11/11/2023

The cheese market is showing some cracks as demand is still behind supply. Milk production is not increasing but cheese plant capacity is more then enough to overwhelm demand. Exports have continued to struggle as we are behind last year. Chinese continued economic problems have dragged down all commodities this year. With out this additional demand supply is out pacing demand even though domestic demand is strong.

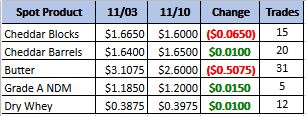

Weekly Spot Prices

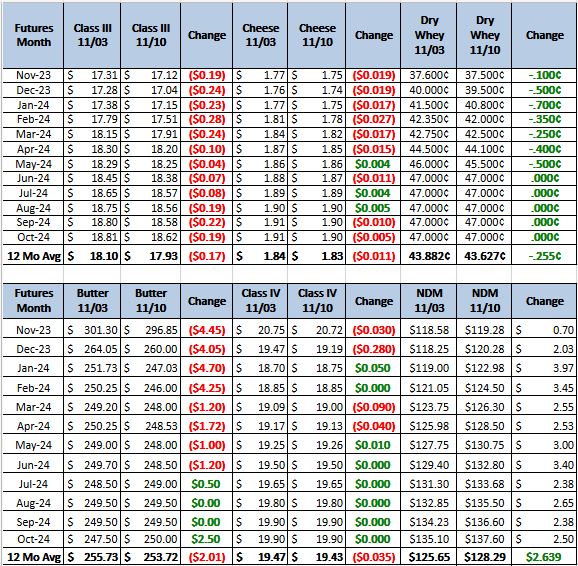

Weekly Future Prices

Cheese: In the Northeast, milk is steadily flowing into Class III production facilities. Contacts in the West report somewhat limited spot milk availability. Meanwhile in the Midwest, cheesemakers report an increase in milk offers late last week and over the weekend and relay spot milk prices around $1-over Class. Cheese production is steady in the West and Midwest, though some plant managers in the Midwest report maintenance/downtime this week. Cheese inventories in the Midwest are moving steadily. In the Northeast, contacts report growing cheese inventories. Domestic demand for cheese varies within the region, as contacts report stronger demand from the retail sector than from food service purchasers. Retail and food service sales are steady to moderate in the West, though export demand is said to be moderate to light. For those export markets, contacts in the region cite less than competitive pricing for domestically produced cheese compared to loads manufactured in the European Union/Oceania. (USDA Cheese Highlights)

Butter: Cream is becoming more available in all regions, and contacts in the Central region report multiples moving below the 1.20 market this week. In the East, butter production is mixed. Some butter makers in the Central region are micro-fixing to prevent inventories from building. Butter production is mixed in the West, as some processors say they have resumed churning, but others say they are waiting until after Thanksgiving to resume butter production. Contacts in the West say butter inventories are satisfactory ahead of the holiday season. Inventories of unsalted butter are more available than salted in the East, despite higher demand for holiday baking in the region. Demand for bulk butter has slowed, particularly from food service customers in the Central region, while retail demand is steady. In the West, retail butter demand is strong to steady. Bulk butter overages range from 3.0 to 10.0 cents over market value. (USDA Butter Highlights)

Dry Whey: The dry whey price series jumped higher at both ends of the range. Farm level milk outputs are increasing week over week, and cheese processing is steady. Liquid whey is available for drying. Contacts relay the strength of the whey protein concentrate market continues to influence the dry whey market. Inventories of dry whey are tightening. Some feed contacts share that their needs are being met through contracted loads. Spot activity is unchanged

U.S. DRY WHEY EXPORTS. 2023 Exports % Change From (Million Lb.) 1 Year Ago

SEPTEMBER Total 34.2 – 31

TOTAL, JAN – SEP 299.1 – 18

1 China 118.6 – 11

2 Canada 22.3 – 42

3 Philippines 21.6 + 29

4 Thailand 19.1 + 82

5 Vietnam 18.7 – 13

(USDA Dry Whey)

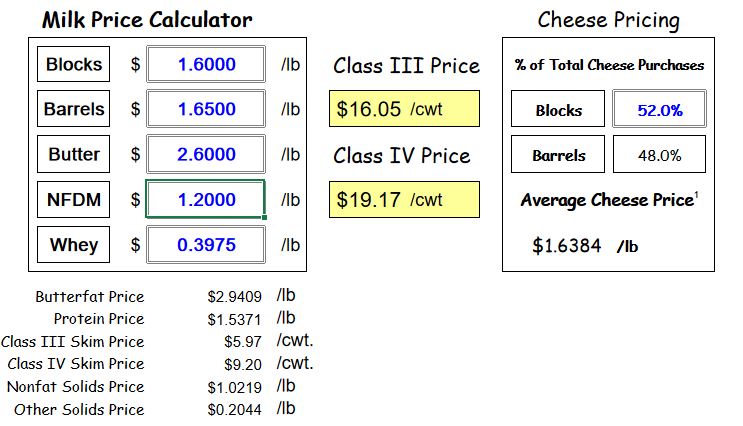

The cheese markets are starting to look a little weaker this week. As spot prices continue come in below future prices. Export demand is bellow last year and food service is starting to slow. Cow numbers are not growing and cost of production is still above future prices on average. Recommendation, Buy puts or sell and buy calls. This market could turn quickly on a little increase in demand, but at the present time production is out pacing demand. Give us a call for a more specific recommendation.