1/7/2022

Happy new year. The dairy market ended 2021 red hot and the first week of 2022 we saw new highs on class 3 and class 4 futures. Expect more volatility in the coming weeks as futures remain at a premium to NDPSR.

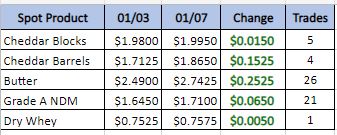

Weekly Spot Prices

Weekly Future Prices

Cheese: With the holidays behind, there is still an adequate amount of available milk for Class III cheese vats to satisfy the steadfast demand of a bullish cheese market. Along with COVID triggered labor shortages, hauling shortfalls and costly transportation fees, manufacturers are processing yet another supply chain challenge. Wintery weather conditions in the West and Northeast are further slowing the transporting of milk supplies to cheese production facilities, prompting tighter inventories in some instances. In general, cheese production in the regions this week is reported steady to lower in the West, mixed in the Midwest, and moderate in the East. Overall, interest is steady to stronger and supports the uphill adjustment in the block/barrel wholesale market prices this period.

Butter: Cream availability varies. Cream is tighter in the East and Central regions. While supplies are more available in the West, access has been stymied by inclement weather and limited drivers. Butter production is mixed. Spot availability is limited, and unsalted butter is noted to be more difficult to source than salted. Domestic demand is steady to stronger from retail and food service sectors. Export demand is healthy, as well, as global butter supplies are tight and U.S. prices are competitive. Across the country, bulk butter overages range from 7 to 18 cents above market.

Dry whey prices continued their push higher this week. Although demand is steady, availability notes are mixed. Some end users are beginning to report a few more loads being offered out, but a number of buyers continue to say availability is slim. Production rates have been uneven due to numerous factors from milk availability (preceding the holiday weeks) to staff/driver shortages. Additionally, a notably bullish pressure on higher protein whey concentrations has given rise to a growth in focus on producing WPC 80%, and the like. Animal feed whey trading has been sluggish since the upsurge of markets in the latter portion of 2021. This week, however, some trades were reported and prices are moving higher. Dry whey market tones are uncertain, with bullish undertones.

Tight supplies and good demand has push the class 3 and class 4 milk markets to new highs in 2022. The biggest question is will this demand last into the spring that is typically a slow demand period. My recommendation is sell or buy DRP. Both may become very expensive if futures move higher. But, in the last 20 years there has only been 1 year to average above $20.00.