1/21/2024

Sad day for the cheese heads out there as an exciting season came to an end. A bit like the cheese market, there is plenty of promise out there for higher cheese prices. Lower milk production and higher prices in the rest of the major milk producing areas of the world. A solid jobs reports and stable economy here in the US. Flat to lower milk production for the last 6 months. Unfortunately that has not resulted in higher prices. Tepid domestic demand has been the Achilles heel for prices through four quarter of last year into this year. There has been some opportunities to lock in good prices on a few rallies, but these have all been short lived.

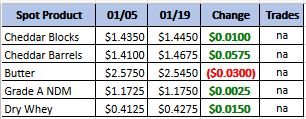

Weekly Spot Prices

Weekly Future Prices

Cheese: Winter weather again affected dairy operations in the eastern states. Some milk volumes intended for Class III processing were redirected into bottling for grocery retailers. Cheese plant managers relay lighter production schedules have not affected inventories. In the Central region, winter weather also proved to be an obstacle to cheesemakers. Milk is readily available, but cheese production schedules are lighter due to weather. Spot milk prices were reported at $7 to $0.50 under Class III. Inventories in the region are comfortable, and demand is seasonally steady. Retail cheese demand has flattened in the West. Milk volumes are readily available for Class III processing. Some transportation delays and disruptions were reported, but some contacts relayed they were able to acquire spot milk loads below Class III pricing. Cheese inventories are steady to stronger. Export demand has strengthened as domestic cheese prices become more competitive. (USDA Cheese Highlights)

Butter: Retail and bulk butter demands are steady throughout most of the country. That said, demand from domestic and international buyers is noted as steady to moderate for the Western region. Weak food service demand continues to be noted for the Eastern region. Stakeholders say unsalted butter availability is tighter. Cream loads are readily available, and some Central region cream handlers say finding homes has been an uphill battle. Butter production is mixed. Some butter makers are running stronger, seven-day-a-week production. However, some butter makers are running lighter production schedules due to weather-related setbacks or planned machine maintenance. Bulk butter overages range from 1 to 8 cents above market, across all regions. (USDA Butter Highlights)

Dry Whey: Prices moved slightly higher on both ends of the range. The mostly price series is unchanged. A few manufacturers note Grade A dry whey availability is tight for spot buyers. Some stakeholders indicate offered loads of downgraded dry whey have increased recently. Demand is steady domestically for both preferred and nonpreferred brand loads. Export demand is moderate with no big upticks from Mexican or Asian purchasers. In northern parts of the region icy conditions caused some transportation delays and disruptions. That said, manufacturers say impacts to steady dry whey production were minimal. Cheese making is providing ample

amounts of liquid whey to accommodate dry whey manufacturing needs. Industry sources indicate demand for high-protein whey products has strengthened, keeping some liquid whey out of the edible whey drying stream (USDA Dry Whey)

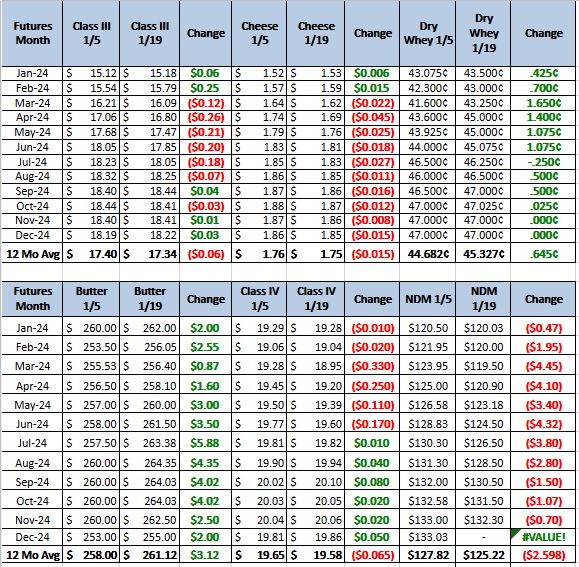

Looking at the March graph above the class 3 market is still in a bearish trend. Which means that technically it is still a sell. With the price well bellow cost of production in most of the country at this I am not recommending limiting the top. Recommendation: buy calls on sold positions and buy put spreads to limit the cost on option contracts. The chart is still saying the market is likely to go lower, but some of those promising fundamentals I mentioned in the beginning of this report should take effect. This market will turn at some point the million dollar question is when.