6/10/2022

Updates are stronger this week with better demand in whey and cheese. Global Trade prices went up but cheese price went down on this weeks action with their cheese price now coming in at 2.43. Class 3 and Class 4 prices for the month of May come in at 25.21 and 24.99 respectively but current cash prices have them at 23.46 and 26.63. NDPSR and cash prices are pretty disconnected right now but we should see the gap close in the next couple of weeks.

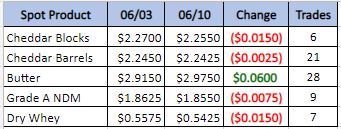

Weekly Spot Prices

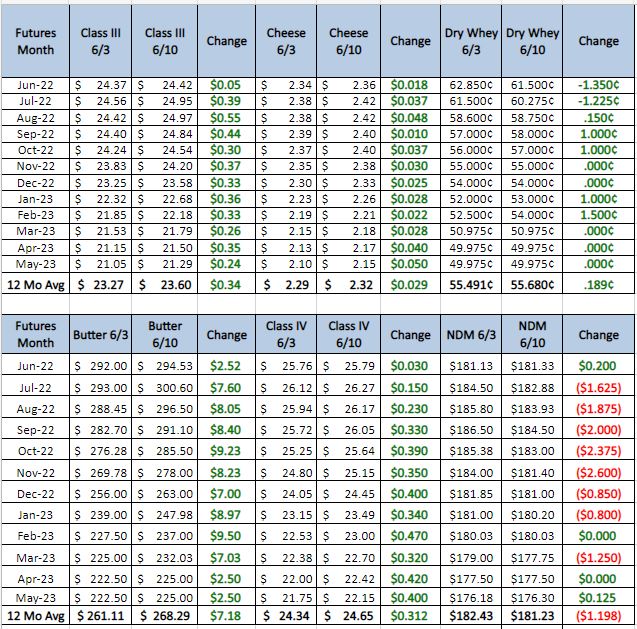

Weekly Future Prices

Cheese: Cheesemakers across the country say that milk supplies are available for production facilities to run active schedules. Some Midwest contacts relay that production schedules are limited by labor shortages. These shortages as well as delayed deliveries of production supplies are causing some cheesemakers in the West to run below capacity. Meanwhile, a few barrel cheese plant operators in the Midwest are reporting some maintenance related downtime this week. Domestic demand for cheese has, reportedly, begun to soften across both food service and retail markets in the West, though sales are fairly stable with some hints of softening in the Northeast. Midwest cheese orders are stable and/or meeting seasonal expectations. Contacts in the Northeast and West say that strong interest is present from purchasers in international markets and that spot inventories are available in both regions. (USDA Cheese Highlights)

Butter: Across all regions, cream inventories are tightening. Despite this, some contacts in the Northeast report that cream is more available than is typical at this time of year. In the West, some stakeholders say that they are receiving inquiries from cream purchasers in other regions. Slower butter sales and higher cream multiples, in the Northeast, are contributing to some reduced butter production schedules and increased cream sales. In the Central region, some butter makers indicate that they are increasing their micro-fixing. Plant managers in the region have been reporting staffing shortages for months, and some are concerned with the additional employees needed for micro-fixing. Butter makers in the West say that labor shortages and delayed deliveries of production supplies have caused output to fall below expectations for the last few months. In the Northeast and West, consumer demand for butter at both retail and food service markets has softened. Some purchasers in these regions are, reportedly, selecting lower-priced private label brands of butter due to higher retail prices. Loads of butter are available in the Central and West regions, though availability has tightened in the Northeast. Across all regions, bulk butter overages range from 5 to 15 cents above market. (USDA Butter Highlights)

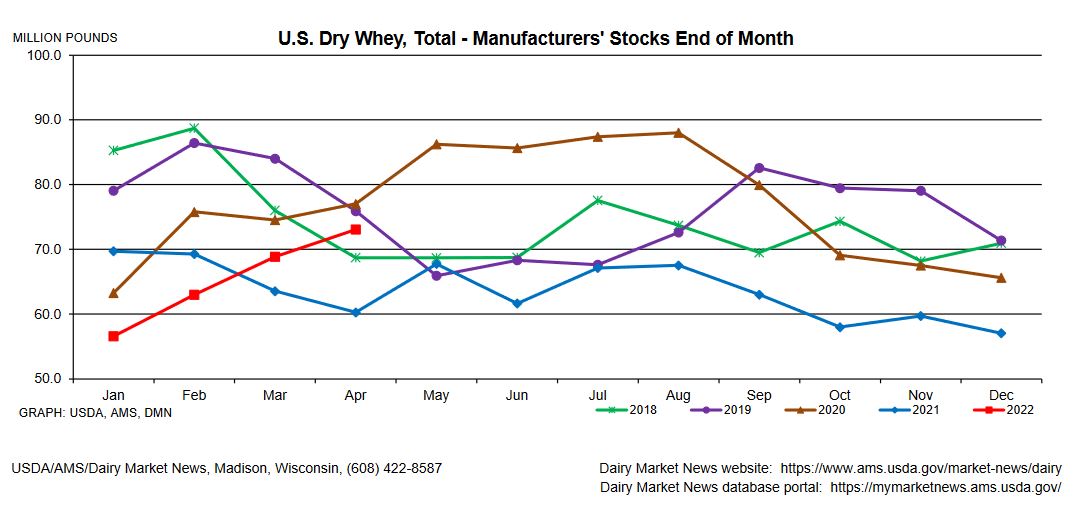

Dry whey: Domestic demand for dry whey is unchanged to steadier then previous weeks. Export demand is steady to lower, as contacts report that sales to Asian markets remain below expectations. Prices held near the top on the top of the range. Port congestion and a shortage of available truck drivers are contributing to some delays in deliveries of dry whey loads. Spot purchasers say that dry whey inventories are available. Cheese makers are running busy schedules, leaving supplies of liquid whey available for drying operations. Plant managers say that they are actively drying whey, but some are focusing their schedules on the production of higher whey protein concentrates and permeate. (USDA Dry Whey updates)

There is still plenty of milk flowing into cheese plants as they run full schedules for both cheese and whey. This has not been a problem because demand has been driving this market and keeping prices at all time highs. This is large part to do with exports, they have been very strong and they are still strong but whey demand has slipped a little bit. With whey prices also slipping into the low to mid 50s the average cheese price needs to come in around 2.45; if we are to hold onto the $25 Class 3 futures prices. Recommendation this week is for selling milk over $25 or buying $24 puts and selling $26 call for even money, July through September 2022.