09/25/2020

The spot markets went through a turbulent week as follow-through buying after last week’s enthusiasm didn’t materialize and a harsh sell-off ensued, only to be greeted by a new government solicitation Thursday afternoon, causing a rebound of sorts on Friday. The block/barrel spread narrowed to “only” 89½¢, but the star this week was NDM, with a 3¢ gain, settling NDM futures much higher.

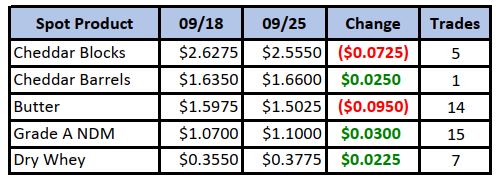

Spot Market Recap

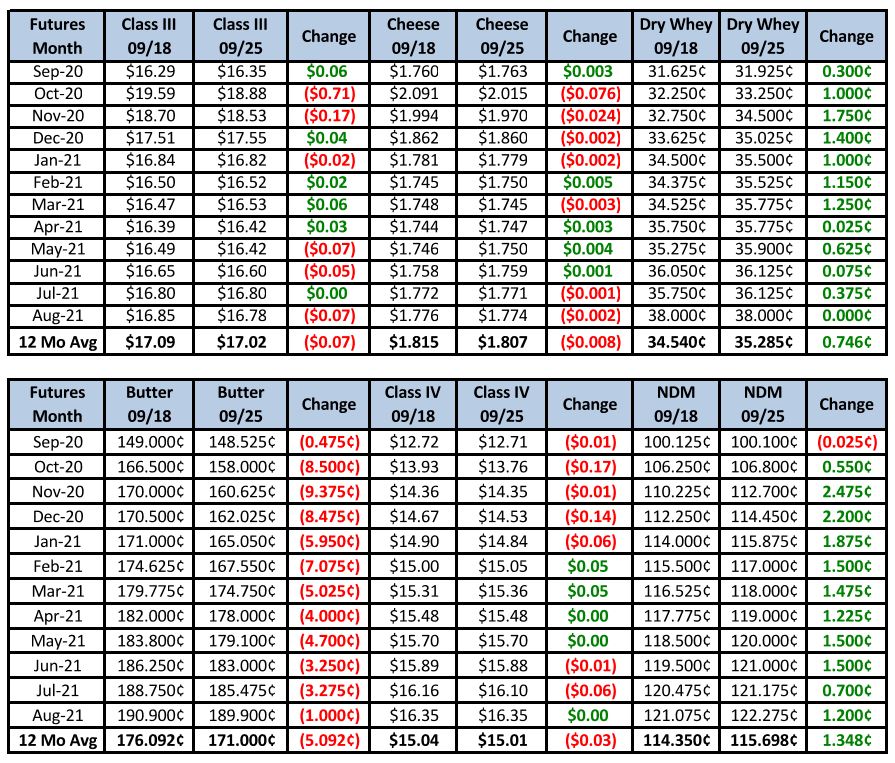

Futures Recap

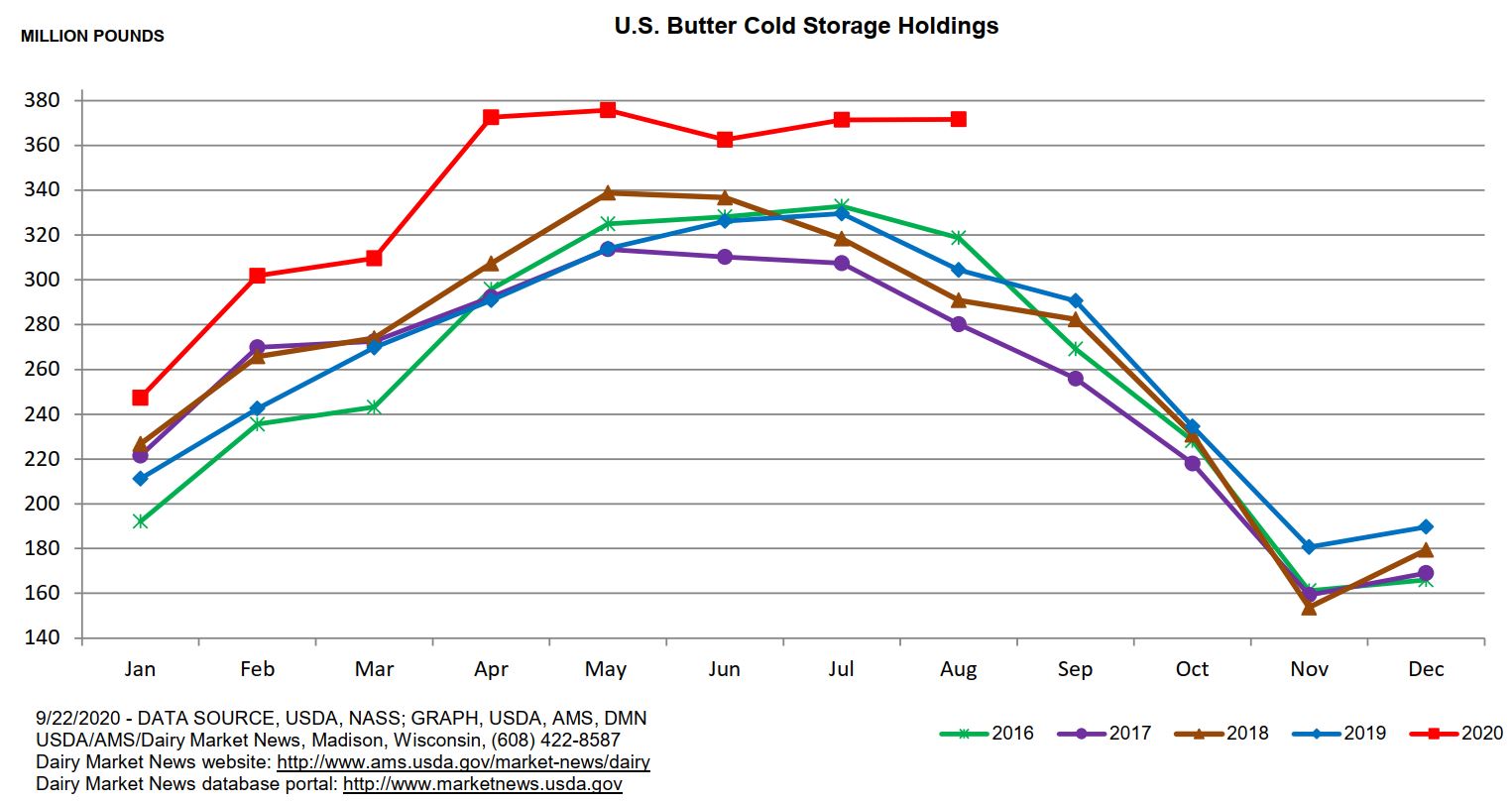

Two USDA reports were released this week, but with the government involved in our markets, they had little impact, except for maybe butter. The Cold Storage Report showed butter stocks in U.S. warehouses at the end of August totaled 371.7 million lbs, up 22% from a year ago and unchanged from the prior month. As can be seen from the graph below, butter stocks are typically declining at this time of year. No doubt the slowdown in restaurant sales due to COVID is partly to blame.

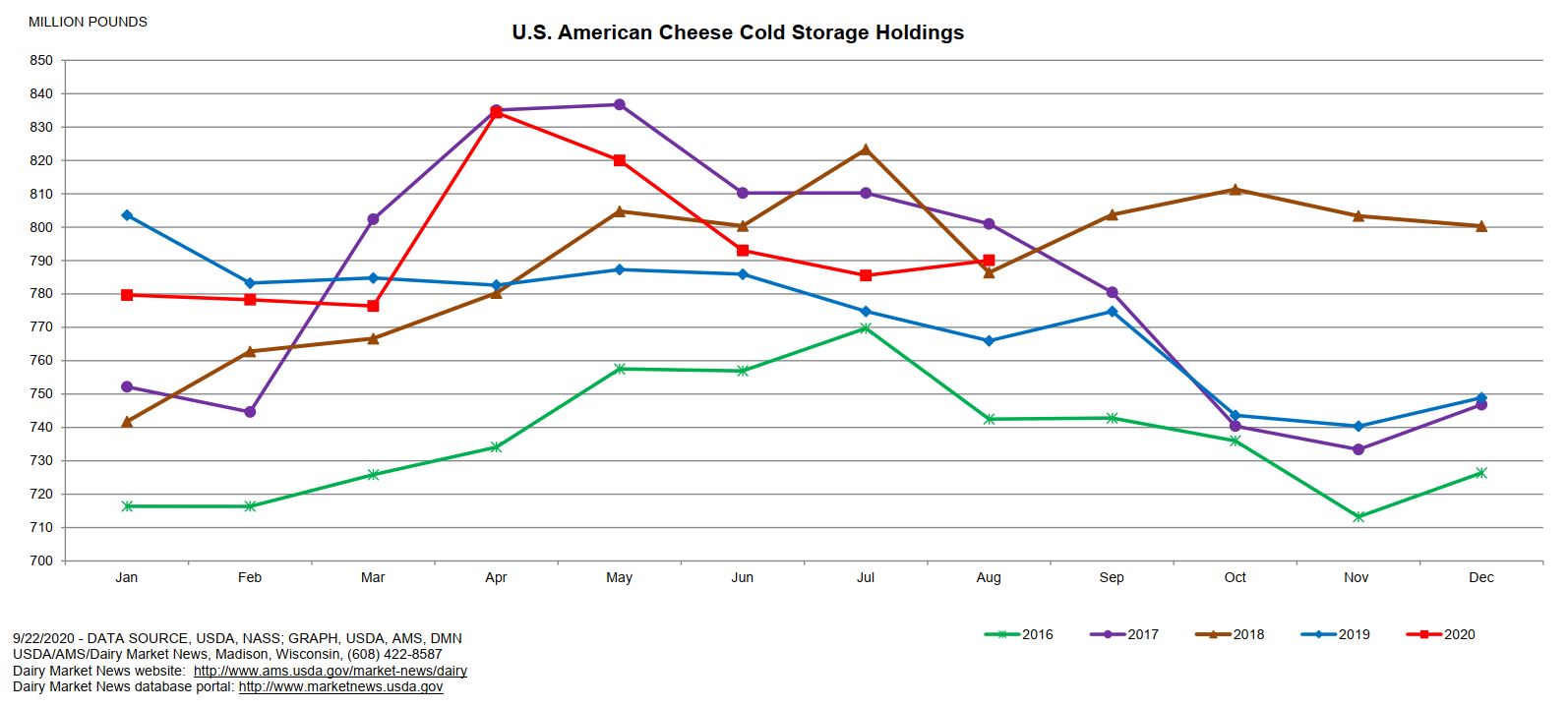

American cheese stocks pulled off the same trick, increasing an anti-seasonal 1% vs. July, while notching a 3% increase over Aug 2019.

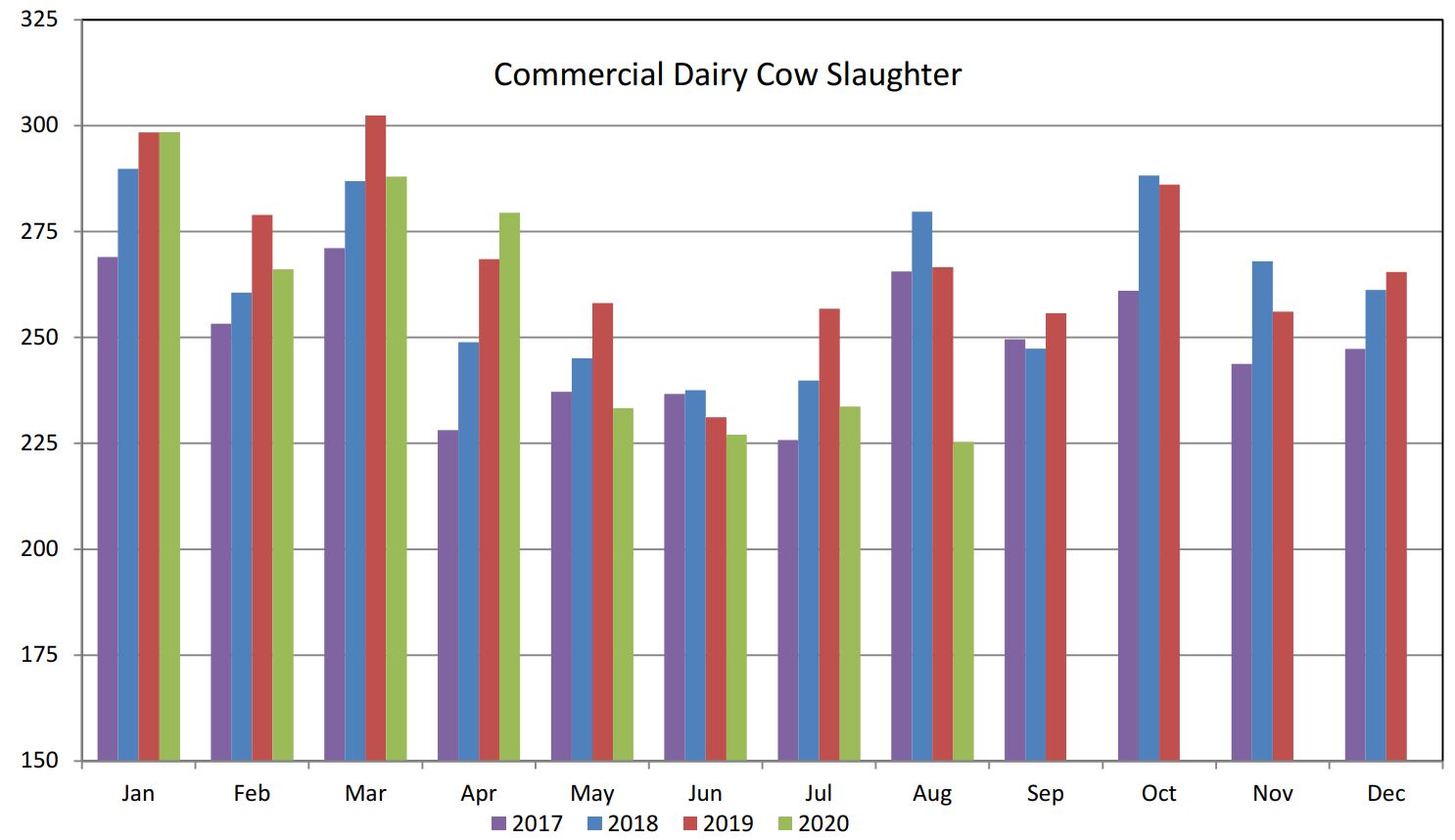

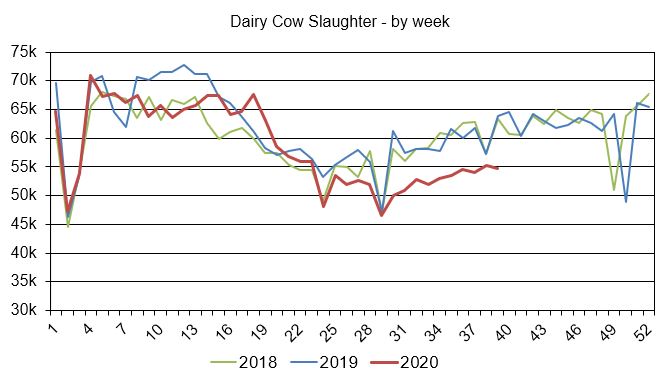

Next up, the Livestock Slaughter Report revealed a dramatic YoY decline of 15.5% and the lowest total for August since 2007.

Weekly numbers indicate we may see a similar decline when the Sep report is issued. For the week ending 09/12, just 54,700 head were culled, down 14.3% vs. the same period a year ago. Looking at the week to week trend in the graph below, we can observe the gap between this year’s culling activity and the prior two years, especially starting after week 28. This data suggests the size of the herd is probably already in expansion mode.

Were it not for government programs artificially stimulating demand, our bias is that prices would head lower in short order. Speaking of government programs, on Thursday afternoon, USDA released a new solicitation for 56.6 million lbs of natural American cheese, with 44.9 million lbs of that for barrel cheese. Barrels are in more plentiful supply, so in the short-term, it could help close the block/barrel spread if bidders decide to get involved with the contract. Another interesting detail on this contract is that it’s labeled as a “shortfall invitation”, probably meaning the government is trying to acquire cheese it failed to get in previous solicitations. Spot barrels did jump 2¾¢ in today’s session on zero trades, so perhaps they continue to move higher next week.

Dairy Market News reports EU milk production is growing faster than in the U.S.; July output was 2.2% higher than a year ago, putting their Jan-July production up 2% vs. 2019. Australia has begun its new milking season, with the first month of July showing a 2.9% increase over last year, while New Zealand reported an August increase in milk production of 5.8%. Weather has been favorable, leading to projections of a strong year.

In the U.S., milk production is mostly steady, with plenty of milk available for processors due to lower Class I needs from schools. Pizza cheese demand has remained strong and food service orders are gradually increasing, but most cheese plants across the country are able to run at or near full capacity. Blocks are tighter than barrels, though supplies are not burdensome for either.

October Class III really saw some whip-saw action, opening the week at $19.58, before plummeting expanded limits at one point, hitting a low of $17.72 on Thursday, before ripping 73¢ higher on Friday to settle at $18.88. The market feels like it doesn’t want to move higher, but then gets jerked by news events. In addition, current spot prices work out to about $20,00 milk and we are in the October pricing period, putting Oct futures at a steep discount to cash. Are current spot prices sustainable? It’s hard to say, but current cheese futures are expecting some type of decline. Oct block cheese futures settled at $2.40/lb, well behind spot.

Current government intervention is providing an opportunity for hedgers to lock in higher prices. Unless we are rid of COVID-19 soon, we return to a growing economy and global exports improve, we believe we’ll be heading in to the new year with too much milk. A strong start to the new milking season in Oceania and solid growth in the EU could put us in a global surplus. Will the U.S. government keep spending on Ag at similar levels after the election? Producers should begin looking at the first half of 2021 and getting some hedges on. At a $16.56 average Jan-Jun might look pretty good several months from now.

Have a great weekend!