07/12/2019

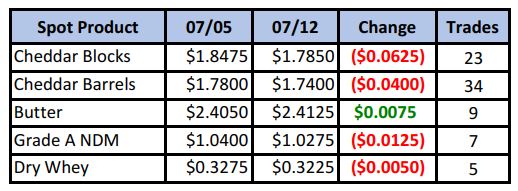

With the exception of butter, all spot Class III components finished lower this week. The block/barrel spread continued to narrow, reaching 4½¢, its tightest since early May. Offers appeared to have the advantage this week, many times with multiple loads seen and no bids. As prices moved lower, however, buyers did step in to make their presence known.

Spot Market Recap

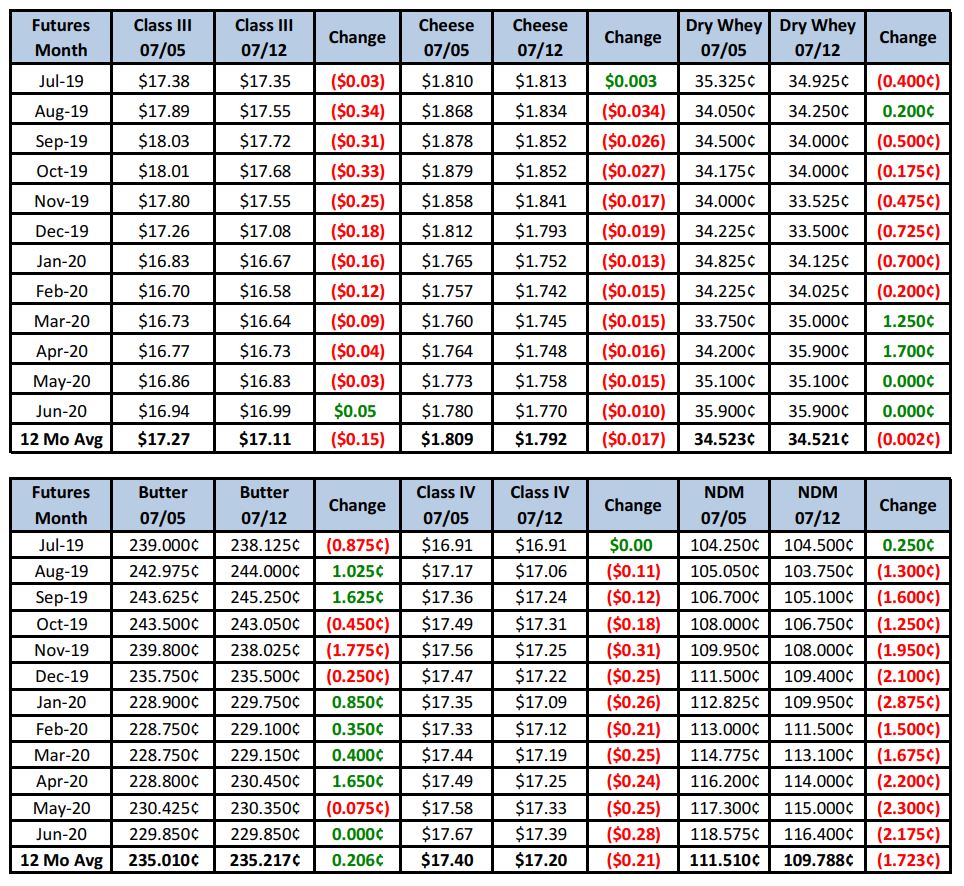

Most futures finished the week solidly in the red, taking the lead from the spot market, and we would expect some further losses up front when trading resumes next week.

Futures Recap

Looking at the Sep Class III chart, we’ve taken prices higher in a very short amount of time. Markets don’t trade in just one direction, so a retracement like this is actually somewhat healthy.

The most recent low-to-high on this daily chart puts the 50% retracement right at $17.50. Could we break through and continue lower? Certainly, but given current fundamentals, we think it’s more likely that buying would begin to get more aggressive around that level. Oct Class III futures looks about the same.

Recapping fundamentals, grains had a major rebound this week as skepticism on USDA’s most recent crop numbers combined with more weather/yield uncertainty, led to aggressive buying to close the week. It doesn’t affect much up front in regards to dairy, but feed costs look like they will be heading higher in the long term. Feed/forage is already a concern in the Midwest due to heavy winter kill.

Milk output in the NE is finally coming off peak levels as heat and humidity have arrived. However, balancing plants are still running at capacity as Class I orders have decreased for the summer. Production in the SE is falling as it’s been hotter there longer. Manufacturers are not at capacity in that part of the country. Spot milk is less available in the Midwest, with very few loads available during the recent holiday weekend. Contacts we spoke to this week indicated some processors’ milk receipts are down and dairy operations continue to shutter. Expectations are for the milk supply to get tighter moving forward. Heading West, milk production is flat in CA, but is in good balance with manufacturing needs. Output continues to decline in AZ and NM and manufacturing plants are not running at full schedules. Class II demand is strong from ice cream plants. Finally, milk output in the Pacific NW remains strong, with plenty of milk available for manufacturing.

Butter remains a bright spot. Production has declined in response to strong pulls by Class II processors, primarily ice cream makers, on available cream supplies. This is restricting churning schedules. Pulling from frozen storage and microfixing is being utilized to meet demand in some instances, especially in the Midwest. Demand remains fair to good across the U.S. Butterfat is at the lowest levels of the year, leading some to believe the market will firm going forward.

Dry whey continues to be plagued by weak demand, but manufacturers have done a good job limiting output, and thus keeping inventories from growing. NDM prices have weakened, but some manufacturers are indicating most stocks for current and future output are highly committed. That should work to keep prices from dropping much further. Demand has increased recently from both bakers and cheese makers, while exports to Mexico are steady to strong as their own milk output is decreasing seasonally.

Mozzarella and provolone cheese supplies are growing in the NE as demand for those varieties has declined. Cheddar cheese demand has increased, however. Midwest cheesemakers are noticing a tightening milk supply, but are still able to run facilities at or near full capacity. Heat and humidity is forecast to hit the region next week, so processors are trying to stay a bit ahead of anticipated demand. They are aware that the milk supply may tighten further in Q4 with the exodus of more dairy farms, and may have to expand their search for extra milk at that time. Meanwhile, but food service and retail demand is nudging higher. Cheese sales in the West are active as grilling season is now in full swing. International sales are harder to land with current prices, leaving cheese inventories plentiful for all buying needs. In particular, there is a lot of Mozarella in warehouses.

Dairy cow slaughter for the week ending 06/26 totaled 55,800 head, down 3.3% vs. the same period a year ago, in another sign that culling is slowing down. The stock market reached in to new record highs this week, with a new high posted on Friday. That may bode well for demand as it boosts consumer confidence. With swelling stock portfolios and 401(k)s, dining out and restaurant sales should continue to improve, boosting dairy sales.

In summary, don’t be surprised by continued weakness next week. Spot cheese prices may continue to decline in the near term. However, with milk output and components falling and global milk production flat, we’d be surprised to see spot cheese fall back in to the $1.60’s. End users of dairy products should see this market correction as a long-term buying opportunity. Dairy farms that have already sold milk should consider buying call options in Q4 to open those hedges to any future upside price movement.

Have a great weekend!