5/20/2022

Good rally this week in class 3. Prices pushed higher this week despite a drop on the cash market on the blocks and whey. Production report was down 1% with milk out dropping the most in Florida and New Mexico. Both down more then 12 percent from a year ago. With the dry weather in the southwest and the high cost of feed, dairies have continued to shed cows and milk production in this area. That said most updates across the country this week state that there is plenty of milk for manufacturing.

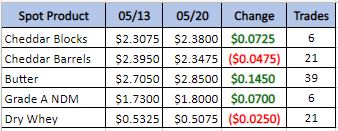

Weekly Spot Prices

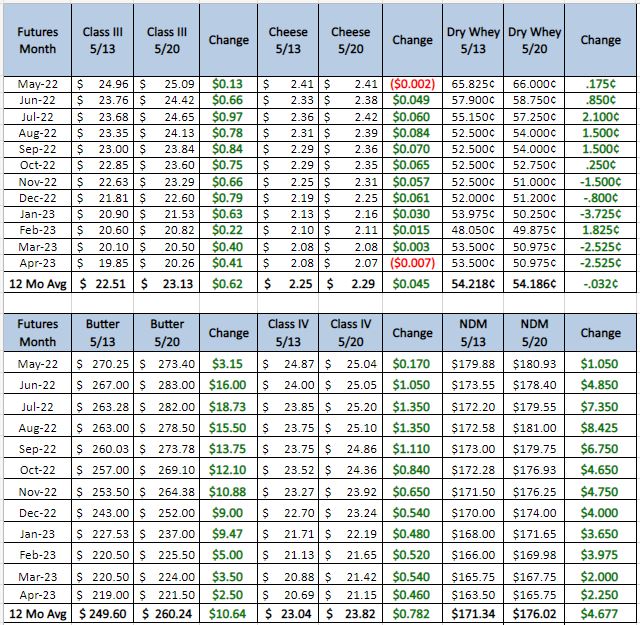

Weekly Future Prices

Cheese: Across all regions cheese production is active, though some production facilities in the Northeast and West are, reportedly, running below capacity due to labor shortages. Some cheese makers in the West also cite delayed deliveries of production supplies and limiting their ability to run full schedules. Midwestern cheese demand is mixed; contacts report that slipping prices in previous weeks caused some hesitance from purchasers, while others are purchasing to get ahead of a potentially bullish market. Meanwhile, demand is noted to be hearty in the Northeast and West. Cheese inventories are present to satisfy demand in the Northeast. In the Midwest, availability varies from balanced to tight. Spot inventories are available in the West, but contacts in the region say that cheese barrels have begun to show some tightness in recent weeks. (USDA Cheese Highlights)

Butter: Cream inventories are available in the West, and contacts note that purchasers from other regions are interested in buying loads to meet local production demands. Contacts in the Northeast and Central region relay that local cream spot availability is tighter. Some butter makers in the Northeast say that more cream is being churned this week, though butter production schedules vary across manufacturers. Meanwhile, butter makers in the Central and West regions are running active schedules. Western butter makers say that labor shortages are limiting their ability to run full schedules. Contacts in the Central region report that demand has softened in the past few weeks. Food service demand for butter is stable in the Northeast and West, while retail demand is trending lower. Spot inventories are unchanged in the Northeast, but are becoming more available in the West. Bulk butter overages range from 4 to 15 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: Prices for dry whey continue to slide lower across the price range, though the top of the mostly price series is unchanged. Market prices for dry whey have fallen on the CME, by 6.5 cents since last Wednesday. Contacts say that domestic and international demand is soft. Some spot purchasers report that uncertainty in the market is preventing them from buying additional loads, despite lower prices. Dry whey inventories are available. Deliveries of loads continue to face delays due to port congestion and a shortage of available truck drivers. Cheese operations are running busy schedules, leaving plenty of liquid whey available for drying. Meanwhile, plant managers say that dry whey production is limited as they are focusing their schedules on the production of higher whey protein concentrates and permeate. (USDA Dry Whey updates)

July Class 3 Futures Price This Week

Good rally this week on a little less milk production. As seen from the updates that has not slowed cheese production, if any thing it is the plant capacity that is the bottle neck; weather that is just capacity or a combination of labor and shipping issues. Cold storage is this next week. It may be a good time to get some hedges in place before that report. Recommendation is still for put spreads. Buy the $24 put sell the $22 put for 45 cent July to September 2022.