11/13/2022

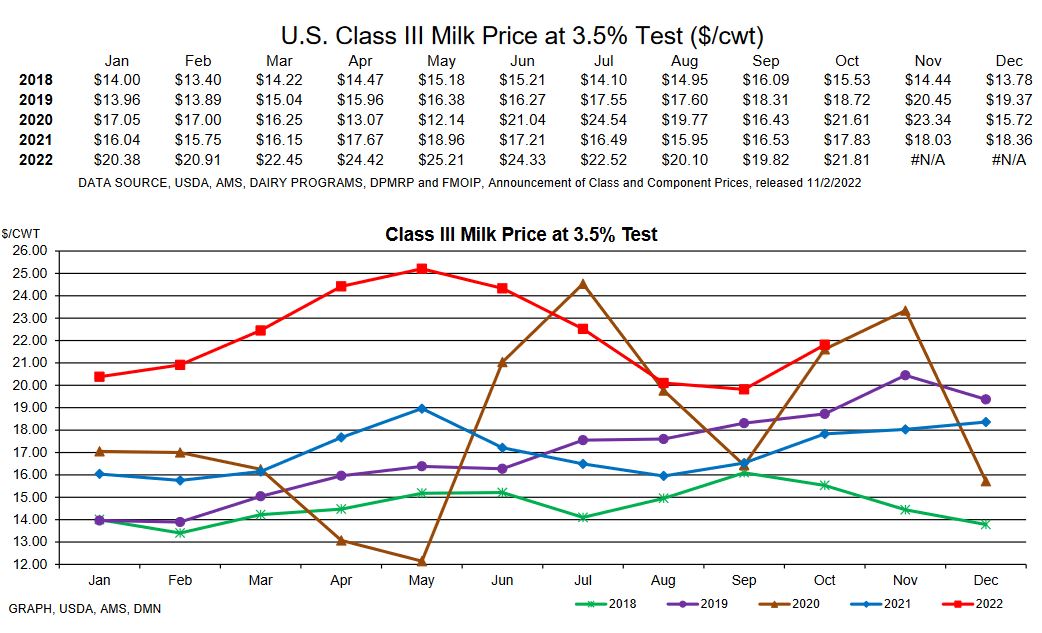

Big up week for class 3 this week as the government announced a “Feed kids & Families” program for the end of the year. This will be 2 billion for protein purchases. That announcement turn a bearish market around this week and pushed Dec 22 futures up more than a $1.50.

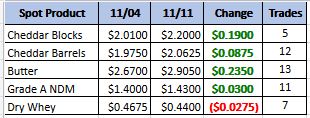

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk is available for cheesemakers in the Northeast and West to run steady production schedules, though some plant managers say they are operating below capacity due to labor shortages and supply chain delays. In the Midwest, spot milk remains steadily available, though cheese production varies across different plants. In recent weeks, curd and barrel cheese makers have reported shifting to alternate varieties to counterbalance slowing cheese sales. Some cheddar block and Italian cheesemakers say they are now seeing similar slowdowns. Western cheese contacts say retail and food service demands are steady. In the Northeast, retail demand, is steady to lower, though food service sales are unchanged. Loads of cheese produced in domestic markets are being sold at lower prices than those produced internationally, and contacts in the Northeast and West say this is contributing to strong interest from export purchasers. Spot loads of cheese are available for purchasing in the Northeast and West regions. (USDA Cheese Highlights)

Butter: Cream is becoming more available in the Northeast and in most of the West. Contacts in some parts of the West note cream remains tight. In the Central region, cream availability is mixed. Some plant managers say availability is growing week to week, while other report cream is available but purchasers could use more loads than are locally available. Butter production is growing in the Northeast and Central regions. In the West, butter makers are busy churning though some say labor shortages are causing them to produce below capacity. Food service demand for butter is steady in the Northeast and retail sales are active, though some regional stakeholders believe inflation is contributing to reduced shopper interest. Retail demand for butter is softening in the West as some grocers have finished purchasing butter to meet their holiday needs. Food service and bulk butter demand is steady in the region. In the Central region, demand is present for bulk butter, but butter stocks are, reportedly, exclusively from recent production. Butter loads are becoming more available in the West. In the Northeast, butter inventories remain tight, but some users are searching westward for loads to meet their current needs. Bulk butter overages range from 5 to 18 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: Prices for the most part, are steady with previous weeks’ reports. However, there was a slight bump on the top of the range. Dry whey availability varies from one plant to the next. Some sought-after brands are reportedly tight, while interchangeable loads are readily available. There were some situational loads traded at above the current range, although current markets are comfortably within the low/mid-$.40s zone. Some end users say they are chock full at the moment, and are showing little to zero interest in the spot market. After a few weeks of consternation regarding 2023 contracting negotiations, contacts are starting to report agreements being made. Production rates are generally steady, although there continue to be reports from cheese plant managers closing an extra day or two per week for scheduled maintenance. Milk, though, is steadily available. Animal feed whey prices are unchanged on steadily slow trading activity. Most trading is taking place toward the top of the animal feed whey range (mid-$.30s.) Generally, dry whey market tones are somewhat stable. (USDA Dry Whey updates)

With the governments announcement this week and better demand on the domestic front there was a good rally in class 3 prices this week. Class 3 futures 2023 is back over $20 and that makes it a good time to get some hedging done. I would recommend selling up to Half and then looking to put spreads or DRP on another 25%. This may seem pretty agressive but as governments continue to grapple with bringing down inflation, and consumers tighten there belt to get by; these prices could disappear fast.