8/14/2022

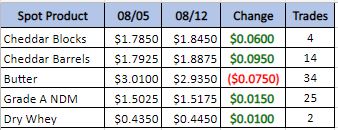

After several weeks of lower prices on Spot and the futures we saw a little rebound this week. With a 6 cent blocks and 9.5 cent barrel rally a few traders have started to look for a bottom. This lead to 54 cent rally in class 3 in the next 12 months. There are reports of good demand for cheese under 2 dollars. This has given some specs confidence to go long. With that said sales are still reported to be slower for this time of year.

Weekly Spot Prices

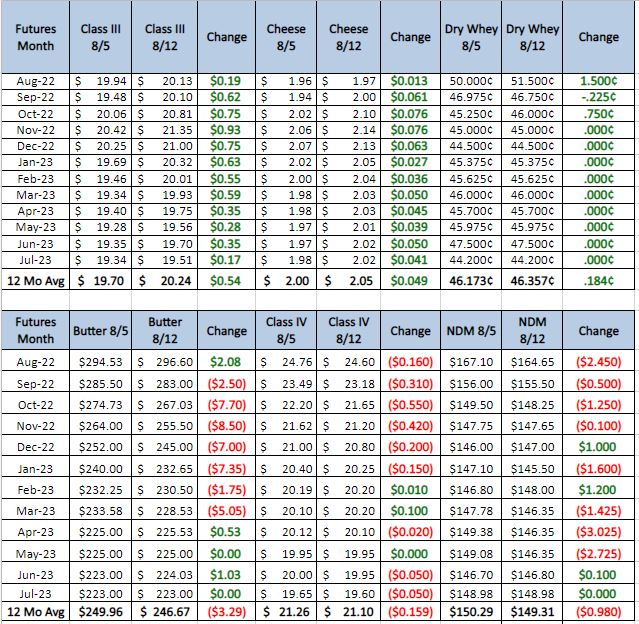

Weekly Future Prices

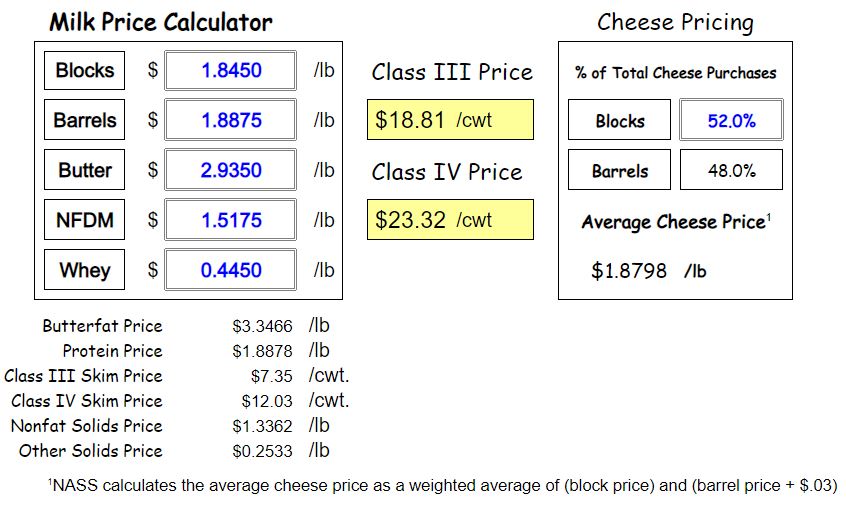

Cheese: Milk output is declining in the Northeast and West, but contacts in these regions say milk is available for cheese makers to run busy production schedules. In the Midwest, milk availability varies by location and timing. Cheese inventories are available for spot purchasing across all regions. Demand for cheese is softening from both retail and food service customers in the Northeast and West. In the Midwest, cheese demands have been varying from week to week, but stakeholders say they have been consistent this week. Some Midwestern cheese contacts say the drop in cheese prices in recent weeks has encouraged some increased purchasing, while others note that sales are seasonally slower. (USDA Cheese Highlights)

Butter: Cream supplies are tightening across the country. In the Northeast and West, high temperatures are contributing to reduced milk output and cream volumes. Some butter makers in the Northeast and West say higher cream multiples have made selling cream more advantageous than churning. Butter production is steady to lower in the Northeast and West. Labor shortages and high temperatures are contributing to some reduced butter making in the West. Micro-fixing has increased in the Central region, despite the increased number of employees required and staffing shortages at production facilities in the region. Demand for butter is trending higher in the Central region as some customers are preparing their fall inventories. In the Northeast, overall butter demand is stable. Some butter shoppers in the region say higher market prices have made them wary of taking on extra loads. Food service and retail demand for butter are declining in the West, though bulk butter demand is strong. Bulk butter overages range from 2 to 16 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: Demand for dry whey is unchanged in domestic markets, while export demand is softening. Stakeholders say exports to Asian markets are down compared to last year and remain below some expectations. Dry whey prices slid lower across the range and mostly price series, this week. The bottom of the price range slid below $0.40, for the first time since December of 2020. Spot purchasers say dry whey is available, and inventories are growing as supply is outpacing demand in the region. Liquid whey is available for drying operations to run busy schedules. Dry whey production is steady, but remains hampered by labor and supply chain shortages. Plant managers say they are focusing on the production of higher whey protein concentrates and permeate. (USDA Dry Whey updates)

Class 3 futures rallied this week as it maintained a $1.50 premium to spot. With weak demand still in the updates the recommendation is still for put spreads or selling in the front months as NDPSR should start to narrow the gap with spot prices. To limit risk to the top end look to buy the $20 put sell the $19 put for 30 cents, Oct. 22 through Feb. 23.