05/03/2019

This week it was block buyers that caused the fireworks, as buyers picked up 22 of 25 loads on Friday. While overall cheese stocks are still heavy, young cheese, aged under 30 days, and the kind traded at the spot market, might be showing some signs of tightening. Blocks still finished the week lower, but came off the low put in earlier. Barrel cheese as well continued to march higher on good volume.

Spot Market Recap

| Spot Product | 4/26 | 5/3 | Change |

| Cheddar Blocks | $1.6850 | $1.6750 | ($0.0100) |

| Cheddar Barrels | $1.6300 | $1.6625 | $0.0325 |

| Butter | $2.2700 | $2.2700 | $0.0000 |

| Grade A NDM | $1.0400 | $1.0525 | $0.0125 |

| Dry Whey | $0.3275 | $0.3475 | $0.0200 |

Spot Market Trade Volume

The block/barrel average is once again making a run at resistance after rejecting its recent move lower (see chart below). Will the 4th time be the charm? Cheese futures are predicting prices well over $1.70/lb, so a break above could happen as early as next week.

Futures Recap

| Futures Month | Class III 04/26 | Class III 05/03 | Change | Cheese 04/26 | Cheese 05/03 | Change | Dry Whey 04/26 | Dry Whey 05/03 | Change |

| May-19 | $16.32 | $16.37 | $0.05 | $1.690 | $1.690 | $0.000 | 37.550¢ | 38.900¢ | 1.350¢ |

| Jun-19 | $16.39 | $16.58 | $0.19 | $1.705 | $1.716 | $0.011 | 36.500¢ | 37.600¢ | 1.100¢ |

| Jul-19 | $16.53 | $16.77 | $0.24 | $1.721 | $1.739 | $0.018 | 36.250¢ | 37.300¢ | 1.050¢ |

| Aug-19 | $16.74 | $17.08 | $0.34 | $1.741 | $1.769 | $0.028 | 36.500¢ | 37.000¢ | 0.500¢ |

| Sep-19 | $16.94 | $17.21 | $0.27 | $1.757 | $1.780 | $0.023 | 36.500¢ | 37.250¢ | 0.750¢ |

| Oct-19 | $16.89 | $17.16 | $0.27 | $1.761 | $1.778 | $0.017 | 36.500¢ | 36.775¢ | 0.275¢ |

| Nov-19 | $16.78 | $17.00 | $0.22 | $1.751 | $1.765 | $0.014 | 36.250¢ | 37.350¢ | 1.100¢ |

| Dec-19 | $16.61 | $16.70 | $0.09 | $1.728 | $1.740 | $0.012 | 36.500¢ | 37.100¢ | 0.600¢ |

| Jan-20 | $16.27 | $16.40 | $0.13 | $1.702 | $1.710 | $0.008 | 37.000¢ | 36.875¢ | (0.125¢) |

| Feb-20 | $16.25 | $16.26 | $0.01 | $1.695 | $1.700 | $0.005 | 37.250¢ | 36.750¢ | (0.500¢) |

| Mar-20 | $16.24 | $16.30 | $0.06 | $1.700 | $1.696 | ($0.004) | 37.825¢ | 37.000¢ | (0.825¢) |

| Apr-20 | $16.26 | $16.31 | $0.05 | $1.695 | $1.706 | $0.011 | 38.400¢ | 37.875¢ | (0.525¢) |

| 12 Mo Avg | $16.52 | $16.68 | $0.16 | $1.721 | $1.732 | $0.012 | 36.919¢ | 38.000¢ | 1.081¢ |

| Futures Month | Butter 04/18 | Butter 04/26 | Change | Class IV 04/18 | Class IV 04/26 | Change | NDM 04/18 | NDM 04/26 | Change |

| Apr-19 | 227.525¢ | 227.525¢ | 0.000¢ | $15.77 | $15.81 | $0.04 | 96.700¢ | 96.500¢ | (0.200¢) |

| May-19 | 230.000¢ | 230.500¢ | 0.500¢ | $16.25 | $16.32 | $0.07 | 101.250¢ | 101.975¢ | 0.725¢ |

| Jun-19 | 232.700¢ | 233.500¢ | 0.800¢ | $16.61 | $16.75 | $0.14 | 104.250¢ | 104.875¢ | 0.625¢ |

| Jul-19 | 234.525¢ | 235.275¢ | 0.750¢ | $16.83 | $17.04 | $0.21 | 106.000¢ | 107.500¢ | 1.500¢ |

| Aug-19 | 236.000¢ | 236.575¢ | 0.575¢ | $16.97 | $17.15 | $0.18 | 107.250¢ | 108.575¢ | 1.325¢ |

| Sep-19 | 236.975¢ | 238.000¢ | 1.025¢ | $17.10 | $17.30 | $0.20 | 108.625¢ | 110.175¢ | 1.550¢ |

| Oct-19 | 235.450¢ | 237.000¢ | 1.550¢ | $17.10 | $17.35 | $0.25 | 109.375¢ | 111.150¢ | 1.775¢ |

| Nov-19 | 232.900¢ | 235.450¢ | 2.550¢ | $17.06 | $17.34 | $0.28 | 109.975¢ | 112.125¢ | 2.150¢ |

| Dec-19 | 228.400¢ | 229.225¢ | 0.825¢ | $16.93 | $17.21 | $0.28 | 110.675¢ | 113.075¢ | 2.400¢ |

| Jan-20 | 222.900¢ | 224.025¢ | 1.125¢ | $16.77 | $17.00 | $0.23 | 110.500¢ | 113.725¢ | 3.225¢ |

| Feb-20 | 221.050¢ | 222.775¢ | 1.725¢ | $16.80 | $17.00 | $0.20 | 112.000¢ | 114.475¢ | 2.475¢ |

| Mar-20 | 221.350¢ | 223.200¢ | 1.850¢ | $16.84 | $17.10 | $0.26 | 112.225¢ | 115.050¢ | 2.825¢ |

| 12 Mo Avg | 229.981¢ | 231.088¢ | 1.106¢ | $16.75 | $16.50 | ($0.25) | 107.402¢ | 109.100¢ | 1.698¢ |

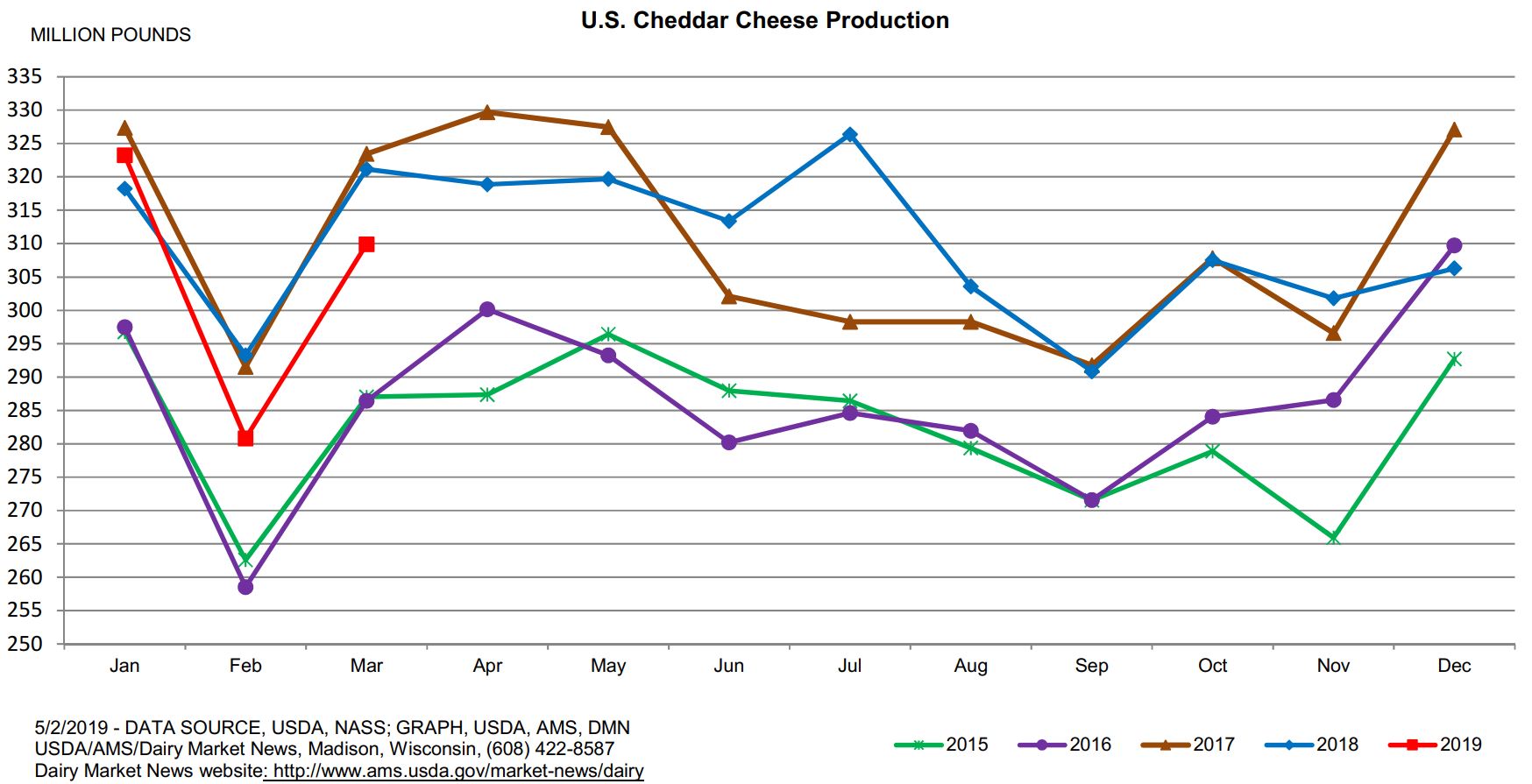

With last week’s surprise Milk Production Report still fresh in the minds of decision makers, the appetite to own milk at at levels still within the range of the past three years compelled some aggressive buying, even well out into the 2020 contracts. And it makes sense. If you are an end user of dairy, why not lock in some of your input costs at these levels? But it was also the Dairy Products Report, released yesterday, that helped fuel the fire. Cheddar cheese output in March came in below expectations, down 3.2% vs. a year ago and below 2017 levels as well.

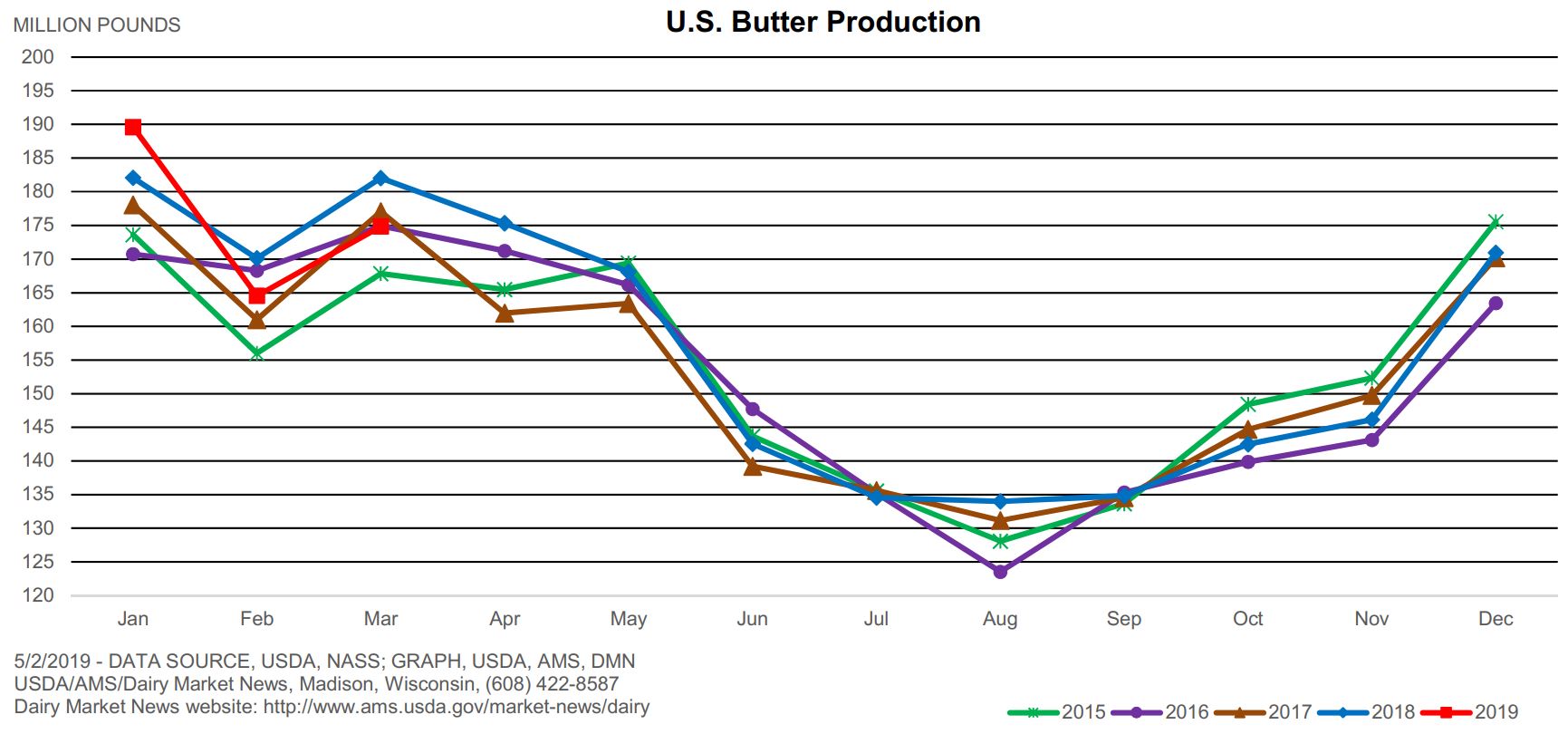

March butter production also came in under expectations, declining 3.9% vs. March 2018.

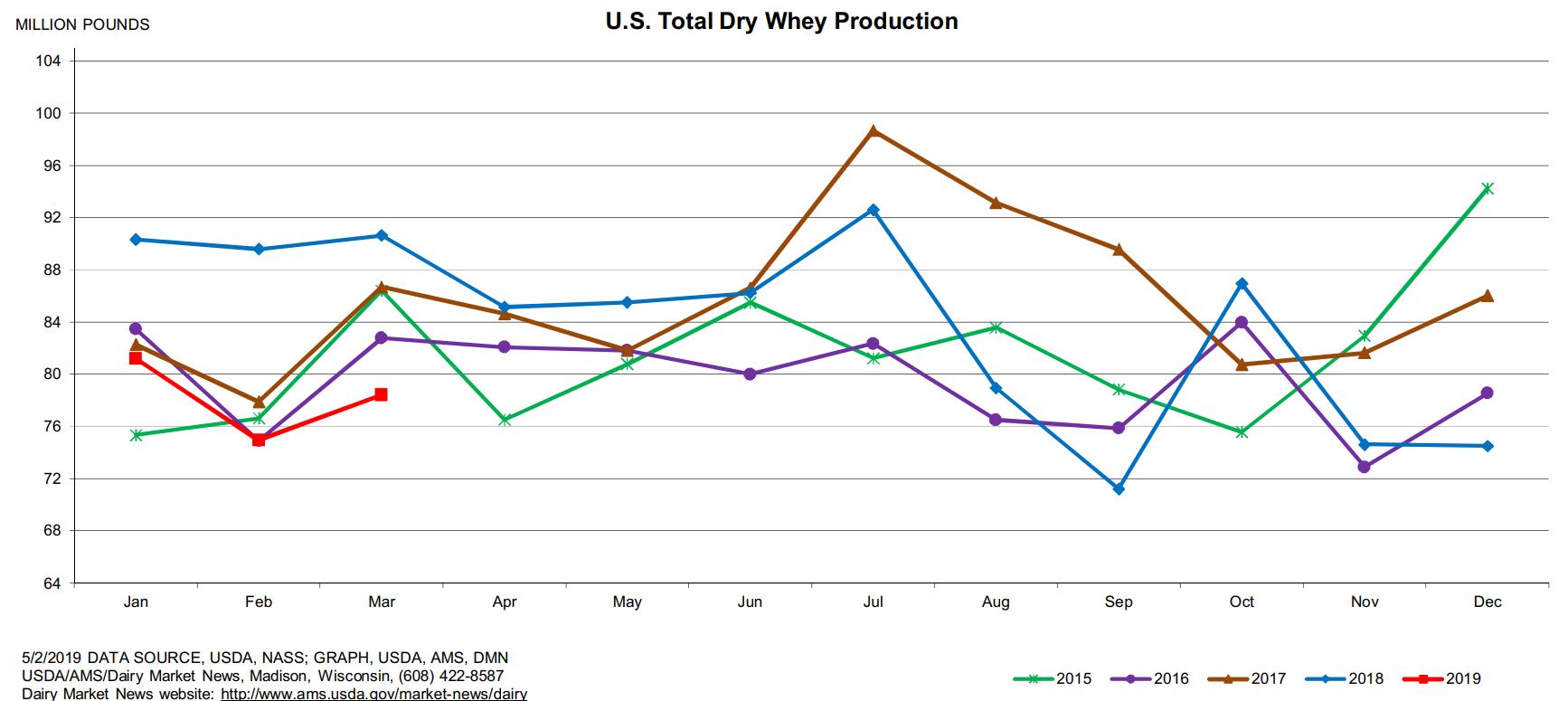

Dry whey output plunged 14.2% compared to a year ago, but stocks on hand actually increased 5.5% due to the drop in demand from African swine flu.

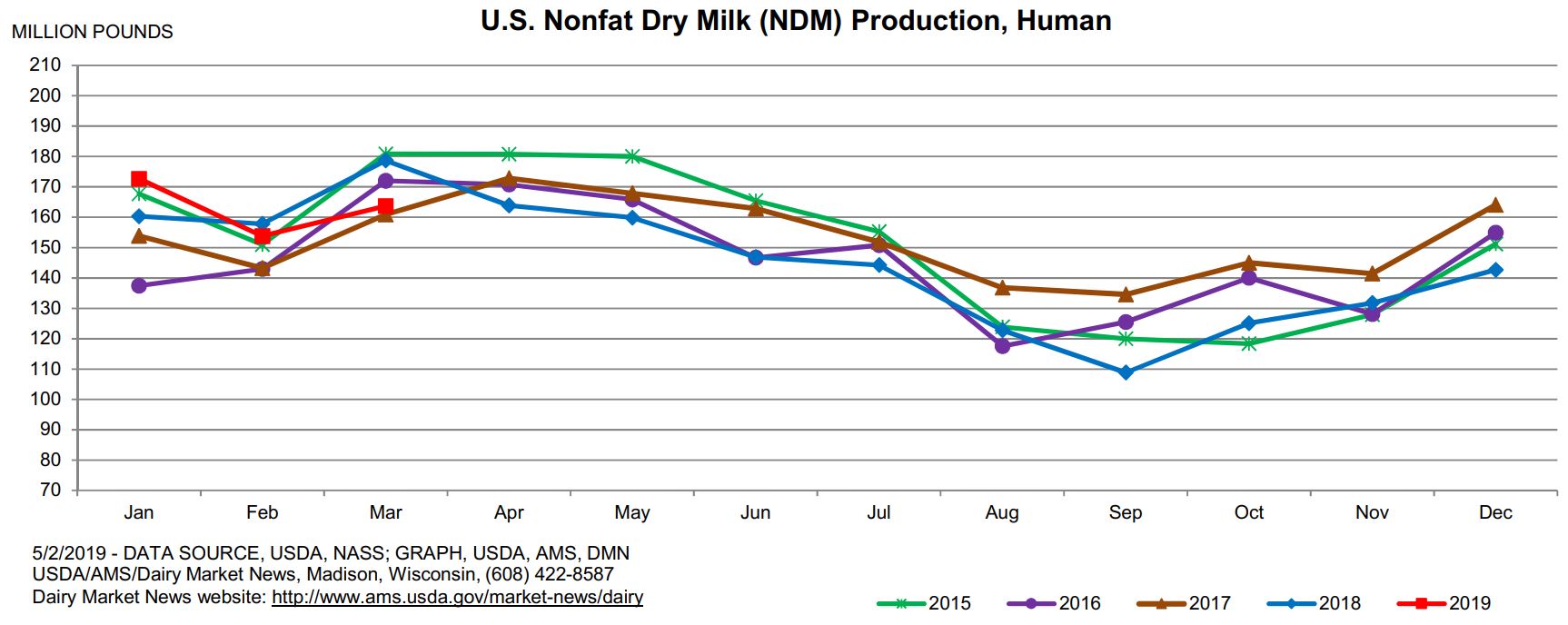

Finally, NDM output in March fell 8% compared to last March, while stocks at the end of the month were down 2.9%.

Weekly dairy cow slaughter numbers totaled 61,000 head, up 2% vs. a year ago, but there seems to be a tapering off after seeing seven consecutive weeks at 70k+ earlier this year. We’ll need to watch the milk cows number in future Milk Production Reports to see if the decline is tapering, especially considering the higher milk prices out there now will be encouragement enough for some to hang on. Dairy Market News updates this week continue to paint a picture of improving milk production over much of the country, but at flush levels below prior years, and nothing that seems will stress processing capacity. Spot milk prices are still not being steeply discounted as has happened the prior 2-3 years, with some loads even being priced at a premium. Cheese inventories are building slightly with the improved milk output, but cheese demand is good, especially in the East. NDM updates this week leaned bullish, with some talk of prices heading into the $1.10s. Futures prices are already headed in that direction. Dry whey continues to languish on weak demand, but most of the info related to the swine flu virus is already baked in to the market and prices have stabilized. Spot dry whey actually gained 2 cents this week. With the decline in dry whey output, the market might be putting itself in better balance. There was a lot of trade talk this week in Washington, with hopes that a deal with China would be done within two weeks. We’ll wait to see it actually happen, but it could be a helpful development to the Ag markets. Very wet weather is hitting much of the grain belt, with the potential for further delays in planting. Watch corn prices as some of those acres may end up going to beans or left vacant. Finally, encouraging economic statistics were released this week, pushing the stock market higher. With an economy that appears to be strong and the lowest unemployment since 1969, consumers may be encouraged to open their pocketbooks further at restaurants and food service outlets. Technically, the market is overbought and due for a correction, but that doesn’t mean it won’t keep going higher. However, producers should begin to ask themselves how high is realistic? We’re already pricing $1.78 this fall. Are we headed to $1.90? $2.00? Higher? For those that have little to nothing hedged, perhaps prices north of $17.50 Class III should be a starting point to either sell or buy PUT options. Don’t wait until it’s too late! Have a great weekend!