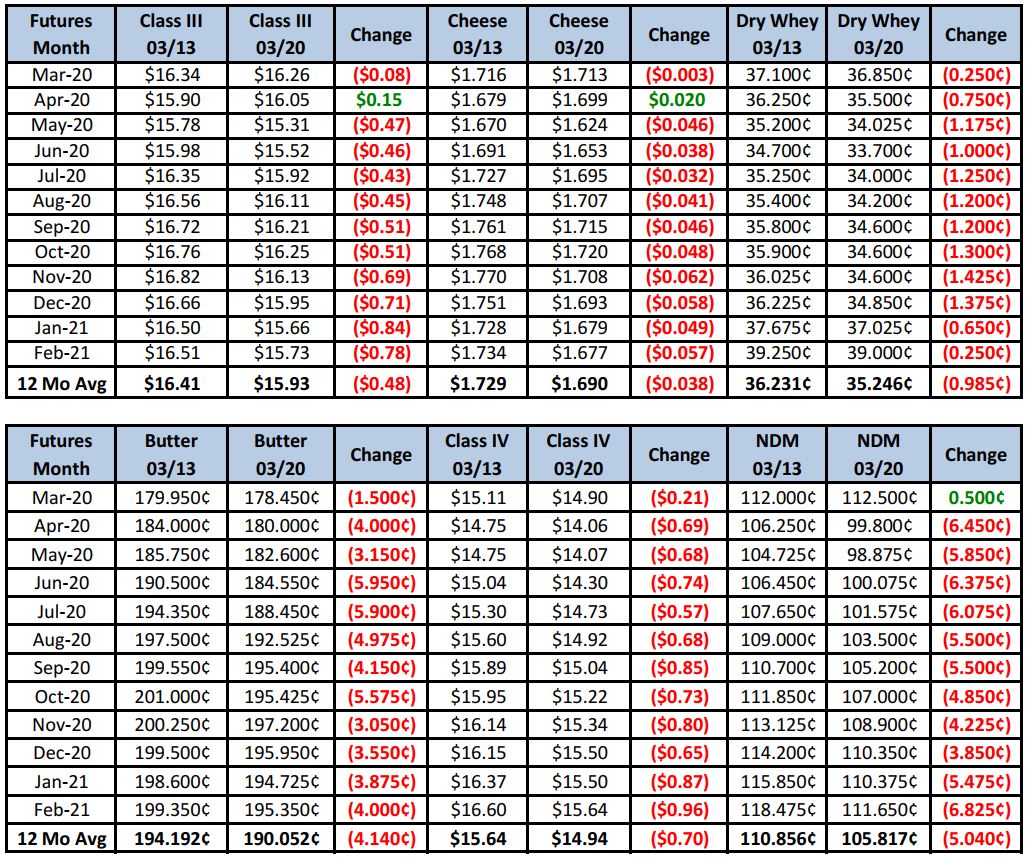

Panic selling intensified, with dramatic losses seen even out into the 2021 futures contracts.

Futures Recap

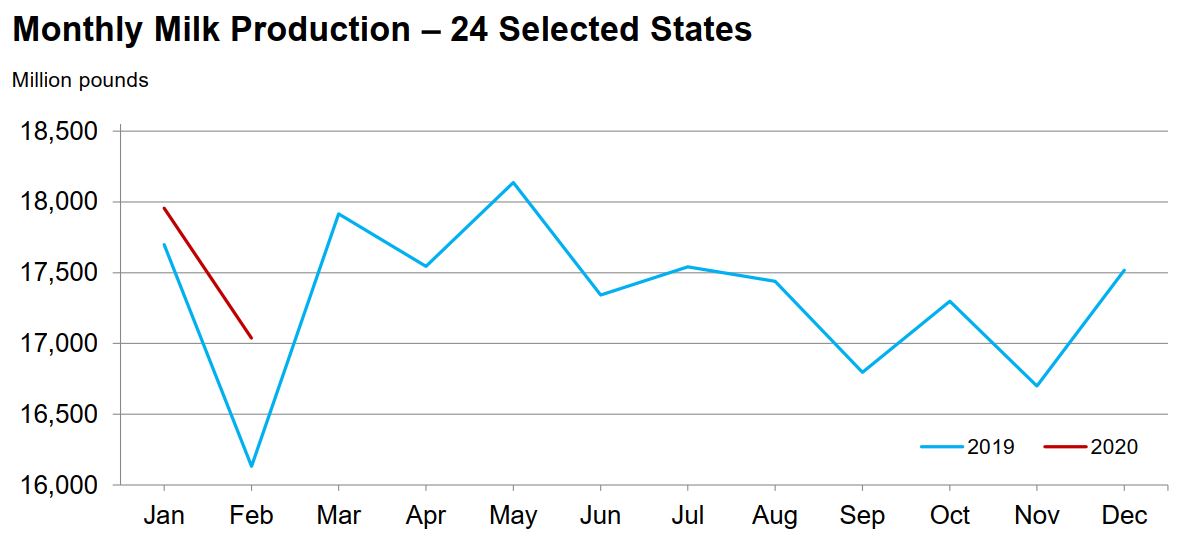

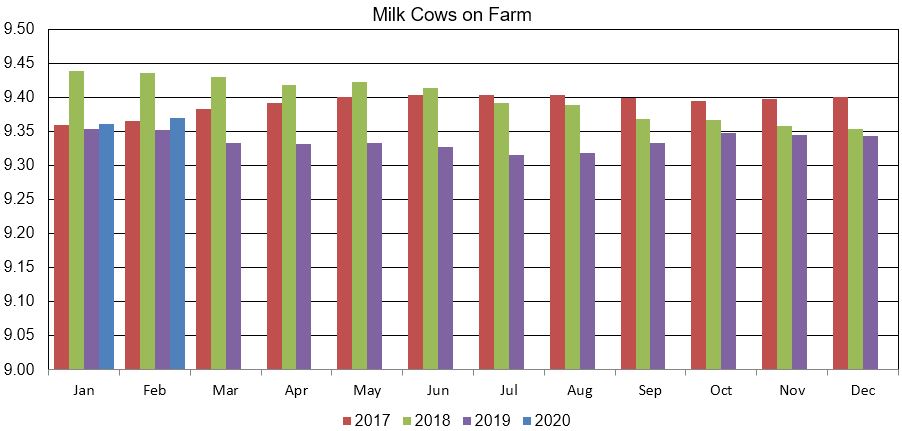

USDA released the Milk Production Report this week. February output was up 5.3% due to the extra day, but still up 1.7% when adjusted for leap year. January cow numbers and production were revised higher, yet cow numbers still increased another 9,000 head from Jan to Feb. The milking herd is growing again, led by TX up 32,000 head, and ID up 27,000 head.

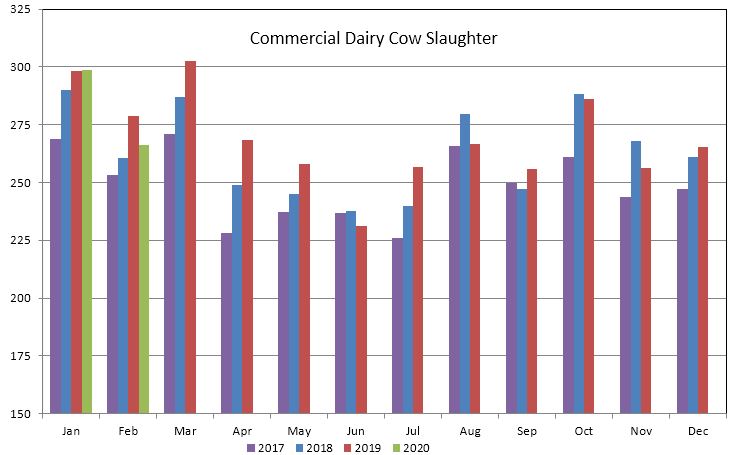

Part of the growth in the milking herd is due to a decline in the cull rate. Weekly numbers have been trailing last year’s numbers the past five weeks, putting the YTD total 29,000 head below (-3.7%) last year. And this week’s Livestock Slaughter Report had the February total dairy cull at 266,100 head, down 12,800 head (-4.6%) vs. 2019; this despite having an extra day in Feb.

Dairy Market News this week reports milk output is increasing across the country, as would be expected this time of year. But due to the “toilet paper effect” of hoarding food staples, retail orders have spiked for butter, cheese and milk. Food service orders from dine-in types of restaurants are predictably much lower, but the net affect has still been a pull for Class I needs to refill grocery aisles, leaving less milk available for cheese production. Dominos Pizza reported this week they may need to hire 10,000 people to meet demand due to the Coronavirus. Weekly cold storage numbers are beginning to reflect the burst in demand, with butter stocks at USDA selected storage centers down 5% (3.4 million lbs) and cheese stocks down 1% (538k lbs) over the first 16 days in March. Stocks usually build during March.

While futures took quite whack this week, they did see a nice rally today, with Class IIIs mostly up double-digits and butter up 8-10¢. However, we want to emphasize that this crisis is likely far from over. The hyper-demand the industry is trying to catch up with may likely be followed by weaker demand as the economy takes a hit. Right now though, contacts are telling us fluid demand is through the roof. That might be enough to give the May Class III contract in particular, a boost. Current spot prices work out to about $15.50 Class III, so when adding in basis, closer to $16.00. May settled at $15.31 today, well below cash. Should the cheese supply temporarily tighten in the next 30 days, due to milk being diverted to fluid, we could see a jump in cheese prices due to a tightening in the fresh cheese supply. Take this with a grain of salt though; this is just an educated guess. Longer-term predictions are even more difficult. Will the herd continue to grow? How long will people’s mobility be impacted? More questions than answers.

Producers may want to look at adding hedges May-July should those months rally further next week, based on the idea that this bounce will be short-lived. Beyond that, we would be cautious selling further out.

Have a great weekend and stay safe!