05/24/2019

After last week’s big run up, the dairy markets this week felt a little tired and gave up some ground. It was also a week packed with data releases, but more on that later.

Futures Recap

| Futures Month | Class III 05/17 | Class III 05/24 | Change | Cheese 05/17 | Cheese 05/24 | Change | Dry Whey 05/17 | Dry Whey 05/24 | Change |

| May-19 | $16.30 | $16.38 | $0.08 | $1.692 | $1.692 | $0.000 | 37.900¢ | 38.250¢ | 0.350¢ |

| Jun-19 | $16.45 | $16.31 | ($0.14) | $1.709 | $1.692 | ($0.017) | 36.900¢ | 37.500¢ | 0.600¢ |

| Jul-19 | $16.72 | $16.52 | ($0.20) | $1.740 | $1.719 | ($0.021) | 35.250¢ | 35.950¢ | 0.700¢ |

| Aug-19 | $17.08 | $16.80 | ($0.28) | $1.781 | $1.749 | ($0.032) | 35.000¢ | 35.500¢ | 0.500¢ |

| Sep-19 | $17.25 | $17.04 | ($0.21) | $1.798 | $1.770 | ($0.028) | 35.000¢ | 35.500¢ | 0.500¢ |

| Oct-19 | $17.17 | $16.97 | ($0.20) | $1.793 | $1.771 | ($0.022) | 34.750¢ | 35.000¢ | 0.250¢ |

| Nov-19 | $17.01 | $16.85 | ($0.16) | $1.776 | $1.761 | ($0.015) | 34.125¢ | 35.000¢ | 0.875¢ |

| Dec-19 | $16.68 | $16.55 | ($0.13) | $1.751 | $1.732 | ($0.019) | 34.750¢ | 34.725¢ | (0.025¢) |

| Jan-20 | $16.38 | $16.30 | ($0.08) | $1.715 | $1.709 | ($0.006) | 35.000¢ | 34.850¢ | (0.150¢) |

| Feb-20 | $16.29 | $16.29 | $0.00 | $1.714 | $1.709 | ($0.005) | 34.750¢ | 34.750¢ | 0.000¢ |

| Mar-20 | $16.25 | $16.28 | $0.03 | $1.713 | $1.709 | ($0.004) | 35.250¢ | 35.250¢ | 0.000¢ |

| Apr-20 | $16.29 | $16.35 | $0.06 | $1.722 | $1.717 | ($0.005) | 34.750¢ | 35.150¢ | 0.400¢ |

| 12 Mo Avg | $16.66 | $16.55 | ($0.10) | $1.742 | $1.728 | ($0.015) | 35.285¢ | 38.000¢ | 2.715¢ |

| Futures Month | Butter 05/17 | Butter 05/24 | Change | Class IV 05/17 | Class IV 05/24 | Change | NDM 05/17 | NDM 05/24 | Change |

| May-19 | 229.600¢ | 229.475¢ | (0.125¢) | $16.28 | $16.26 | ($0.02) | 101.300¢ | 101.500¢ | 0.200¢ |

| Jun-19 | 237.000¢ | 238.500¢ | 1.500¢ | $16.85 | $16.96 | $0.11 | 104.025¢ | 103.800¢ | (0.225¢) |

| Jul-19 | 240.100¢ | 241.950¢ | 1.850¢ | $17.14 | $17.12 | ($0.02) | 105.100¢ | 104.750¢ | (0.350¢) |

| Aug-19 | 242.850¢ | 243.300¢ | 0.450¢ | $17.28 | $17.30 | $0.02 | 106.300¢ | 106.000¢ | (0.300¢) |

| Sep-19 | 244.000¢ | 244.600¢ | 0.600¢ | $17.35 | $17.56 | $0.21 | 107.275¢ | 107.525¢ | 0.250¢ |

| Oct-19 | 242.950¢ | 242.500¢ | (0.450¢) | $17.50 | $17.56 | $0.06 | 109.525¢ | 109.450¢ | (0.075¢) |

| Nov-19 | 239.000¢ | 238.100¢ | (0.900¢) | $17.44 | $17.48 | $0.04 | 110.825¢ | 111.175¢ | 0.350¢ |

| Dec-19 | 233.775¢ | 232.450¢ | (1.325¢) | $17.25 | $17.28 | $0.03 | 112.025¢ | 112.725¢ | 0.700¢ |

| Jan-20 | 227.175¢ | 225.525¢ | (1.650¢) | $17.02 | $17.16 | $0.14 | 113.150¢ | 114.025¢ | 0.875¢ |

| Feb-20 | 226.000¢ | 224.625¢ | (1.375¢) | $17.02 | $17.15 | $0.13 | 113.750¢ | 115.050¢ | 1.300¢ |

| Mar-20 | 226.250¢ | 225.575¢ | (0.675¢) | $17.04 | $17.33 | $0.29 | 114.750¢ | 116.475¢ | 1.725¢ |

| Apr-20 | 226.500¢ | 226.500¢ | 0.000¢ | $17.24 | $17.32 | $0.08 | 115.725¢ | 117.925¢ | 2.200¢ |

| 12 Mo Avg | 234.600¢ | 234.425¢ | (0.175¢) | $17.12 | $17.21 | $0.09 | 109.479¢ | 110.033¢ | 0.554¢ |

Spot trading was much lighter this week, with just 1 block trade vs. 19 last week. Blocks still managed to finish a penny higher. Barrel buyers were less active as well, with bids seemingly being hit almost instantly all week. That allowed barrels to sag back under $1.60/lb.

Spot Market Recap

| Spot Product | 5/17 | 5/24 | Change |

| Cheddar Blocks | $1.6725 | $1.6825 | $0.0100 |

| Cheddar Barrels | $1.6250 | $1.5800 | ($0.0450) |

| Butter | $2.3400 | $2.3875 | $0.0475 |

| Grade A NDM | $1.0475 | $1.0450 | ($0.0025) |

| Dry Whey | $0.3400 | $0.3600 | $0.0200 |

Spot Market Trade Volume

The much-anticipated Milk Production Report was released on Monday, and it was really a mixed bag. Milk output during the month of April was actually 0.1% higher than last April, surprising a few analysts. Just the month prior, milk output saw its first YoY decline, so it was thought that trend would continue.

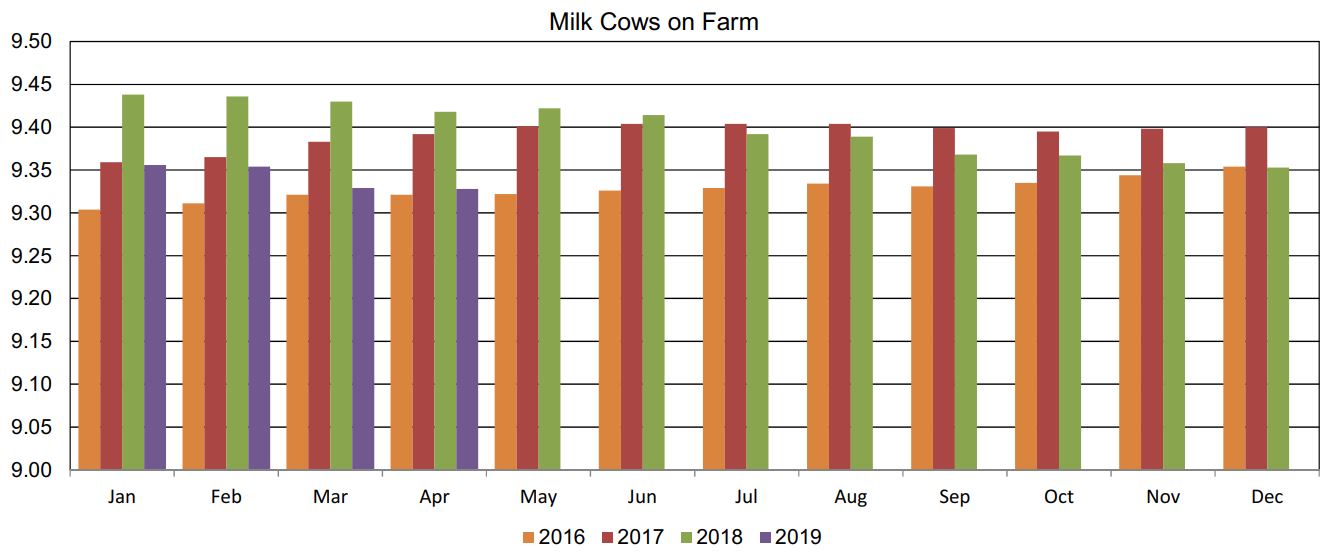

On the positive side, cow numbers declined 1,000 head from March to April, even after a 15,000 head revision lower for March. At 9.328 million head, it puts the milking herd at its lowest level since June 2016, and down 90,000 head from a year ago.

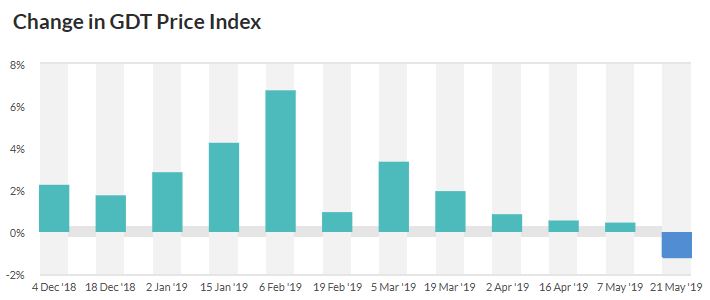

On Tuesday we had a GDT auction, with the Dairy Price Index declining 1.2% vs. the previous event. It was the first negative result in 11 events.

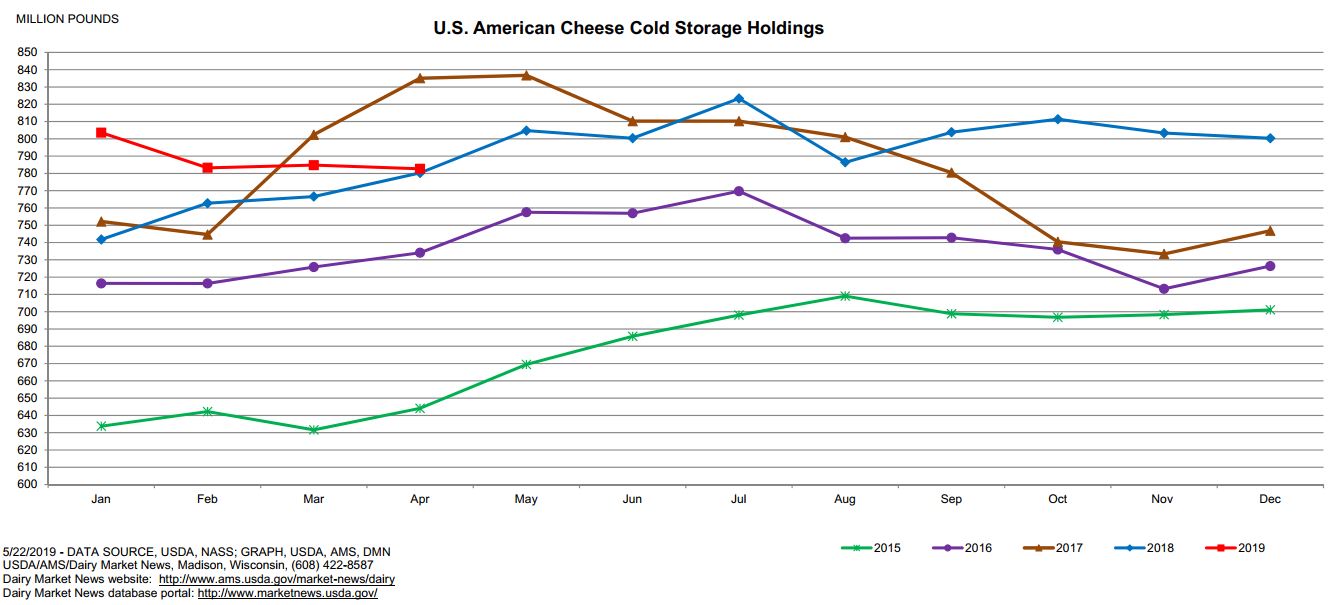

The Cold Storage Report was released Wednesday, and once again we had a mixed bag. American cheese stocks at the end of April were unchanged vs. a year ago, while Total cheese stocks were up 4%.

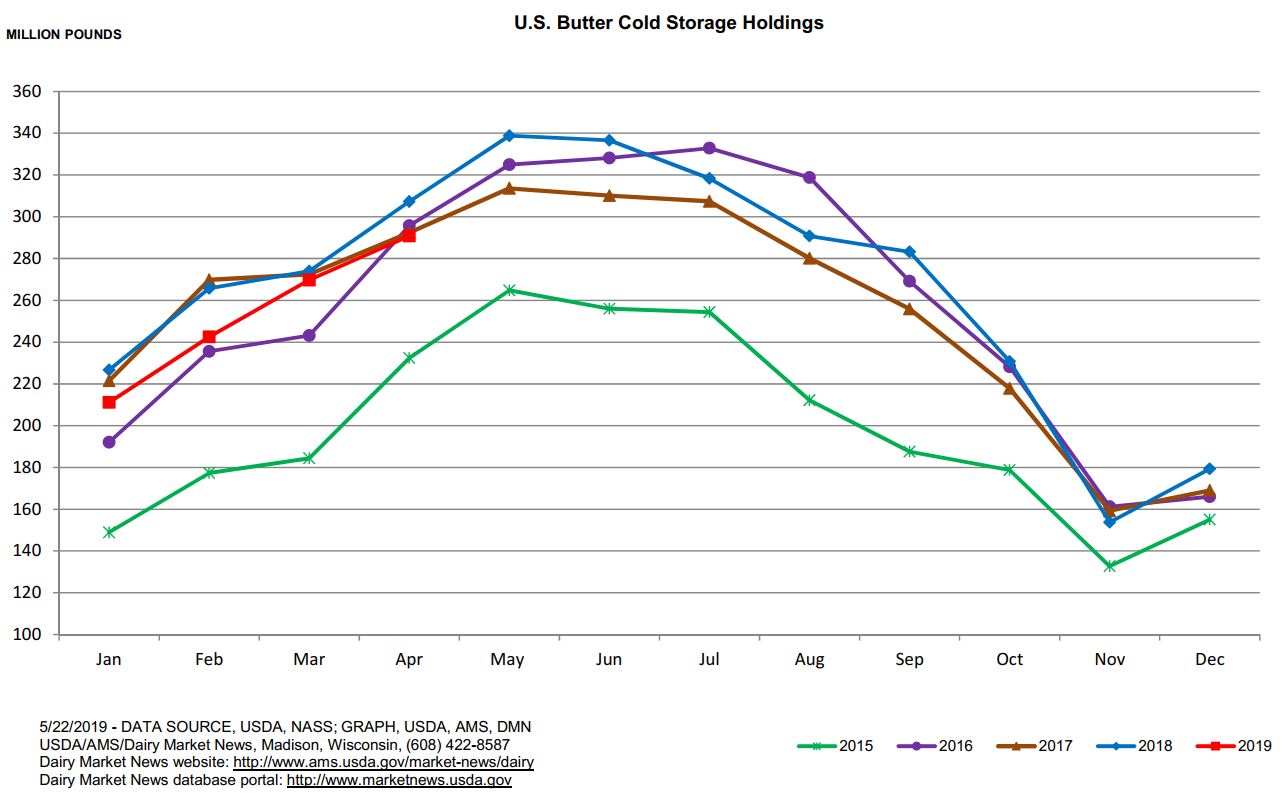

Butter stocks, on the other hand, were down 5% vs. the prior year, and at their lowest levels since 2015.

While there will be some extra cream available over Memorial Day weekend, cream supplies across the U.S. continue to tighten as ice cream and other frozen dessert manufacturers are pulling considerable amounts of butterfat. This is limiting the amount of spot cream loads for some butter makers and forcing them to draw from frozen stocks and microfix to produce print butter. Dairy Market News updates this week continue to point to a muted spring flush. Milk volumes are level across the East and Mid-Atlantic, but are high enough to keep balancing plants at capacity. Further south, milk output is beginning to drop. In the Central region, fewer cows is equating to less milk, with spot loads staying within the $.50 below to $.50 above Class range. In the West, output in California is now below peak levels, but is meeting current demand. Arizona’s milk output is falling and not meeting the needs of some processors. Milk loads from surrounding states are being shipped in. Output in the Pacific Northwest is up slightly, but appearing to be leveling off.

Heading overseas, EU milk production Jan-Mar was down 0.1% vs. the prior year. There is optimism that output will increase in April, but demand is also on the rise. Prices firmed for skim milk powder this week, with most Q2 production already sold. Cheese sales are active, but there is not enough milk to be able to increase output. Spot loads of cheese are hard to find.

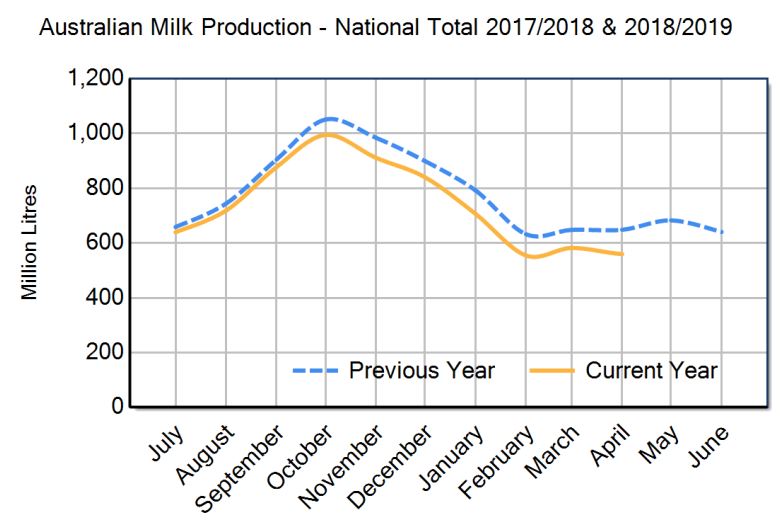

In Australia, the milking season continues to wind down, yet April milk output fell below prior year levels by a stunning 13.7%. YTD (July-April), their current milking season output is down 7.3% vs. the prior season.

High irrigation costs and difficult weather conditions in most dairy regions were cited for the decline. Output is expected to fall further, and struggle next season, as culling levels stay high and feed shortages force some to dry cows off early.

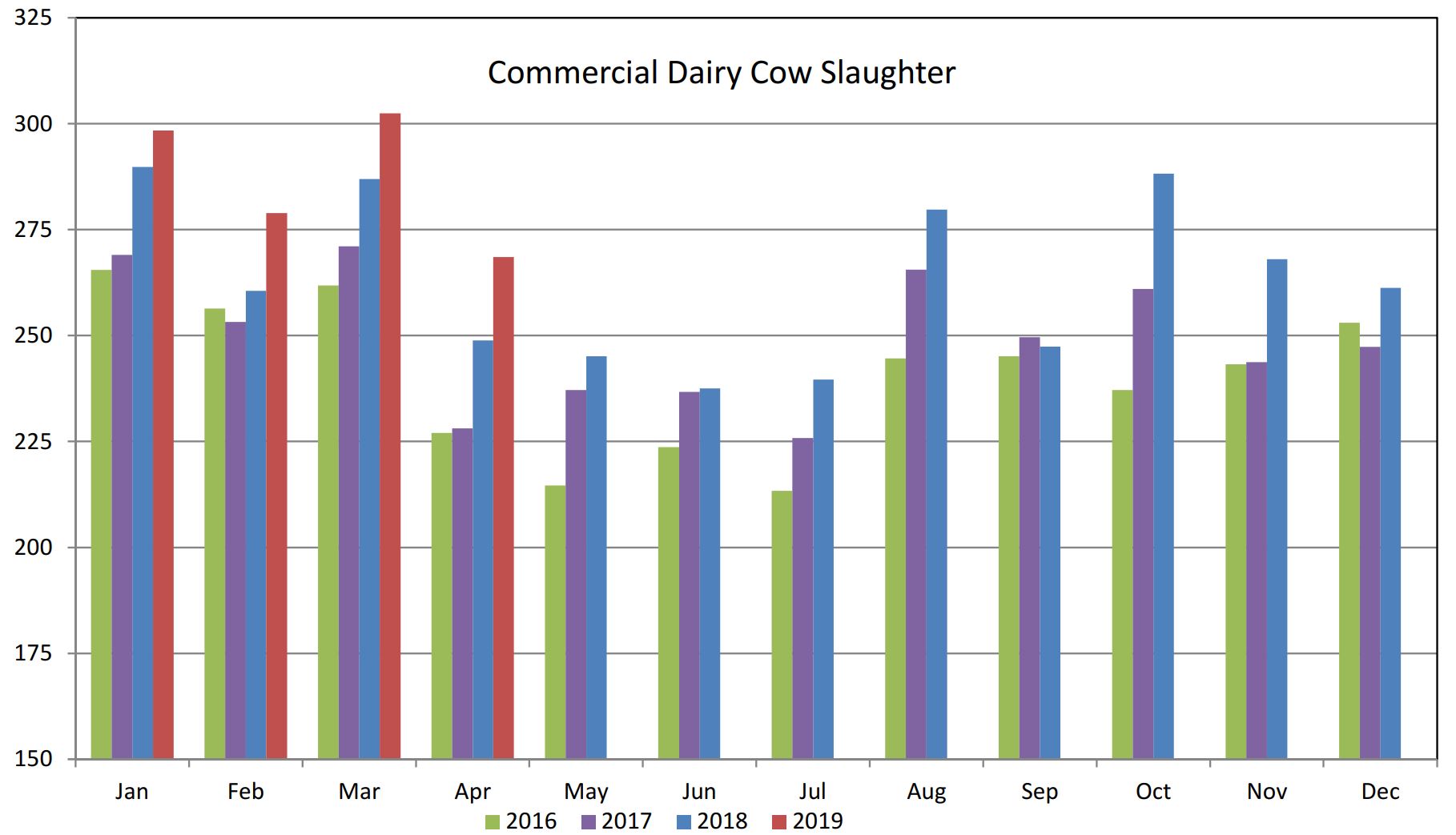

Back to the U.S., weekly culling data came back to the positive column, with 57,800 dairy cows removed from the herd for the week ending 05/11. That’s up 4.5% vs. the same week a year ago. And the Livestock Slaughter Report was released Thursday. 268,500 dairy cows were culled during April, the highest total for that month in more than a decade, and up a strong 7.9% (19,600 head) vs. last year.

It’s a bit hard to say where we go from here after observing the pullback in the markets this week. There will be surplus milk available over the holiday weekend, and schools are closing more rapidly. With barrel cheese taking a bit of a tumble, will block cheese be the next to fall? The deepening trade war with China is not helping matters either, as well as the geopolitical turmoil from Brexit. Financial markets were very whippy this week. On the positive side, domestic demand appears to be very good, with grilling season getting into full swing soon. Cool, wet weather has the corn planting season way behind and probably too late for many acres that may remain fallow. Corn futures rocketed higher this week, with the December contract reaching nearly $4.20/bu, a price not seen since last June. The cost of feed is almost assuredly going to climb. Output in the EU is mainly flat, but weather will play a role there. Oceania will most likely struggle to increase output at the start of their next milking season in a few months. Financial woes in Australia will make it tough to expand, while the swine flu virus is affecting powder exports in New Zealand too. For a country the exports most of its dairy output, this is particularly tough on their operations. And here in the U.S. we continue to hear about the continued closings of many farm operations in the Midwest and East. Though mainly smaller, it is keeping a lid on output. Globally, then, milk output and dairy fat looks like it could be on the tighter side going forward. Producers should consider getting coverage up front, where the weak spot market could push prices lower. Longer term we would be cautious getting too aggressive on the sell side. Current spot prices work out to about $15.95 Class III, but the strength in butter and NDM has Class IV at about $17.00. With butter looking bullish, further gains in Class IV could begin to pull Class III along for the ride.

Note: Our offices will be closed on Monday in observance of Memorial Day. Enjoy your freedom and thank a veteran!