9/25/2022

Both milk production and cold storage were out the week. I do not think anyone was to surprised with ether. First milk production came out on the 19th and with a total of 19.0 billion pounds for August. That is up 1.6 from last year but down slightly from last month. Next cold storage came in 4 percent up from last year but 3 percent down from last month. Futures sold off on Friday more on concerns of a recession then a reaction to ether one of the reports this week.

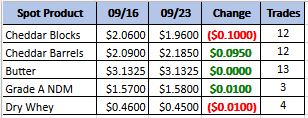

Weekly Spot Prices

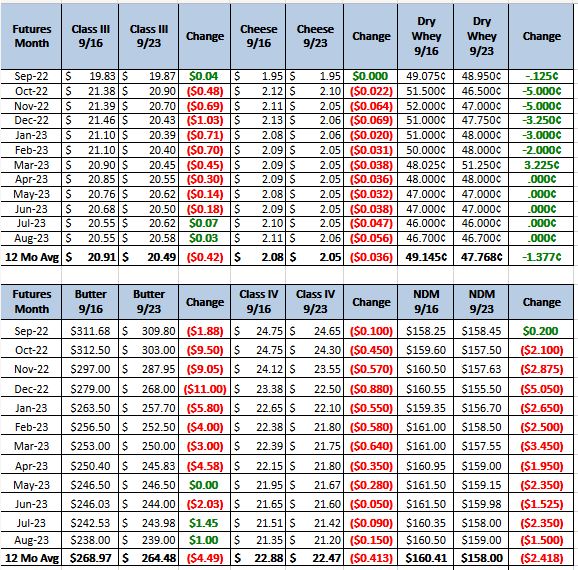

Weekly Future Prices

Cheese: Milk availability is tightening across all regions, though cheese makers in the Northeast and West say volumes are sufficient for steady production. In the Midwest, cheese production is trending higher amid stronger market prices. Spot milk offers are becoming rare in the Midwest, though some cheesemakers are selling their loads at or above Class III. In the Northeast and West, strong demand for cheese is present from export purchasers. Domestic sales are declining in the Northeast. In the West, retail demand is softening while food service sales are holding steady. Cheese producers in the Midwest say they are cutting back on orders to keep up with the recent rise in demand. In the Midwest and West, cheese barrels are tight as contacts cite strong demand. Cheese blocks are available for spot purchasing in the West. In the Northeast, spot purchasers say cheese is available. (USDA Cheese Highlights)

Butter: In the West, cream volumes are tight though sales are mixed. Regional ice cream makers are reducing their purchasing, but demand for cream is strong from butter makers. In the Midwest, butter makers say spot loads of cream are very tight to unavailable, and cream multiples are in the 1.30s. High cream multiples in the Northeast are causing some butter makers to steer cream away from churns, reducing butter production. In the Midwest, butter makers are increasing their micro-fixing as less butter is churning. Contacts in the West say they are running reduced production schedules. In the Northeast, retail butter demand is picking up, but tight inventories are causing some producers to regulate supplies across existing orders. Demand for butter is steady from retail and food service purchasers in the West. Contacts in the region report spot inventories of butter are tight, and that loads of unsalted are more difficult to find than salted. In the Midwest, butter demand is currently outpacing supplies. (USDA Butter Highlights)

Dry whey: In the West the bottom of the dry whey price range moved higher while in the Midwest it moved lower. The top of the range shifted higher in both the East and West. Demand for dry whey is steady in both domestic and international markets. Spot purchasers say loads of dry whey are available, but stronger demand for specific brands has made their loads more difficult to obtain. Cheesemakers are running steady production schedules, despite declining milk output. Liquid whey is available for drying operations to steadily produce dry whey. Some plant managers in the East region say they are running below capacity due to labor and supply chain shortages. (USDA Dry Whey updates)

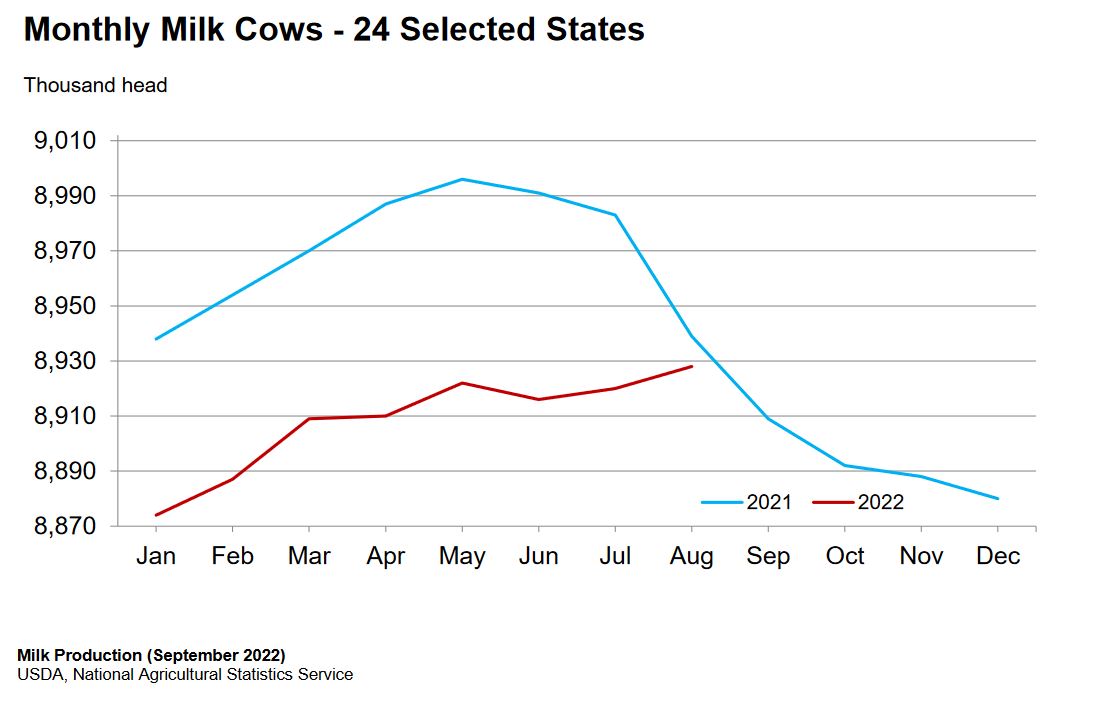

The graph above show cow numbers, and I expect we will see 2022 exceed the cow numbers of 2021 on the next report. This means milk production for the rest of the year will exceed that of 2021 by a good margin. This may be partly to blame for the bullish market that we have been running the last couple of weeks cooling down. On the other hand we are drawing down on cold storage which means demand is still out pacing production. The question going forward is will that continue going forward with the threat of recession looming. Recommendation this week is to buy some calls to sell into on a rally. Buy 22.00 call sell 24.00 call for 50 cents, and stick in sell orders at 22.50.