2/6/2021

Big rally on more stimulus talk, plenty of milk for cheese production, and food service sales improved but still on the weak side; as we have another wild ride this week.

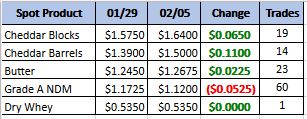

Spot Market Recap

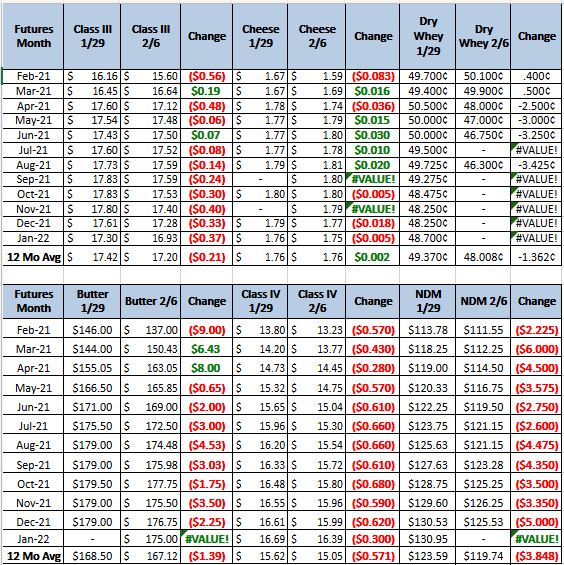

Milk Production

We were moving lower all week until Thursday after the close; then the Democrats fast tracked the $1.9 trillion stimulus bill and brought the buyers back to the market. With over $11 billion left from that last bill to spend and a possibility of more money coming behind that, buyers were more then willing to drive up future prices through the rest of the year. Still questions remain about how much will be funneled into the dairy market and how much of that will be spent buying up cheese.

Cheese Northeastern: There is plenty of milk for cheese makers to run full schedules. Inventory is steady for the time being and spot orders are fairly steady with several buyers still on the sidelines. Overall market tone is weak and somewhat unsettled. Cheese Midwestern: Spot loads of milk remain at steep discounts as cheese production is busy. Cheese inventories are in balance with cheese makers pushing more cheese into aging programs. Cheese Western: Cheese is widely available with inventories growing as production tries to keep pace with available milk. Demand has dropped off with football season drawing to a close and restaurant capacity still restricted.

Butter is starting to see a light at the end of the tunnel with export interest picking up and refilling the pipe line as restaurants start to recover. We are not out of the woods yet as inventories are widely available and heavy milk supplies still weigh down the market.

Dry whey prices are shifting higher on good demand and a little less production. Cheese plants are trying to limit the cheese output because of week food service demand for cheese which has also limited whey output. Animal feed whey prices were unchanged on another slow trading week. Inventories are tight with whey producers opting to fill orders for higher protein products instead of making sweet whey powder.

On the grain side China’s Dalian exchange is pricing corn at $10.92. This will give continued support in the corn market with China’s appetite for US Corn, it may take another bumper crop year to satisfy it. Consider a short-range trade; buying the March 545 put at 11 cents and buying March futures at 5.47- 5.50. The put will cover your long position for 15 + days . After the put expires manage your long position with Stops 10 cents below current price.

The dairy market is largely negative with overwhelming milk production hitting all facets of manufacturing. This drove class III prices down this week until there was the possibility of further government buying. This year is looking more like it will be a roller coaster ride with steep climbs on perceptions of more government buying, and drops when we are relying on non-government demand. My suggestion is after the drop starts to level out and the volatility drops, buy calls and wait for the jump from the next announcement to sell futures. This strategy is not for everyone. Talk to your commodity advisor on what is right for you and if there is anything we can help you, do not hesitate to call.