07/05/2019

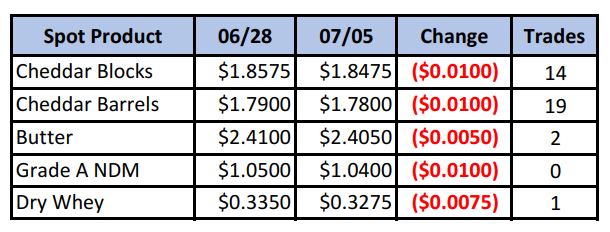

In a holiday-shortened week, spot cheese gave up a penny to bring the block/barrel average to $1.81/lb. Cheese futures, on the other hand, bucked the trend and finished the week solidly higher.

Spot Market Recap

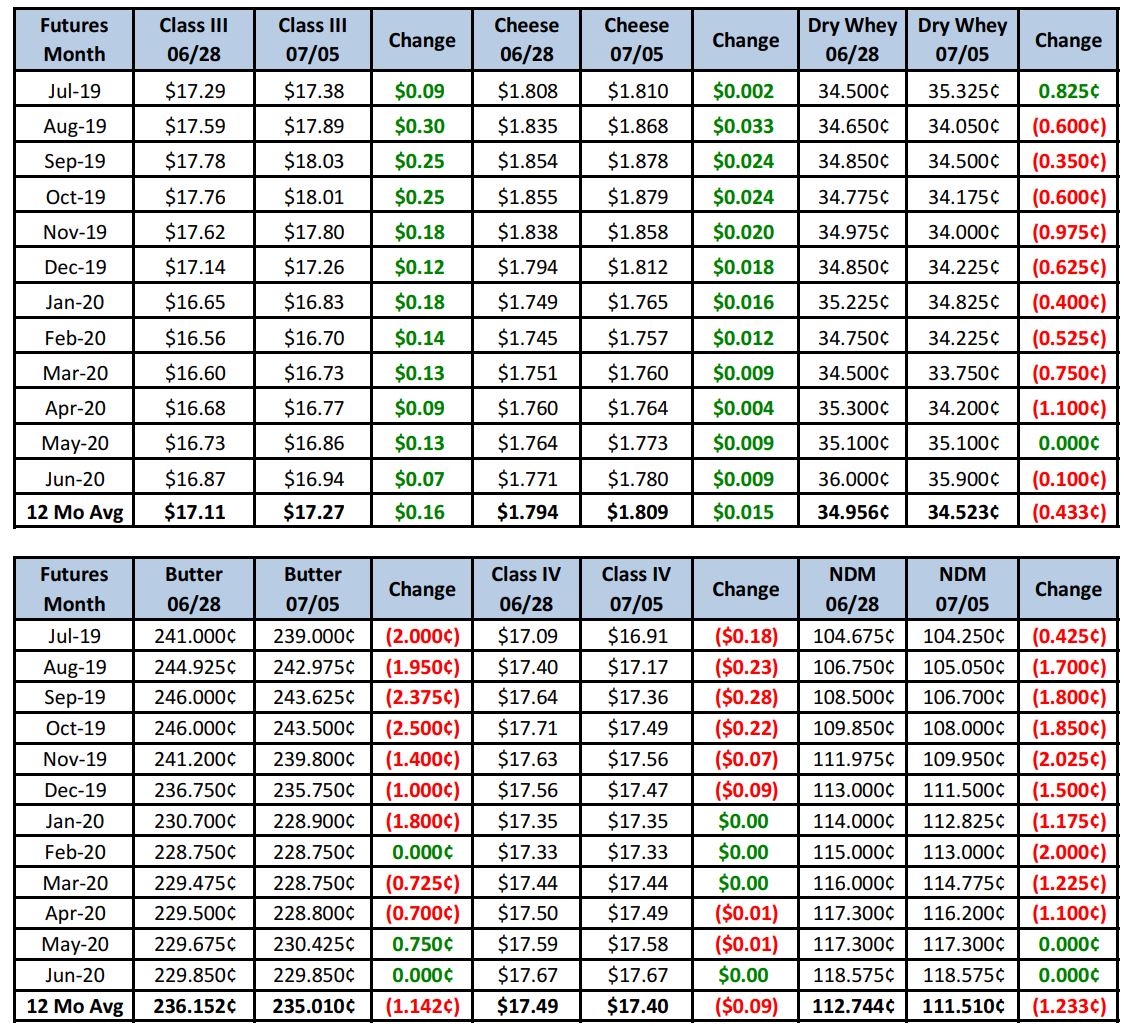

The strength in cheese futures carried over into Class III, with sizeable gains up front. New contract highs were made on Tuesday, before backing off a bit the remainder of the week.

Futures Recap

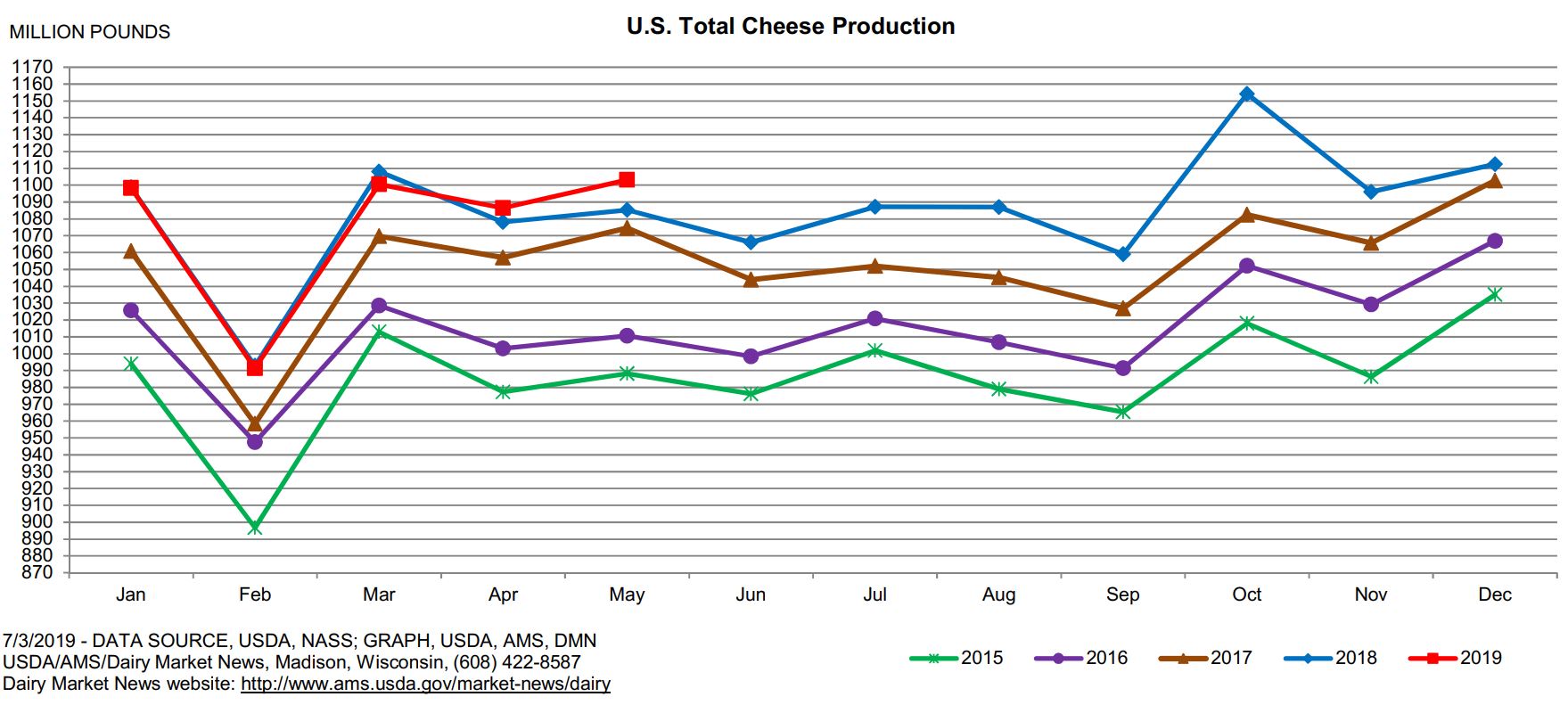

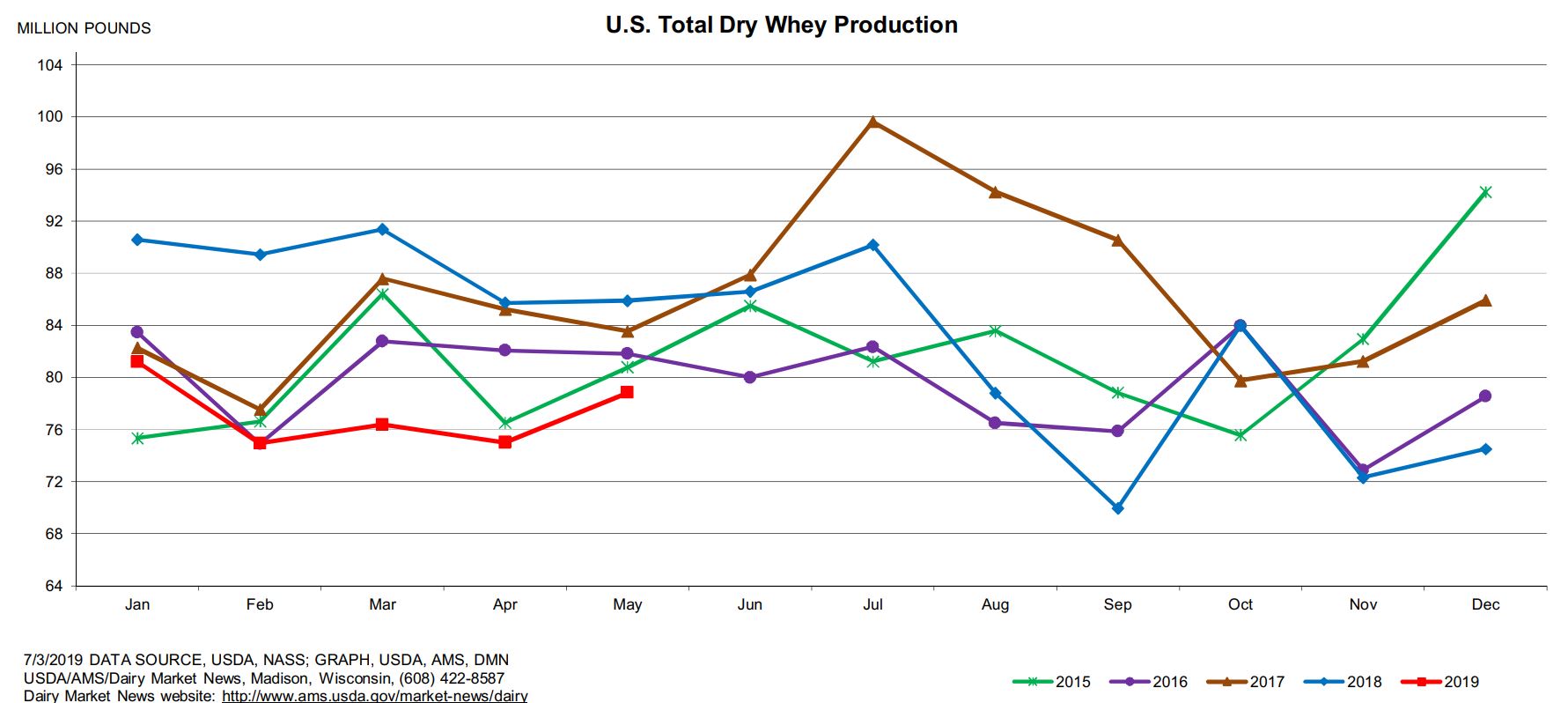

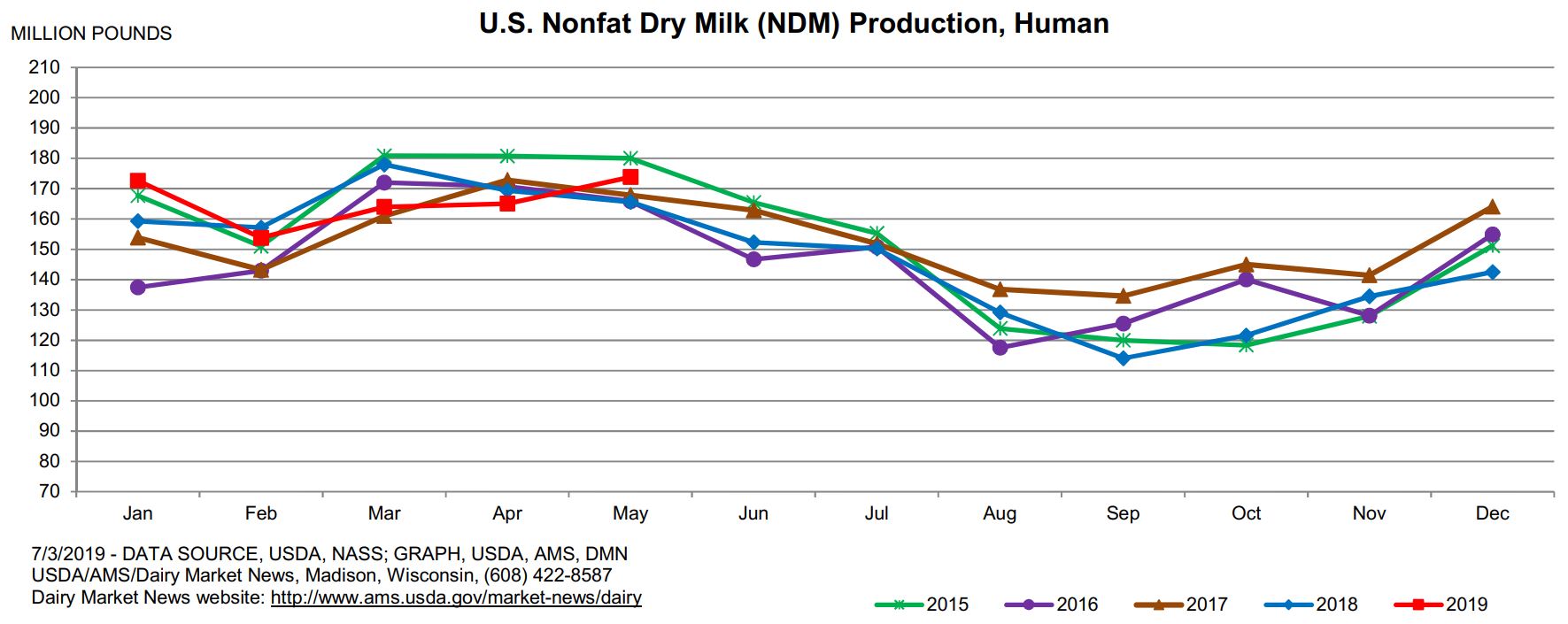

Dry whey output in May fell 7.4% and manufacturers’ stocks were down 4.5% compared to the prior year, but NDM output jumped 5% and manufacturers’ stocks increased 4.2%.

The U.S. Dairy Export Council had some positive news for the market. The value of May dairy exports hit a 4-year high, according to their statistics. The increase was led mainly by an 11% jump in cheese exports. However, due to a loss of sales to China, total dairy export volume in May was down 13% compared to last year. Dairy exports during the month were the equivalent of 14.7% of U.S. milk solids production. Mexico remained the top export market, followed by Southeast Asia, Canada and South Korea. Exports to China fell 44% vs. a year ago, dropping it into the 5th spot.

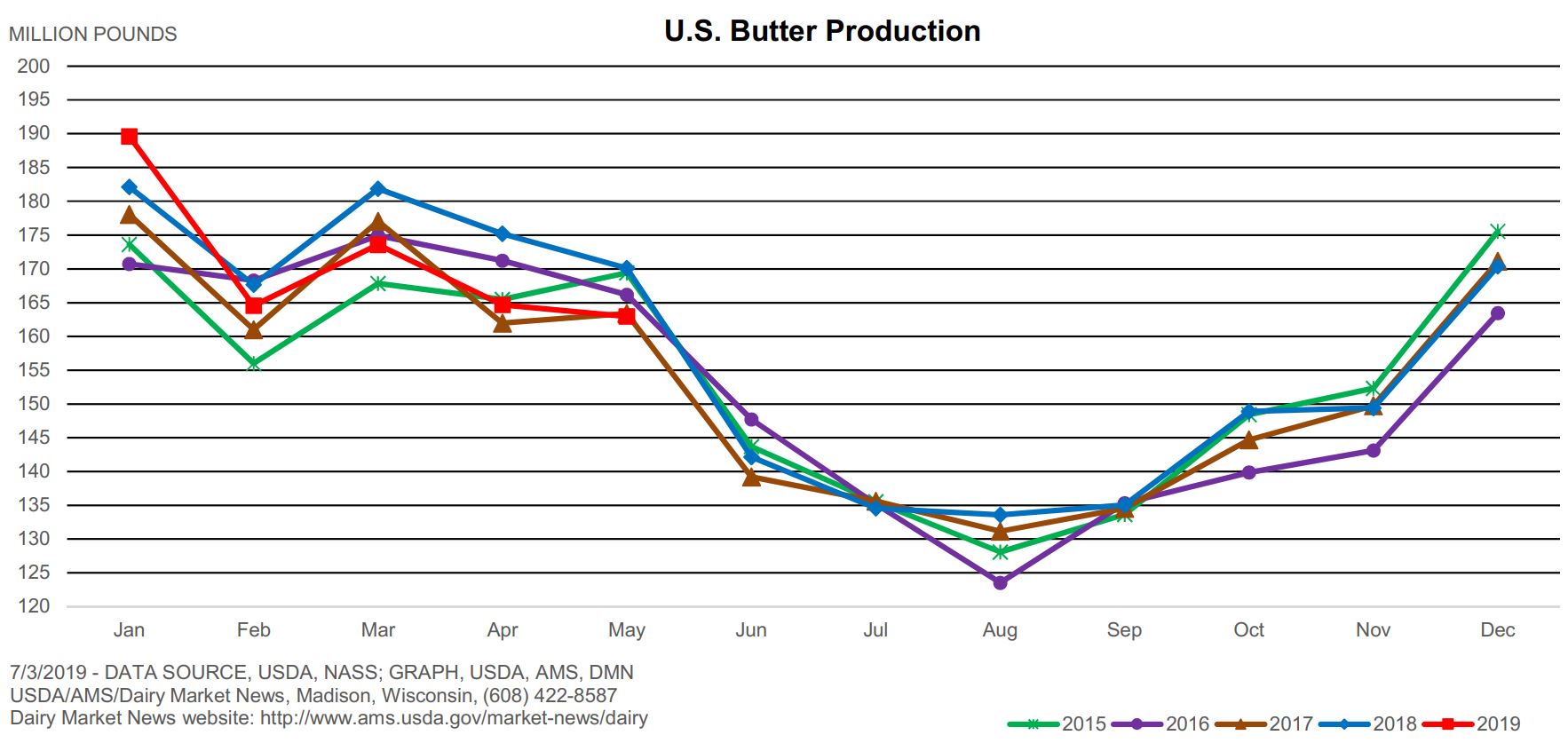

Despite having the world’s most expensive cheese and butter at the moment, the markets still feel well supported. One factor for that is solid domestic demand, which still makes up the vast majority of cheese and butter consumption. Milk output in the Northeast is still keeping processors running full schedules, but production is declining in the Southeast, with Florida back to being a milk-deficit state. Output is still strong in the Central region, but lingering feed issues continue to raise the cost of production and mute the benefit of rising milk prices. Moving West, milk output in California is low enough to the extent that it’s barely enough to meet demand. Production is also declining in AZ and NM as summer heat settles in. Milk is still plentiful in the Pacific Northwest, but components are beginning to fall. Cheese output across the country is active in the East and Midwest, but struggling in the West. Sales have improved and inventories are available, but more processors are beginning to report a tightening of supplies. That’s continuing to lend a bullish tone to the cheese market.

The recent heatwave in Europe has contacts concerned about future milk output in the region. The effects of the heat are expected to linger as cows attempt to recover. It’s still too early to tell, however, what the long term impact will be. French dairy producers are seeing an increase in the number of bankruptcies due to low milk prices and lack of an EU intervention program to help support them. Meanwhile, cow numbers in Germany, the largest milk producing country in the EU, fell 2.4% than a year earlier, bringing the milking herd to its lowest level since 2008.

With milk and cream tightening in the U.S. and production struggling in other major milksheds globally, the market looks set to continue upwards. One question many are now asking is how high? Both the Sep and Oct Class III contracts settled at over $18/cwt, prices we have not seen in some time. Near the end of today’s trading session, both of those contracts were bid more than 40x at 18+ prices. Buyers are still thinking prices can go higher. At one point, we didn’t think $19 Class III was a possibility for 2019, but with the recent help of Mother Nature and a strong U.S. economy and a rebound in grain prices, perhaps we could. There are no guarantees, however, so producers should be looking to protect these much-improved prices. We continue to recommend strategies that leave your upside open. Give us a call and we’ll help you put together a strategy for your operation.

Have a great weekend!