04/05/2019

Block cheese gained a little while barrels lost a little in this week’s spot market, leaving the block/barrel average unchanged from a week ago at $1.62/lb. So, while we weren’t able to retest the $1.70 level again, we also didn’t collapse as both buyers and sellers were active.

Spot Market Recap

| Spot Product | 3/29 | 4/5 | Change |

| Cheddar Blocks | $1.6450 | $1.6600 | $0.0150 |

| Cheddar Barrels | $1.6025 | $1.5750 | ($0.0275) |

| Butter | $2.2550 | $2.2700 | $0.0150 |

| Grade A NDM | $0.9625 | $0.9875 | $0.0250 |

| Dry Whey | $0.3225 | $0.3450 | $0.0225 |

Spot Market Trade Volume

With spot cheese largely holding steady and gains in other spot Class III components, Class III futures benefited mainly up front, where they continue to trade at a discount to spot. Current spot prices work out to about $15.80 Class III. Given the positive NDPSR survey basis, we’re well above $16.00. Futures continue to disbelieve, however. With April almost fully priced and May about to begin pricing, should spot cheese hold or go higher, May Class III could see a decent jump. But with spot cheese hitting a wall this week, we may very well be in for at least a moderate correction.

Futures Recap

| Futures Month | Class III 03/29 | Class III 04/05 | Change | Cheese 03/29 | Cheese 04/05 | Change | Dry Whey 03/29 | Dry Whey 04/05 | Change |

| Apr-19 | $15.61 | $15.85 | $0.24 | $1.617 | $1.634 | $0.017 | 38.500¢ | 39.250¢ | 0.750¢ |

| May-19 | $15.48 | $15.76 | $0.28 | $1.600 | $1.628 | $0.028 | 38.450¢ | 38.725¢ | 0.275¢ |

| Jun-19 | $15.67 | $15.87 | $0.20 | $1.625 | $1.640 | $0.015 | 37.500¢ | 38.050¢ | 0.550¢ |

| Jul-19 | $16.04 | $16.14 | $0.10 | $1.659 | $1.672 | $0.013 | 37.500¢ | 37.675¢ | 0.175¢ |

| Aug-19 | $16.26 | $16.39 | $0.13 | $1.684 | $1.695 | $0.011 | 37.575¢ | 37.700¢ | 0.125¢ |

| Sep-19 | $16.50 | $16.56 | $0.06 | $1.703 | $1.710 | $0.007 | 38.250¢ | 38.425¢ | 0.175¢ |

| Oct-19 | $16.48 | $16.55 | $0.07 | $1.704 | $1.710 | $0.006 | 38.000¢ | 38.000¢ | 0.000¢ |

| Nov-19 | $16.34 | $16.44 | $0.10 | $1.694 | $1.699 | $0.005 | 38.000¢ | 38.000¢ | 0.000¢ |

| Dec-19 | $16.23 | $16.30 | $0.07 | $1.679 | $1.683 | $0.004 | 38.000¢ | 38.000¢ | 0.000¢ |

| Jan-20 | $15.85 | $15.90 | $0.05 | $1.660 | $1.664 | $0.004 | 37.375¢ | 37.625¢ | 0.250¢ |

| Feb-20 | $15.80 | $15.88 | $0.08 | $1.658 | $1.655 | ($0.003) | 38.000¢ | 38.000¢ | 0.000¢ |

| Mar-20 | $15.77 | $15.88 | $0.11 | $1.650 | $1.658 | $0.008 | 38.000¢ | 37.900¢ | (0.100¢) |

| 12 Mo Avg | $16.00 | $16.13 | $0.12 | $1.661 | $1.671 | $0.010 | 37.929¢ | 38.000¢ | 0.071¢ |

| Futures Month | Butter 03/29 | Butter 04/05 | Change | Class IV 03/29 | Class IV 04/05 | Change | NDM 03/29 | NDM 04/05 | Change |

| Apr-19 | 228.750¢ | 228.300¢ | (0.450¢) | $15.88 | $15.90 | $0.02 | 97.100¢ | 97.700¢ | 0.600¢ |

| May-19 | 230.700¢ | 229.750¢ | (0.950¢) | $16.12 | $16.22 | $0.10 | 98.900¢ | 100.800¢ | 1.900¢ |

| Jun-19 | 233.750¢ | 231.750¢ | (2.000¢) | $16.43 | $16.55 | $0.12 | 100.900¢ | 103.775¢ | 2.875¢ |

| Jul-19 | 234.800¢ | 233.500¢ | (1.300¢) | $16.55 | $16.73 | $0.18 | 102.350¢ | 105.375¢ | 3.025¢ |

| Aug-19 | 236.200¢ | 234.850¢ | (1.350¢) | $16.65 | $16.89 | $0.24 | 103.500¢ | 106.800¢ | 3.300¢ |

| Sep-19 | 236.300¢ | 235.075¢ | (1.225¢) | $16.76 | $16.98 | $0.22 | 104.825¢ | 107.300¢ | 2.475¢ |

| Oct-19 | 234.375¢ | 233.625¢ | (0.750¢) | $16.74 | $17.04 | $0.30 | 104.975¢ | 108.300¢ | 3.325¢ |

| Nov-19 | 233.100¢ | 231.625¢ | (1.475¢) | $16.75 | $16.94 | $0.19 | 106.425¢ | 109.000¢ | 2.575¢ |

| Dec-19 | 229.150¢ | 227.525¢ | (1.625¢) | $16.65 | $16.82 | $0.17 | 106.250¢ | 109.550¢ | 3.300¢ |

| Jan-20 | 223.250¢ | 222.850¢ | (0.400¢) | $16.55 | $16.58 | $0.03 | 108.000¢ | 109.775¢ | 1.775¢ |

| Feb-20 | 222.500¢ | 221.600¢ | (0.900¢) | $16.55 | $16.60 | $0.05 | 108.275¢ | 110.500¢ | 2.225¢ |

| Mar-20 | 223.500¢ | 222.475¢ | (1.025¢) | $16.50 | $16.60 | $0.10 | 108.350¢ | 110.825¢ | 2.475¢ |

| 12 Mo Avg | 230.531¢ | 229.410¢ | (1.121¢) | $16.51 | $16.50 | ($0.01) | 104.154¢ | 106.642¢ | 2.488¢ |

Fluid Milk Output

Temperatures are rising in the Northeast, leading to improved milk output on some farms, while other farms are seeing slight decreases. Class I sales are higher this week and Class III plants are running at or near capacity. Balancing plants in the region are receiving fewer milk loads than last week. Milk output is steady in the Mid-Atlantic, but plants in this region are not running at capacity. Weather has improved in parts of the Southeast and milk production is up slightly. Some manufacturers are below capacity, so milk is being brought in from other parts of the U.S. to meet processing needs. Schools are back in session, bringing with it improved Class I demand. Output in Florida has been flat now for several weeks.

Spring flush has started in the southern reaches of the Central region, while farms in the upper-Midwest are still going out of business at a rapid pace. Low milk prices, poor cull cow prices, higher feed costs and the potential for feed/hay loss due to flooding are all weighing on those still trying to make it. Spot loads of milk are still available at a discount, ranging down to $1.25 below Class III. Cream prices are firming as demand has increased for holiday items, while at the same time ice cream makers are starting to ramp up production.

In the West, milk production has been strong in California so far this spring. However, there is a good balance between the milk supply and current demand. Manufacturers are running on full schedules. The milk yield is moving higher in Arizona as weather conditions remain favorable for cow comfort. Contacts don’t expect any problems handling this year’s spring flush output. Milk output has increased substantially in New Mexico this week, but processors so far have been able to absorb most of the supply. Class I orders are down but demand for Class II and III is trending higher.

Milk production is not increasing as much as expected in the Pacific Northwest. Class I demand is solid and milk intakes are in good balance with processing needs. Some manufacturers are taking in a few extra loads of milk as they have added processing capacity.

Butter

Holiday butter purchases have wrapped up, so churning rates in the Northeast are moderating. Evenso, Class II cream utilization is on the rise as other product categories begin to need more cream. Cream availability in the Central region varies from light, to sufficient to plentiful. Similarly, churning rates vary along with availability. Demand remains strong ahead of the spring holidays. Western butter demand is strong as spring baking and holidays are around the corner. Bulk butter interest is also decent. Some end users are putting butter in storage to guarantee future needs can be met. A few contacts have suggested that cream has tightened considerably over the last couple weeks. Class II processors have started ramping up production and are soaking up any extra loads of cream.

Dry Whey

Buying and selling is even-handed this week in the East, though there is some downward pressure in the form of weaker demand. Powder production is steady and supplies are adequate for contracted needs. In the Central region, the market is described as steady, for now. But inventories are expected to build shortly as cheese production is beginning to increase. The West continues to be plagued by low exports and a slowdown in domestic demand. However, supplies are in balance with demand. Dry whey output is active, though some manufacturers are shifting towards higher WPCs.

Nonfat Dry Milk

Inventories are outweighing demand somewhat in the East, according to contacts. Manufacturers are drying on full schedules. Buyers in the Central region are hesitant to make purchases in the spot market. They sense weakness in the market, especially if there is a disruption at the US/Mexican border. A blockage would be very bearish indeed. Manufacturers, however, are more upbeat due to recent strength in the GDP auction, so they are holding offers in the high $0.90s. Western NDM prices were up slightly this week, in response to global price support. The market tone has improved with robust demand from cheese plants, bakers and confectioners. Some market participants are expecting a price dip soon, however, in light of large (and building) stocks, spring flush and full balancing plants.

Cheese

With milk production increasing seasonally and weather improving, cheese output is strong in the Northeast. Cheddar and Italian supplies are balanced to growing, but domestic demand is very good. Pizzerias have sold orders while grilling season is approaching. In the Midwest, cheesemakers indicate demand is improving with the warming weather. There is still plenty of cheese available, but inventories at some plants have been held in check due to lower production in the winter. Cheese contacts view the current market as leaning bullish. Cheese offers are abundant in the West and manufactures have plenty of supply on hand. Strong milk output is keeping cheese processing stable, though some manufacturers are trying to refrain from making too much cheese. Export and domestic sales are slightly higher this week, with demand improving for both blocks and barrels.

International

Cheese demand in Germany is very strong from both retailers and large consumers. Requests for cheese from with and outside the EU are strong as well. Cheese inventories are adequate, but there are very limited loads available for spot sales. Cheese output is active, but unable to increase enough to grow supplies.

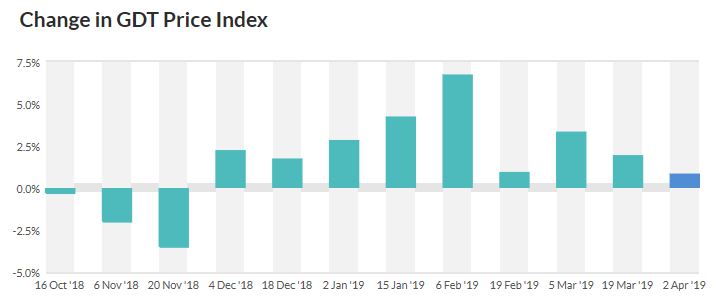

With the milking season ending in Oceania, this week’s GDT auction saw the price index rise 0.8%.

Both butter and butter milk powder saw decent gains, while cheddar cheese was up 3.2% to a U.S. equivalent $1.93/lb.

Source: Global Dairy Trade

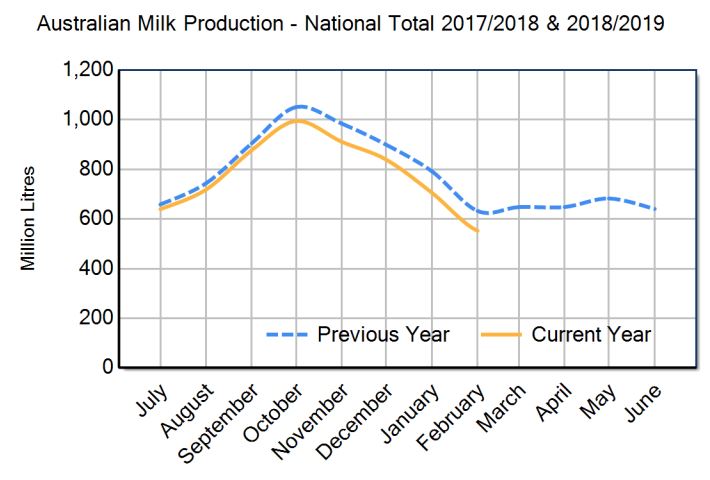

Finally, Dairy Australia released milk production numbers for February. Output was sharply lower, down 12.6% compared to a year ago. That brings their current milking season (July-Feb) 6.4% below the prior season.

Commentary

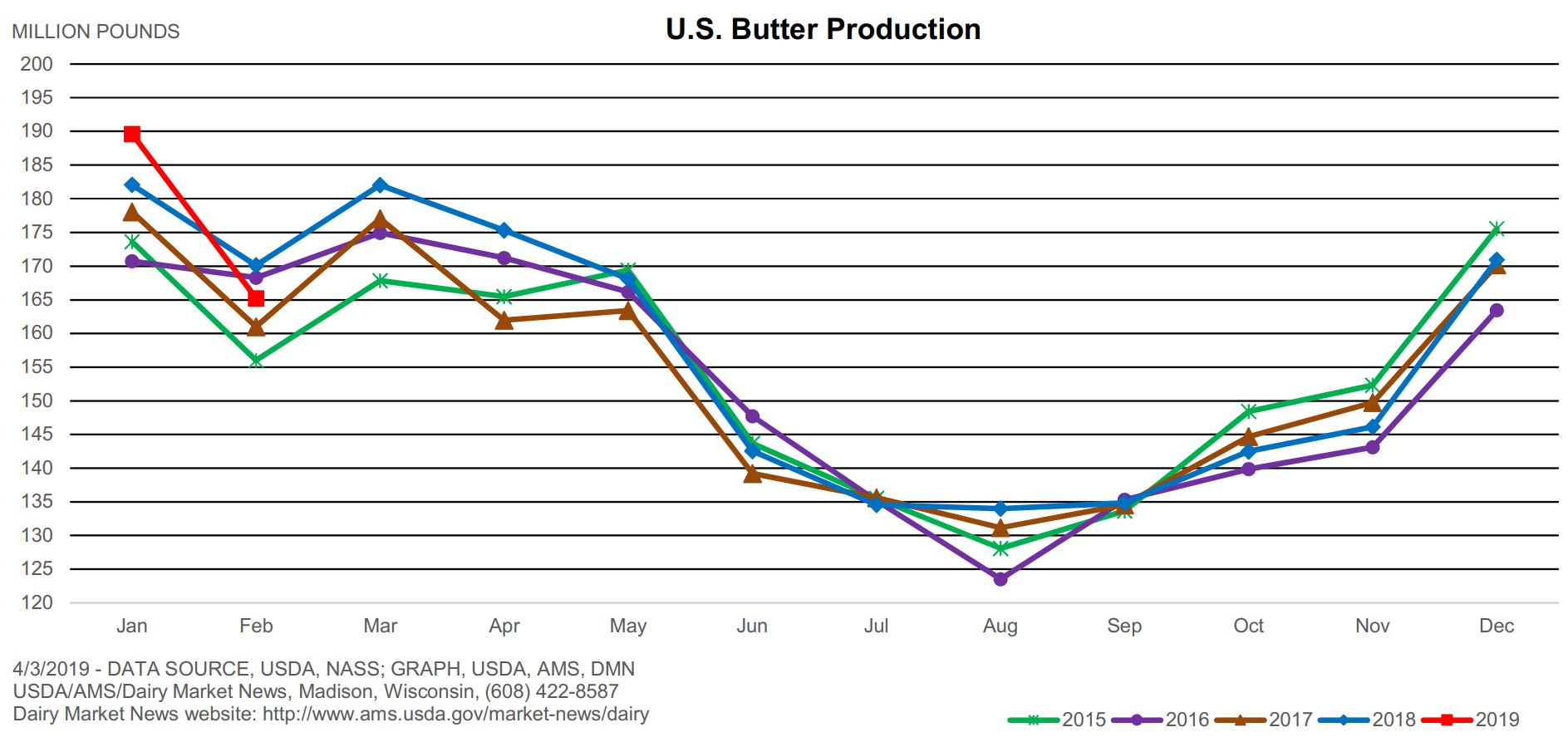

USDA released a Dairy Products Report this week, and it contained a few surprises. Cheddar cheese output in February was down 4.3% compared to a year ago.

Total cheese output was only able to manage a small 0.5% increase over the same period. Meanwhile, butter output was down 2.9% YoY.

Powders lost ground too. U.S. total dry whey output fell 16.4% vs. Feb 2018.

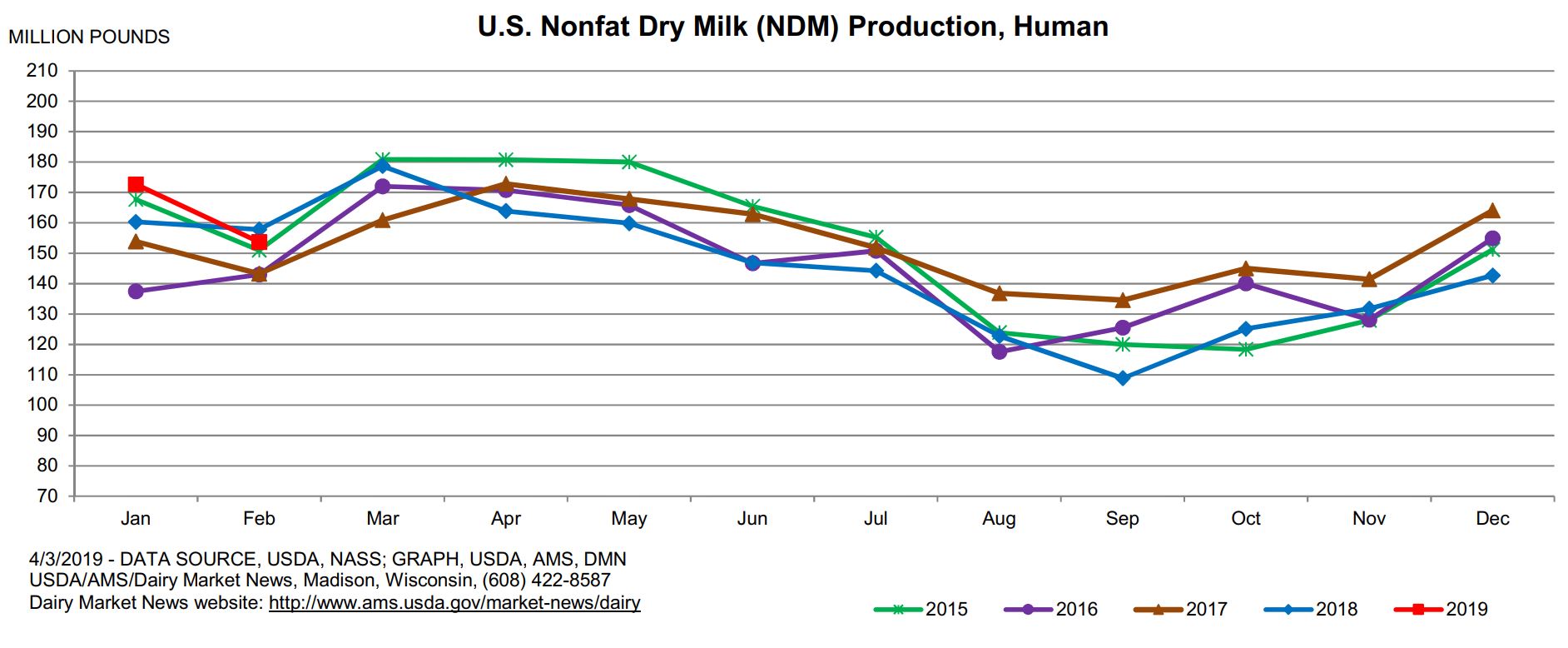

Finally, NDM output declined a more modest 2.6%

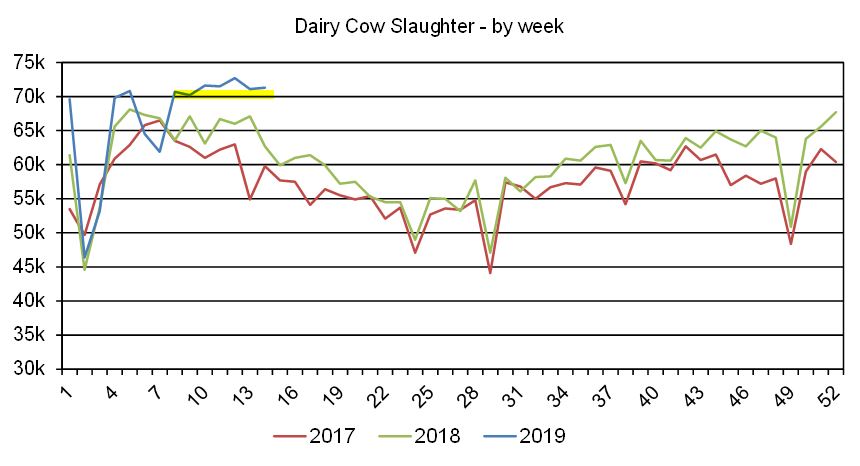

Winter was harsh in February in northern parts of the U.S., which may be part of the reason for the declines, but record culling is a more probable explanation. Weekly numbers continue to impress, with 71,300 head exiting the herd for the week ending 03/23. That’s a 13.7% increase over the same period a year ago, and the 7th consecutive week we’ve been above 70,000 head. The Livestock Slaughter Report for March is due out on April 25th, and looks to be another record setter.

With a move higher in this week’s GDT auction (and strong cheddar price), U.S. dairy product output declining and continued strong slaughter numbers, the longer term outlook remains supported in our opinion. That doesn’t mean we can’t head lower in the near term. Certainly barrel sellers were more aggressive this week and there is plenty of milk for processing as the northern parts of the U.S. head into peak output season. The American consumer continues to drift away from fluid milk consumption, and alternative dairy products are making inroads into diets. The threat of a border closure with Mexico could potentially send shockwaves through the dairy sector, although it seems unlikely to happen. Apparently progress is being made in Chinese/American trade negotiations. Finalization of terms could jumpstart exports to China, which are badly needed. Milk output globally continues to struggle, with dramatically lower production numbers out of Australia, production below year-ago levels in Argentina and Uruguay, mainly flat in the EU and possibly going negative in the coming months in the U.S. Dairy Market News weekly updates summarized above paint a picture of improving cheese demand. We think the stage is set for higher prices longer term. Dairy operations should be locking in their input costs. Crude oil made a 5½-month high this week and further strengthening could help both soybeans and corn head higher due to their biodiesel/ethanol component. We would not be aggressive sellers of milk July-Dec, nor any at all in the 2020 months. Once warmer to hotter weather is established across the countrt and national milk production is past its peak, things could get interesting. A lot of producers have been utilizing the Dairy RP program to establish a floor price for their milk, and that’s great. However, the levels available on a quarterly basis are not that high. With milk prices appearing to have more upside potential than downside, many of these contracts could end up not paying anything to the producer. We believe we can establish higher levels of protection at a competitive cost using option strategies. Give us a call to discuss how we can help your farm stay profitable! Have a great weekend!