04/26/2019

Barrel buyers came back after the Easter holiday and pushed the spot price to a new high for the year. At $1.63/lb, barrels haven’t been this high since last September. NDM came within a quarter-cent at tying the high for the year. With milk output on the decline, it may be a matter of days before it does. Despite cream getting tighter across the country, spot butter couldn’t gain any traction, finishing the week lower. A post-holiday lull in orders is the likely cause. And finally, dry whey continues to suffer from weak demand, forcing sellers to the CME.

Spot Market Recap

| Spot Product | 4/18 | 4/26 | Change |

| Cheddar Blocks | $1.6675 | $1.6850 | $0.0175 |

| Cheddar Barrels | $1.5150 | $1.6300 | $0.1150 |

| Butter | $2.2825 | $2.2700 | ($0.0125) |

| Grade A NDM | $1.0000 | $1.0400 | $0.0400 |

| Dry Whey | $0.3400 | $0.3275 | ($0.0125) |

Spot Market Trade Volume

With barrel buyers driving cheese prices higher, plus surprises in some monthly USDA reports (more on that below), Class III futures up front went on a tear higher. Even 2020 contracts were double-digits higher. And despite spot butter prices losing ground, butter futures finished with a solid week, as the cream situation looks to tighten up very soon.

Futures Recap

| Futures Month | Class III 04/18 | Class III 04/26 | Change | Cheese 04/18 | Cheese 04/26 | Change | Dry Whey 04/18 | Dry Whey 04/26 | Change |

| Apr-19 | $15.92 | $15.97 | $0.05 | $1.642 | $1.646 | $0.004 | 39.000¢ | 39.000¢ | 0.000¢ |

| May-19 | $15.69 | $16.32 | $0.63 | $1.620 | $1.690 | $0.070 | 38.275¢ | 37.550¢ | (0.725¢) |

| Jun-19 | $15.95 | $16.39 | $0.44 | $1.650 | $1.705 | $0.055 | 37.750¢ | 36.500¢ | (1.250¢) |

| Jul-19 | $16.19 | $16.53 | $0.34 | $1.675 | $1.721 | $0.046 | 38.000¢ | 36.250¢ | (1.750¢) |

| Aug-19 | $16.42 | $16.74 | $0.32 | $1.701 | $1.741 | $0.040 | 37.525¢ | 36.500¢ | (1.025¢) |

| Sep-19 | $16.65 | $16.94 | $0.29 | $1.719 | $1.757 | $0.038 | 37.750¢ | 36.500¢ | (1.250¢) |

| Oct-19 | $16.65 | $16.89 | $0.24 | $1.729 | $1.761 | $0.032 | 37.825¢ | 36.500¢ | (1.325¢) |

| Nov-19 | $16.58 | $16.78 | $0.20 | $1.724 | $1.751 | $0.027 | 37.900¢ | 36.250¢ | (1.650¢) |

| Dec-19 | $16.42 | $16.61 | $0.19 | $1.705 | $1.728 | $0.023 | 37.600¢ | 36.500¢ | (1.100¢) |

| Jan-20 | $16.10 | $16.27 | $0.17 | $1.680 | $1.702 | $0.022 | 37.625¢ | 37.000¢ | (0.625¢) |

| Feb-20 | $16.05 | $16.25 | $0.20 | $1.676 | $1.695 | $0.019 | 38.000¢ | 37.250¢ | (0.750¢) |

| Mar-20 | $16.08 | $16.24 | $0.16 | $1.676 | $1.700 | $0.024 | 37.900¢ | 37.825¢ | (0.075¢) |

| 12 Mo Avg | $16.23 | $16.49 | $0.27 | $1.683 | $1.716 | $0.033 | 37.929¢ | 38.000¢ | 0.071¢ |

| Futures Month | Butter 04/18 | Butter 04/26 | Change | Class IV 04/18 | Class IV 04/26 | Change | NDM 04/18 | NDM 04/26 | Change |

| Apr-19 | 227.525¢ | 227.525¢ | 0.000¢ | $15.77 | $15.81 | $0.04 | 96.700¢ | 96.500¢ | (0.200¢) |

| May-19 | 230.000¢ | 230.500¢ | 0.500¢ | $16.25 | $16.32 | $0.07 | 101.250¢ | 101.975¢ | 0.725¢ |

| Jun-19 | 232.700¢ | 233.500¢ | 0.800¢ | $16.61 | $16.75 | $0.14 | 104.250¢ | 104.875¢ | 0.625¢ |

| Jul-19 | 234.525¢ | 235.275¢ | 0.750¢ | $16.83 | $17.04 | $0.21 | 106.000¢ | 107.500¢ | 1.500¢ |

| Aug-19 | 236.000¢ | 236.575¢ | 0.575¢ | $16.97 | $17.15 | $0.18 | 107.250¢ | 108.575¢ | 1.325¢ |

| Sep-19 | 236.975¢ | 238.000¢ | 1.025¢ | $17.10 | $17.30 | $0.20 | 108.625¢ | 110.175¢ | 1.550¢ |

| Oct-19 | 235.450¢ | 237.000¢ | 1.550¢ | $17.10 | $17.35 | $0.25 | 109.375¢ | 111.150¢ | 1.775¢ |

| Nov-19 | 232.900¢ | 235.450¢ | 2.550¢ | $17.06 | $17.34 | $0.28 | 109.975¢ | 112.125¢ | 2.150¢ |

| Dec-19 | 228.400¢ | 229.225¢ | 0.825¢ | $16.93 | $17.21 | $0.28 | 110.675¢ | 113.075¢ | 2.400¢ |

| Jan-20 | 222.900¢ | 224.025¢ | 1.125¢ | $16.77 | $17.00 | $0.23 | 110.500¢ | 113.725¢ | 3.225¢ |

| Feb-20 | 221.050¢ | 222.775¢ | 1.725¢ | $16.80 | $17.00 | $0.20 | 112.000¢ | 114.475¢ | 2.475¢ |

| Mar-20 | 221.350¢ | 223.200¢ | 1.850¢ | $16.84 | $17.10 | $0.26 | 112.225¢ | 115.050¢ | 2.825¢ |

| 12 Mo Avg | 229.981¢ | 231.088¢ | 1.106¢ | $16.75 | $16.50 | ($0.25) | 107.402¢ | 109.100¢ | 1.698¢ |

Commentary

Last week we said we were getting more bullish and suggested getting more aggressive covering upside risks, but even we did not expect the rocket ship that lifted off this week. A combination of spec short-covering as well as new longs were likely behind the push, which blew through several layers of resistance. Friday saw the market swing both ways, with short-term profit taking and some renewed producer hedging at prices they have not seen in months available to them. Friday’s settlements finished well off the highs of the day, but also well off the lows. The market is still technically “over-bought” and could see some more downside next week, but we expect higher lows and higher highs to ensue. Helping fuel the bull, a lot of data was release this week.

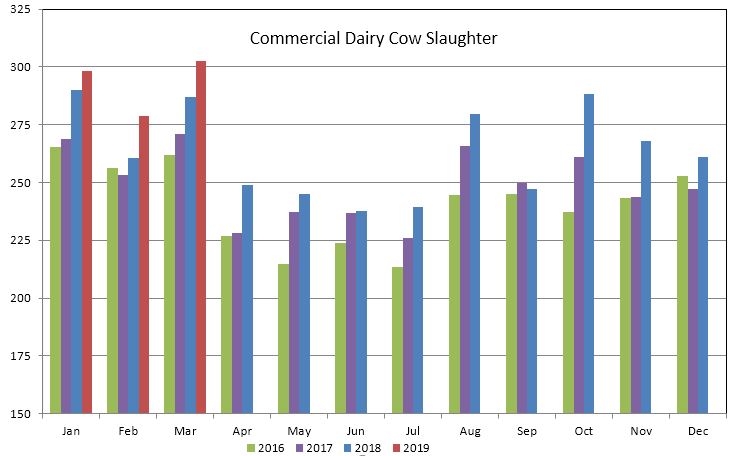

Slaughter numbers continue to impress with weekly numbers up 3.2%, but the big star was the monthly Livestock Slaughter Report, indicating 302,400 head were removed from the herd in March, up 5.4% (15,500 head) vs. a year ago, and the highest single monthly total in over a decade.

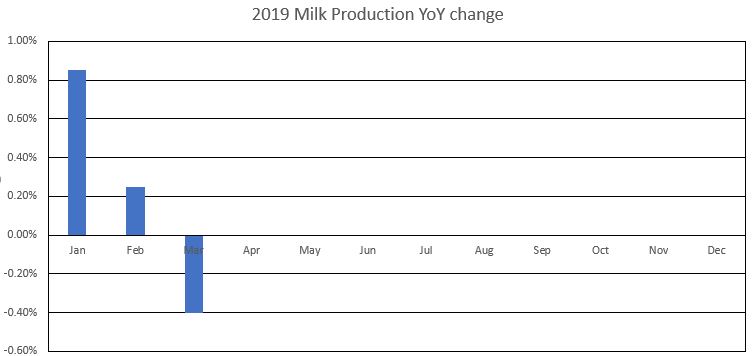

The Milk Production Report surprised analysts who expected cow numbers to remain largely the same month-to-month and for output to increase slightly year-over-year. Instead, USDA reported March milk output in the U.S. declined 0.4% compared to a year ago. It was the first YoY decline since Feb 2017 (though Feb 2016 was a leap year with an extra day of production).

More of a surprise, cow numbers declined 10,000 head from February, an indication that herd liquidation was picking up. At 9.344 million head, the U.S. milking herd is now 86,000 head smaller than it was a year ago.

This week’s Cold Storage Report didn’t do much to move the market, but butter stocks at the end of March were down 1% compared to last year, while American Cheese stocks were up a modest 2%.

Dairy Market News weekly updates continue to paint a picture of a slightly tighter milk supply in the East and Midwest. Cheese processors in the Midwest cite improving cheese demand with milk availability balanced to short. Spot loads of milk marked $3-5 under class are no longer available, but are now going for up to $1 over class. Across the country, the spring flush is seeming to have less of an impact, with milk handlers able to find homes for the milk more easily than in years past. Cheese inventories are balanced east of the Rockies, with the West still reporting heavier supplies. With the weather continuing to warm up across the country, fluid milk production is still rising, but it won’t be long before components come under pressure. Demand for cream is rising as ice cream manufacturers begin competing for available supplies. Schools will be letting out soon, which will also lesson the cream supply. Butter manufacturers are expecting cream prices to rise in the near future. Dry whey continues to put a drag on the market, but a tighter milk supply and lower cheese output may help it carve out a bottom soon. Higher milk prices are certainly a welcome sign. Producers who have not hedge much of their output should begin looking at PUT options up front to guard against a retracement. We would not recommend contracting milk in the 2020 months yet, as we believe the upside risk is still higher than any potential downside. Expect volatility again next week as the market tries to figure out where it should be priced. Have a great weekend!