04/12/2019

Barrel buyers purchased 19 loads Mon-Thur, then bought another 20 loads on Friday. The aggressive bidding closed the block/barrel spread to just 2¾¢.

Spot Market Recap

| Spot Product | 4/5 | 4/12 | Change |

| Cheddar Blocks | $1.6600 | $1.6450 | ($0.0150) |

| Cheddar Barrels | $1.5750 | $1.6175 | $0.0425 |

| Butter | $2.2700 | $2.2575 | ($0.0125) |

| Grade A NDM | $0.9875 | $0.9875 | $0.0000 |

| Dry Whey | $0.3450 | $0.3575 | $0.0125 |

Spot Market Trade Volume

The block/barrel average gained a penny for the week, settling at $1.63/lb. We’ve been watching this chart for the past few weeks. After rejecting the $1.68/lb level three times (red circle), it is definitely an area of established resistance (horizontal orange line). However, over the past two weeks (last two green bars), it’s retested the blue downtrend line and appears to have bounced off of it. These are small bars to be sure, but considering the aggressive barrel bidding we saw this week, it could mean a 4th attempt at breaking above resistance is in the works. Watch this space!

Class III futures had a weaker tone much of the week, but with the spot cheese average moving slightly higher, the front months closed out the week higher, with small losses seen further out. Despite spot dry whey finishing the week higher, dry whey futures continued their downward trend.

Futures Recap

| Futures Month | Class III 04/05 | Class III 04/12 | Change | Cheese 04/05 | Cheese 04/12 | Change | Dry Whey 04/05 | Dry Whey 04/12 | Change |

| Apr-19 | $15.85 | $15.92 | $0.07 | $1.634 | $1.644 | $0.010 | 39.250¢ | 38.875¢ | (0.375¢) |

| May-19 | $15.76 | $15.78 | $0.02 | $1.628 | $1.634 | $0.006 | 38.725¢ | 38.350¢ | (0.375¢) |

| Jun-19 | $15.87 | $15.83 | ($0.04) | $1.640 | $1.643 | $0.003 | 38.050¢ | 37.600¢ | (0.450¢) |

| Jul-19 | $16.14 | $16.12 | ($0.02) | $1.672 | $1.673 | $0.001 | 37.675¢ | 37.500¢ | (0.175¢) |

| Aug-19 | $16.39 | $16.33 | ($0.06) | $1.695 | $1.695 | $0.000 | 37.700¢ | 37.475¢ | (0.225¢) |

| Sep-19 | $16.56 | $16.51 | ($0.05) | $1.710 | $1.709 | ($0.001) | 38.425¢ | 38.000¢ | (0.425¢) |

| Oct-19 | $16.55 | $16.51 | ($0.04) | $1.710 | $1.713 | $0.003 | 38.000¢ | 37.825¢ | (0.175¢) |

| Nov-19 | $16.44 | $16.40 | ($0.04) | $1.699 | $1.704 | $0.005 | 38.000¢ | 37.900¢ | (0.100¢) |

| Dec-19 | $16.30 | $16.23 | ($0.07) | $1.683 | $1.690 | $0.007 | 38.000¢ | 37.600¢ | (0.400¢) |

| Jan-20 | $15.90 | $15.99 | $0.09 | $1.664 | $1.670 | $0.006 | 37.625¢ | 37.625¢ | 0.000¢ |

| Feb-20 | $15.88 | $15.96 | $0.08 | $1.655 | $1.662 | $0.007 | 38.000¢ | 38.000¢ | 0.000¢ |

| Mar-20 | $15.88 | $15.97 | $0.09 | $1.658 | $1.661 | $0.003 | 37.900¢ | 37.900¢ | 0.000¢ |

| 12 Mo Avg | $16.13 | $16.13 | $0.00 | $1.671 | $1.675 | $0.004 | 38.113¢ | 38.000¢ | (0.112¢) |

Cream is tightening across the country, as ice cream manufacturing starts to compete for available supplies, but that didn’t help butter futures this week. All contracts finished lower. Powders continued to be dragged lower as well.

| Futures Month | Butter 04/05 | Butter 04/12 | Change | Class IV 04/05 | Class IV 04/12 | Change | NDM 04/05 | NDM 04/12 | Change |

| Apr-19 | 228.300¢ | 227.725¢ | (0.575¢) | $15.90 | $15.87 | ($0.03) | 97.700¢ | 96.900¢ | (0.800¢) |

| May-19 | 229.750¢ | 228.525¢ | (1.225¢) | $16.22 | $16.14 | ($0.08) | 100.800¢ | 101.050¢ | 0.250¢ |

| Jun-19 | 231.750¢ | 230.500¢ | (1.250¢) | $16.55 | $16.43 | ($0.12) | 103.775¢ | 103.150¢ | (0.625¢) |

| Jul-19 | 233.500¢ | 232.325¢ | (1.175¢) | $16.73 | $16.63 | ($0.10) | 105.375¢ | 104.700¢ | (0.675¢) |

| Aug-19 | 234.850¢ | 233.950¢ | (0.900¢) | $16.89 | $16.80 | ($0.09) | 106.800¢ | 105.700¢ | (1.100¢) |

| Sep-19 | 235.075¢ | 234.600¢ | (0.475¢) | $16.98 | $16.89 | ($0.09) | 107.300¢ | 106.750¢ | (0.550¢) |

| Oct-19 | 233.625¢ | 233.325¢ | (0.300¢) | $17.04 | $16.95 | ($0.09) | 108.300¢ | 107.200¢ | (1.100¢) |

| Nov-19 | 231.625¢ | 231.450¢ | (0.175¢) | $16.94 | $16.89 | ($0.05) | 109.000¢ | 108.400¢ | (0.600¢) |

| Dec-19 | 227.525¢ | 227.300¢ | (0.225¢) | $16.82 | $16.80 | ($0.02) | 109.550¢ | 109.100¢ | (0.450¢) |

| Jan-20 | 222.850¢ | 222.000¢ | (0.850¢) | $16.58 | $16.63 | $0.05 | 109.775¢ | 110.500¢ | 0.725¢ |

| Feb-20 | 221.600¢ | 220.700¢ | (0.900¢) | $16.60 | $16.60 | $0.00 | 110.500¢ | 111.400¢ | 0.900¢ |

| Mar-20 | 222.475¢ | 221.000¢ | (1.475¢) | $16.60 | $16.70 | $0.10 | 110.825¢ | 112.000¢ | 1.175¢ |

| 12 Mo Avg | 229.410¢ | 228.617¢ | (0.794¢) | $16.65 | $16.50 | ($0.15) | 106.642¢ | 106.404¢ | (0.237¢) |

Fluid Milk Output

Milk production in the Northeast is increasing seasonally, with many balancing plants at or near full capacity. In the Mid-Atlantic, milk output is also on the rise, but most processors in the region are not at capacity. Milk is being shipped out of the region, which is keeping balancing plants on lighter schedules. In the Southeast, the increase in milk production has not been enough to fulfill production needs, thus milk from other parts of the country are being imported. Class I sales are up, with some bottlers requesting additional milk. Cream availability has tightened in the region due to improved demand. Class II operations are pulling strong cream orders. In the Central region, individual farms are reporting increases in milk output, but processors are reporting a net decline in milk receipts due to more and more farm closures. Spot loads of milk were reported at $1 over to $2 under Class III, compared to $2 under to $3.50 under Class III last week. Moving West, California processing plants report milk receipts are steady this week. Despite strong milk production throughout the state, handlers have been able to find homes for the milk. Arizona milk output is trending higher, as are components. Milk handlers have so far been able to manage all the milk within the state. Milk output is steady to lower in New Mexico, with no surplus milk reported. Finally, in the Pacific Northwest, milk production is moving higher along seasonal patterns. Supply and demand seem to be in good balance.

Butter

Butter output in the Northeast has been somewhat constrained this week, as Class II production has limited surplus volumes of cream. Retail butter demand is good, as print orders have strengthened. Manufacturers in the Central region are taking notice of the increase in cream prices. Some churners are not as full as they would like to be, and an number of plant managers are out looking for additional cream. Domestic demand is meeting expectations, while export demand has been strong. Inventories are in good balance. Western butter demand is increasing as bakers prepare for spring sales. Butter output is mixed, with some areas seeing tighter cream supplies due to increased Class II usage.

Dry Whey

Eastern dry whey prices were steady this week. Demand is mixed, with stronger orders for ice cream production, but lower bids from other buyers. There are reports that export demand has improved from Mexico, but African swine fever is still affecting international trade. Large inventories in the Central region continue to limit price increases. A growing number of end users suggest their warehouses are near capacity. Domestic demand for Western dry whey is decent, but export demand continues to lag. The 20% reduction in the Chinese pig herd has cut deeply into export opportunities.

Nonfat Dry Milk

As milk output increases, NDM production in the Northeast is stronger, resulting in growing inventories. Prices were firmer this week, but that is not expected to last. Central region producers reported increased buyer interest this week. Prices were pushed to levels not seen in recent weeks. Inventories are available, but producers report both April and May orders are stronger than expected, lending a bullish tone to the market in the near term. Offers direct from manufacturers are currently limited. Western NDM output is active, with dryers running on mostly full schedules. Stocks are building due to demand not keeping up.

Cheese

Cheese output in the Northeast ranges from steady to robust. Inventories are stable to growing, but domestic cheese interest is very good. In the Midwest, some manufacturers are running on 7-day schedules, but demand is booming for curd producers, who report very strong April/May orders. Inventories are in good balance. Western cheese makers say demand is mixed. Some report retail and food service accounts are increasing their orders slightly, but others report demand has been slow. Some processors are trying to limit cheese output in order to control inventories. Cheese stocks remain heavy in the region.

Commentary

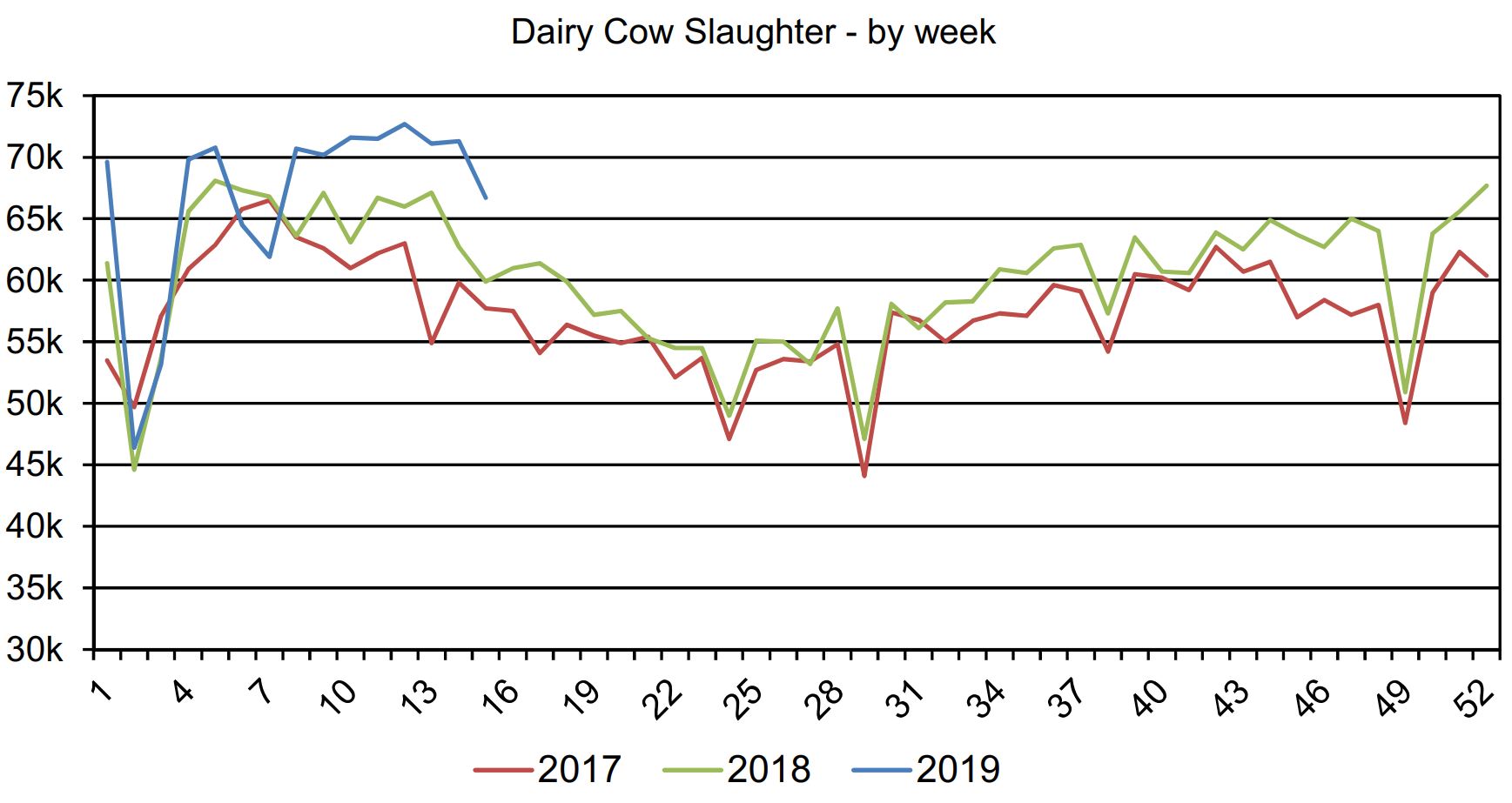

Dairy cow slaughter fell below 70k for the first time in several weeks, but was still up 11.4% vs. the same period a year ago.

With reports of cream beginning to tighten, continued farm closures, strong culling, easily handled spring flush levels and strong cheese demand, the downside for Class III milk prices seems to be somewhat limited. Prices tried to retrace early in the week as blocks lost some ground, but came off their lows by the end of the week. We could see more two-sided trade and price consolidation (both higher and lower) in the weeks to come as we progress through peak production time in the U.S. However, with Oceania’s season complete and limited gains in the EU, global milk output is quite flat. Now if we could only get some trade deals in place and contain the African swine virus, we might see powder prices increase as well. Current spot prices work out to about $15.90 Class III. Adding USDA survey price basis brings it well above $16. With May Class III futures beginning its pricing period as early as next week, further stability or even increases in spot cheese prices could get the front months moving higher. Producers looking to hedge should consider cheap PUT options up front, while avoiding locking in milk July 2019 and beyond.

NOTE: Markets will be closed next Friday in observance of Good Friday.