6/25/2023

Summer is here as New Mexico and Texas saw their first 100+ degree days. These temps are starting to knock down the milk production in these states, but the true over production is happening in the upper Midwest. There is nothing in the forecast for the heat to push that far north yet. With the cows still comfortable in the upper Midwest extra loads were still trading for as much as $11 under class.

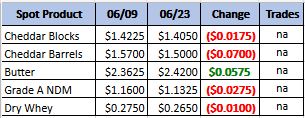

Weekly Spot Prices

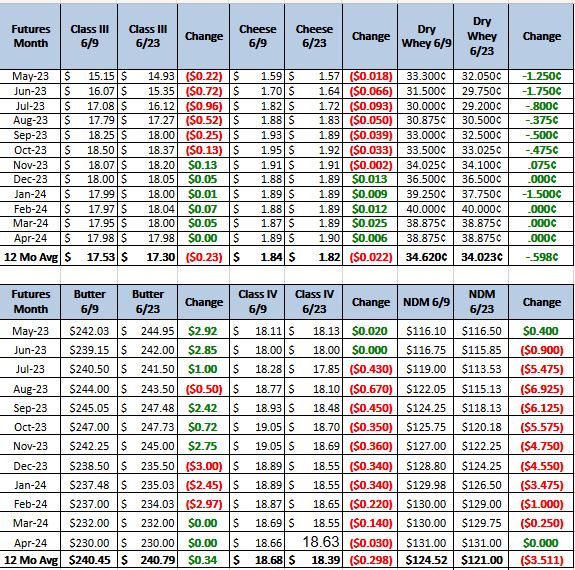

Weekly Future Prices

Cheese: Milk volumes are available for Class III production throughout all regions. In the Midwest, some milk suppliers are selling volumes to cheese plant to avoid disposal, and looking for the processors to cover freight costs. Contacts in the region continue to report spot loads of milk trading as low as $11 under Class. Cheesemakers in the Northeast say production steady, while contacts in the West say production is strong to steady. Retail and food service demands for cheese are steady in the West, though contacts report mixed demand from international purchasers. In the Midwest, cheesemakers say demand is trending higher. Cheese buyers in the Midwest are more willing to purchase inventories for storage with market prices for cheese at or below $1.50/lb. Cheese barrel inventories are tighter than blocks in the West, though stakeholders say loads of barrels and blocks are available to meet current demand. In the Northeast, cheese inventories are unchanged. (USDA Cheese Highlights)

Butter: Cream volumes are steady in the East and West. Eastern butter makers report strong demand for cream from ice cream makers but say that demand is lighter compared to previous years. Central region cream offers were quieter this week, though some contacts in the region anticipate increased cream availability in the coming weeks. Butter makers in the East and West are operating strong schedules. Some manufacturers in the East are operating seven days a week. Inventories in the region are ample, and some regional butter makers are freezing butter. In the Central and West regions, butter loads are available, though some western contacts report tighter unsalted bulk butter inventories. Demand for butter is moderate to steady in the West, and unchanged in the East. Butter sales are trending higher, following seasonal trends in the Central region. Bulk butter overages range from 0 to 10.75 cents over market value. (USDA Butter Highlights)

Dry Whey: Prices for dry whey are largely unchanged, contracting slightly for the range and mostly price series. Although some brand specific loads are holding more stable purchasing activity and comparatively higher prices, spot market activity and contracted sales are more moderate overall. Export demand is moderate to quieter. Supplies are available to meet current demand. Strong Class III milk volumes and strong to steady cheese production schedules are leaving plenty of liquid whey for drying. Dry whey production is steady. Daily CME prices below the $0.30/lb mark persisted through this week. (USDA Dry Whey)

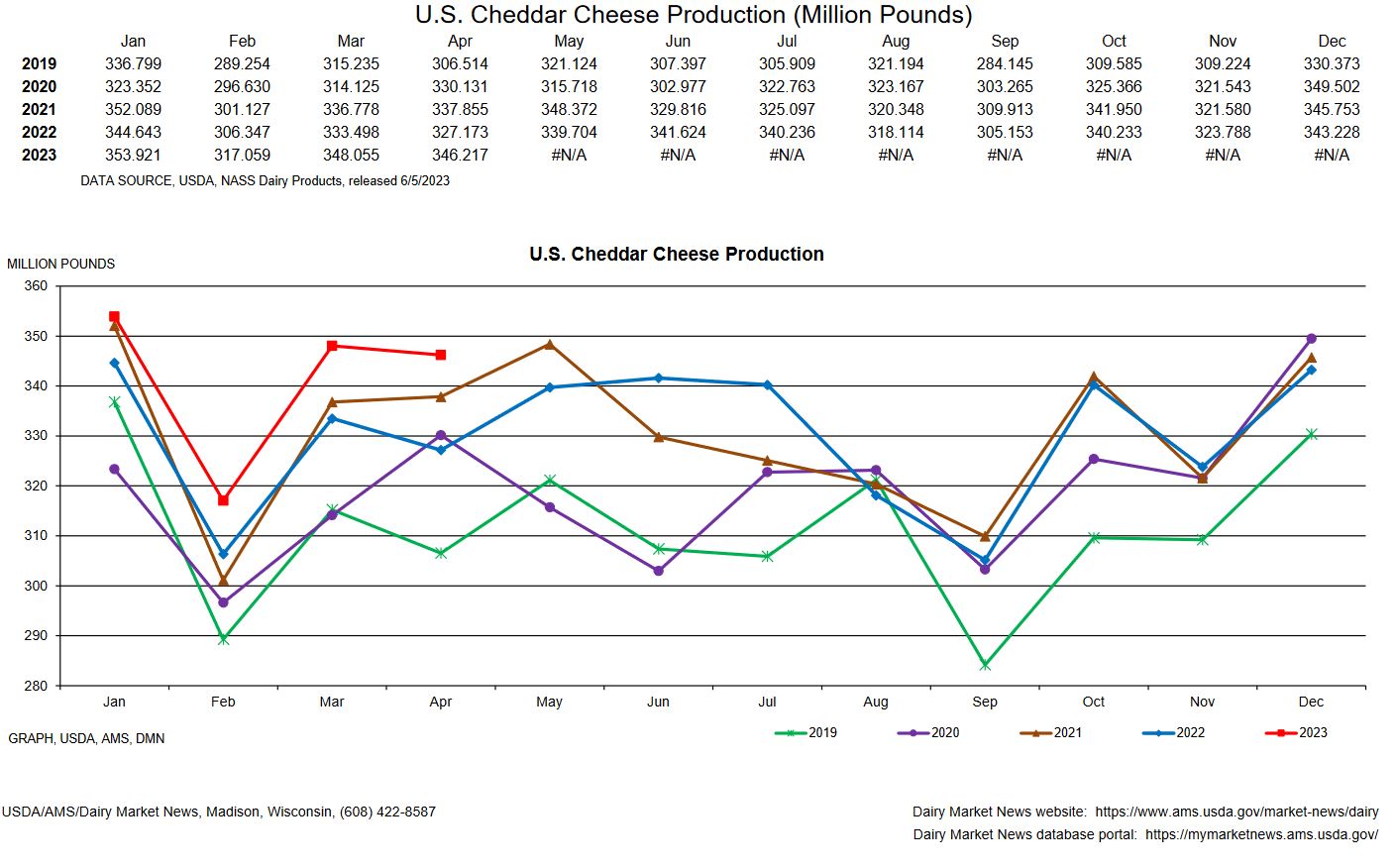

To much Milk, that has been the theme this year with loads trading hands for the cost of shipping. When cheese plants in the upper Midwest have more then enough milk to meet there contract needs; they end up making more cheddar cheese so they can sell it at the CME. The chart above is the cheddar cheese production. Even though Milk Production in April was up .3% the cheddar cheese production was up 5.8%. That means cheese plants could produce a lot more cheese then they had contracts for. This is why we are $10 lower on the class 3 price then last year. The good news is that cold storage is actually down from last year. Therefore, the extra cheese is getting sold. This means when milk production comes down and there is not extra cheese in storage we should see class 3 prices rebound. Recommendation, Buy 1900 calls for 20 – 60 cents, Aug 23 – Mar 24.