01/10/2020

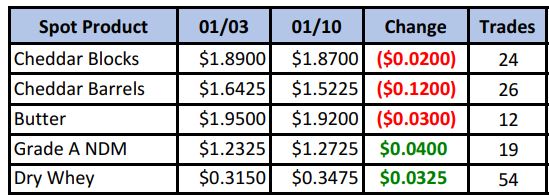

Spot trade volume picked up in the first full week of trading since the week before Christmas. Barrels continued to be pressured, pushing the block/barrel spread to 34.75 cents premium to blocks. Not even two months ago, barrels held a 37 cent premium to blocks and two months before that, blocks held over a 40 cent premium to barrels. The spread is really getting whipped around (see graph below).

Spot Market Recap

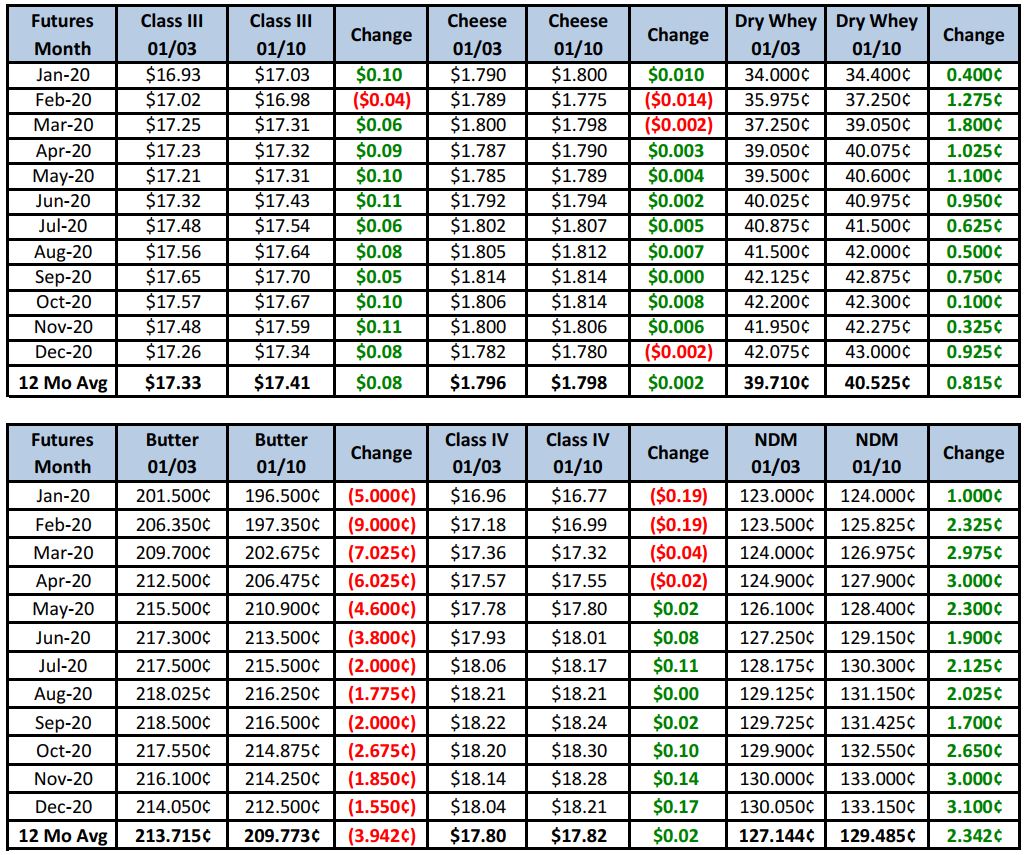

Futures Recap

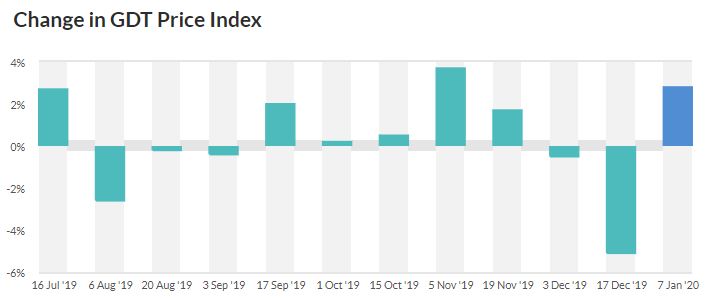

Despite the extreme moves in spot cheese prices, Class III futures have not been near as volatile and have actually shown a reluctance to drop much further. Barrel buyers did get more aggressive as we approached the $1.50 level, with blocks, barrels and butter inching off their mid-week lows on Friday. In addition, there is some strength in both NDM and dry whey as they finished the week higher. NDM pushed in to new highs not seen since 2014. Recall, it was powder-driven rally that spurred Class III to record levels the last time around. Also offering support, this week’s GDT auction saw the dairy price index jump a healthy 2.8%. Cheddar cheese increased 3.7% to a U.S. equivalent $1.82/lb. After months of being the most expensive in the world, suddenly U.S. cheese is price competitive again.

Dairy exports in November continued to shine, up 14% vs. a year ago. NDM/SMP exports surged 41% higher while cheese exports increased 7%. Trade with China continues to improve as exports to that country were up 16% compared to last Nov. On a milk solids basis, total November dairy exports were the equivalent of 15.8% of U.S. milk production during the month.

While some of the long-term fundamentals continue to improve, there are several impediments to higher prices near term. Milk output and components are improving across much of the country as we get closer to spring. While production east of the Rockies is flat to lower, it’s surging in the West, with reports of milk crossing state liens to find a processing home. Even in the Midwest, spot loads of milk are being offered at some pretty steep discounts. Cream is abundant everywhere and churns are running hard. Cheese is in a little better shape. Output is strong and milk is available, but good domestic demand heading into football playoffs, and then March Madness is keeping supplies in check, for now.

Technically, the market continues to be mainly range-bound and appears to be consolidating for its next move. Producers who sold the first half of the year at higher prices should consider buying call options to cover upside risk. Additional calls could be purchased to use as sell targets if and when prices head back up. A few months of higher prices has helped, but not solved, much of America’s dairy financial crisis. Big picture, we still see more upside risk vs. downside risk. For that reason, we would not get too aggressive selling 2020 milk, especially the second half of the year. Up front, it’s hard to tell which way we’ll swing day to day, but hopefully many of you have much of Q1 already hedged.

Have a great weekend!