4/17/2021

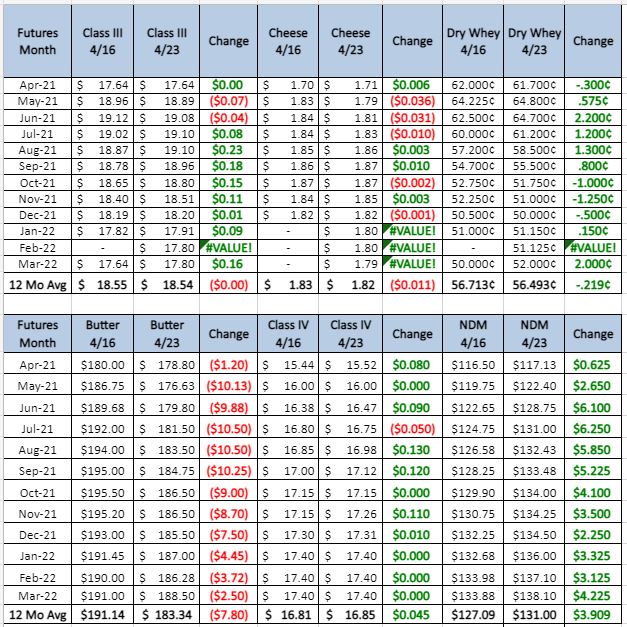

March milk production up 2.0 percent and March natural cheese stocks up 2 percent from last month and 7 percent from last year. Those are some big numbers for the amount of strength we have in this market. Normally when we are seeing class 3 futures prices in the 19s I would expect to see a draw down on cold storage, but the current market is built on the anticipation that there will be better days ahead.

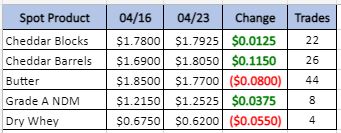

Spot Market Recap

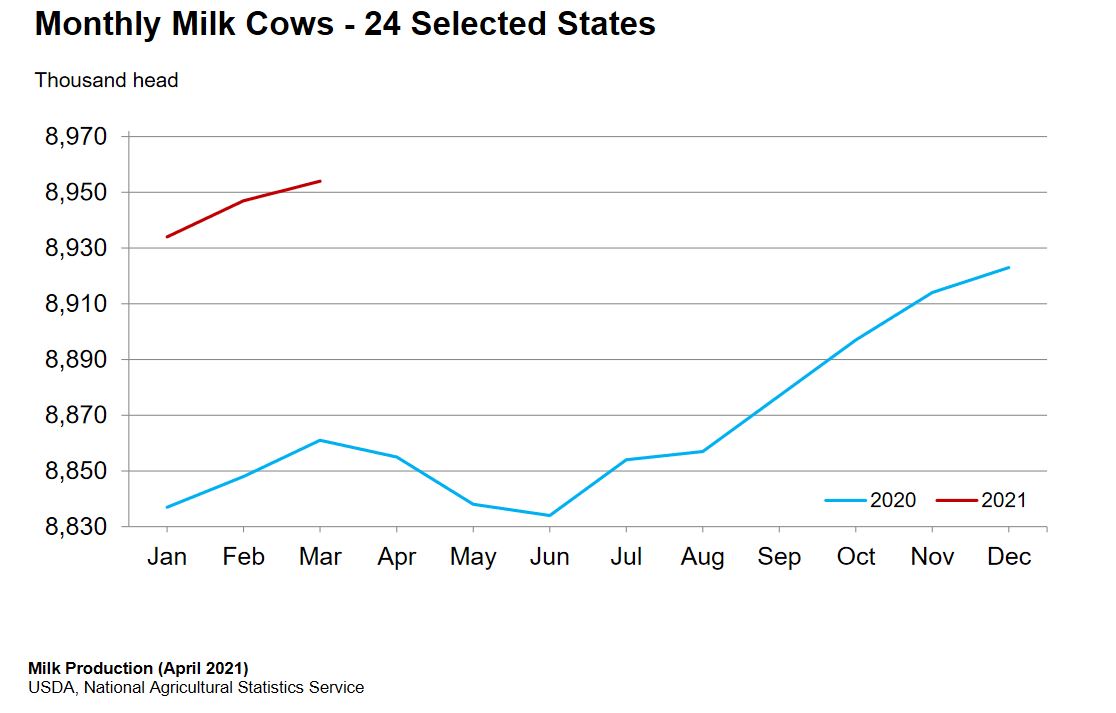

Milk Production

Cheese makers in the Northeastern region are reporting a steady milk supply for cheese making. Demand in food service continues to improve and the retail side remains strong. This has pushed price higher, with barrels now over taking blocks on the CME. In the Midwest cheese plants are running full schedules with spot load still going for $5 under class 3. On the demand side spring weather has brought buy back to the market as any extra loads are snapped up quickly. This has lead to a bullish market tone. On the west coast production has started to shift from retail focused to food service and demand is this sector continues to increase. Production schedules are running at full capacity as milk is readily available for manufacturing. Blocks are available for spot purchases but barrel stocks are tight.

Butter churns generally have adequate volumes of cream to support seasonal production so inventories remain stable. Retail demand is steady to lower. Food service demand is strong and climbing on both the east and west coasts. The market is a little unsettled but bulk butter prices have ranged from 1 to 8 cents above the spot market this week.

Dry Whey price this week was higher across the range. With current prices domestic demand is showing signs of slowing. Exporters have moved more product this week with the congestion at the ports easing but demand is also decreasing. Spot load are still tight and manufacturers are not running at full capacity instead they are focusing on production of higher protein whey.

Since march 30 July corn has rallied over $1.00. extremely over bought. With that said, Market Analysis with Mark Gold comments “could be looking at 18-to-19-dollar beans, 8-to-9-dollar corn”. Friday, we did have a small retracement which may have been a buying opportunity if China does buy the rumored 2 million tons of old crop corn and 1 million tons of New Crop corn. The Biden administration is looking to incentive producers to add to CRP set aside acres, in their climate change initiative. With prices where they are at, we will see if the government can come up with enough money to get producers to Idle acres. Recommendations this week: Buying Soybean meal for August forward needs, or buy December SM futures at 400/ ton or less, or bull call Spreads which give you limited upside protection but do not come with margin risk and are cheaper then buying call outright.

No slow down in milk production as of yet. Milk production in March was up 2 percent and the weekly updates having been reporting that milk is widely available. Production schedules are generally running at full capacities, although plants are looking to do some scheduled maintenance in the coming weeks. Demand is generally good with exports move well. I would look for this next week to hold steady which should bring option prices down as volatility falls. I would look to buy $18 puts for 40 cent or under in 2021 and $17 -$16 put spreads for 30 cents or under in 2022. Give us a call for more specific hedge strategies.