07/24/2020

Block cheese suffered more losses this week, but it was a more ordered affair than last week’s sudden crash. Barrels managed to finish the week in the green along with butter and dry whey, while NDM fell back below $1/lb.

Spot Market Recap

Futures Recap

In addition, the herd continued to decline for the 3rd consecutive month, losing 10,000 head from May, though still higher than 2019 numbers.

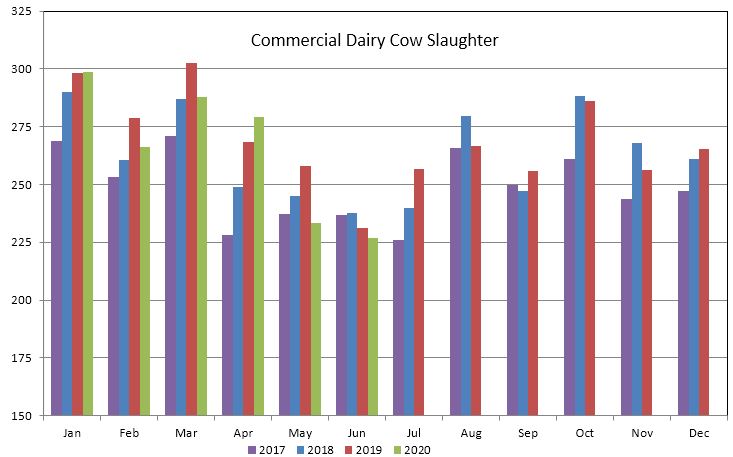

With record high milk prices, however, this may be about to change. Weekly dairy cow slaughter numbers have been lagging year-ago levels as of late (10 straight weeks), with the number of culled cows down 18.4% in the most recent report dated 07/11. Likewise, the monthly slaughter numbers for June were down 2% vs. a year ago and the lowest June total since 2016. We would expect the herd to enter into expansion mode soon.

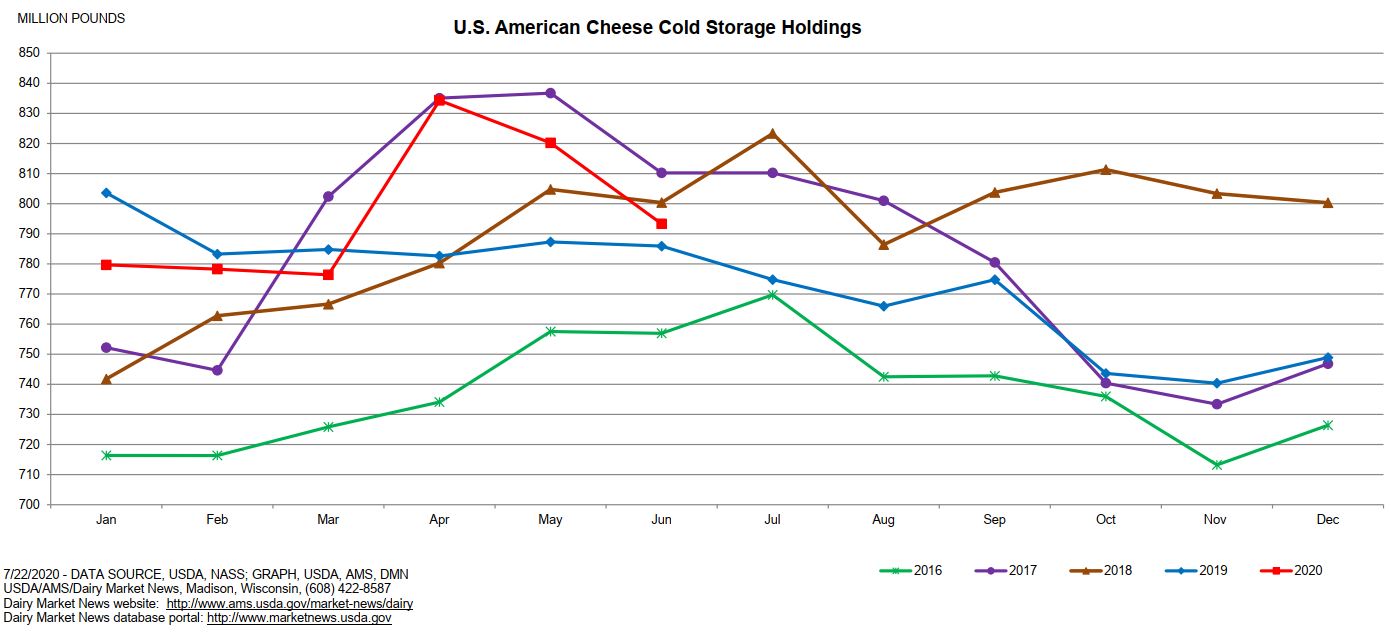

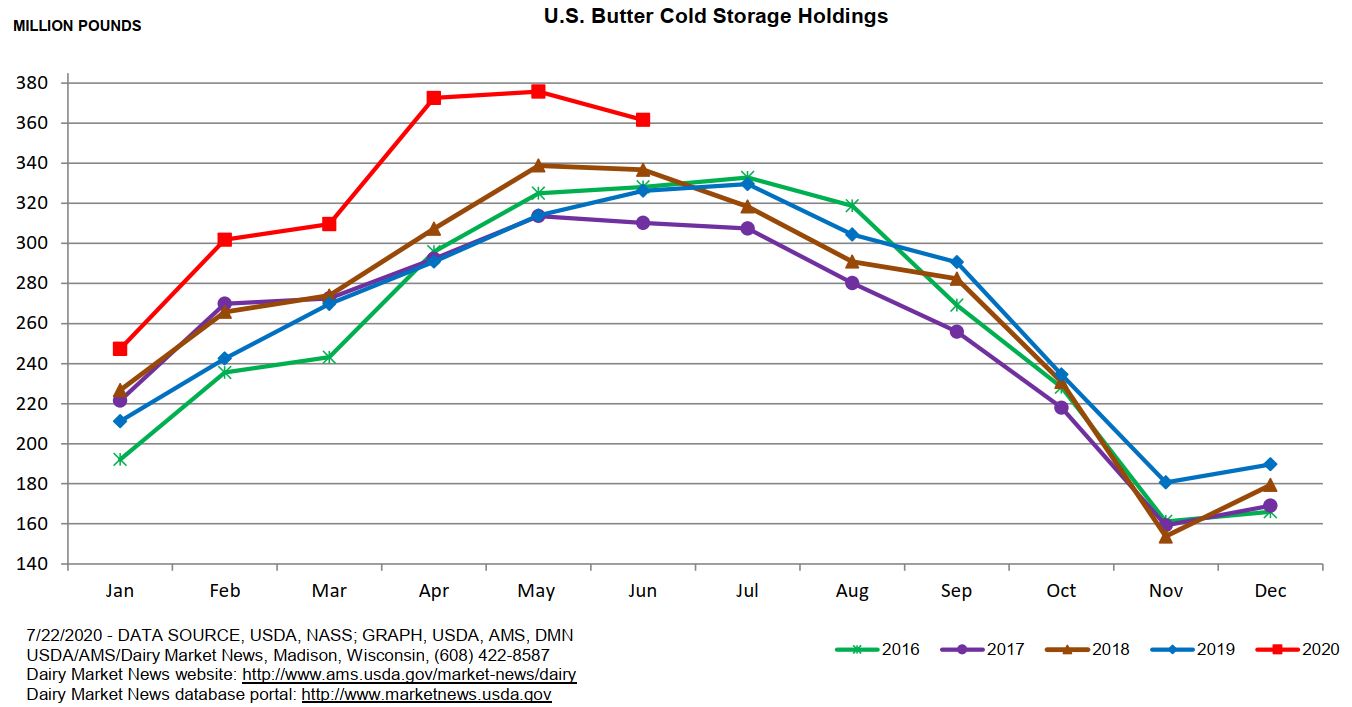

The Cold Storage Report was also released this week and was mainly neutral to the market. American cheese stocks at the end of June were up 1% compared to June 2019, but saw a sizable decline from May. We would expect holdings to continue to decline in light of government programs and strong retail sales.

Butter stocks were 11% higher YoY, remaining at record levels for the month. The loss of food service sales, primarily to sit-down type facilities, is clearly reflected here.

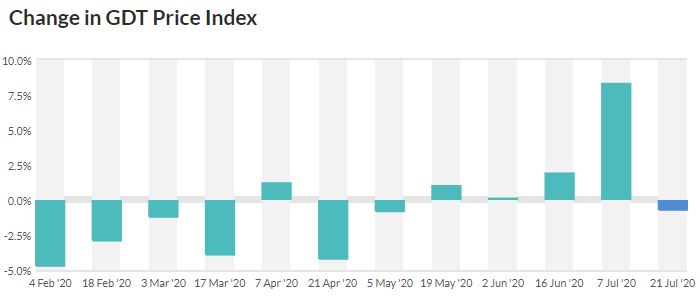

On the international front, after a very strong result at the last event, this week’s GDT auction saw the Dairy Price Index decline 0.7%, its first loss since May.

Technically, the momentum in the near term is still to the downside up front, but that may change. This afternoon, USDA announced a third round in the Farmers to Families Food Box Program, and will spend about $1 billion on fresh produce, dairy products, fluid milk and meat. Solicitations for products will arrive in the coming days, and will us some detail on how much will be purchased in each category. If it is similar to the first two rounds, cheese will get a fair share. With August Class III wrapping up its first week of pricing over $24/cwt, it could make for an interesting market open Sunday evening at 5pm. August futures are pricing in a very large discount to spot. If that doesn’t happen and buyers show up to fill government bids, it will be forced to rally.

Producers should begin to get more aggressive in covering Q4 and the first half of 2021 in our opinion. Unless new government programs are passed, this third round of the Food Box program is it. Deliveries for this third round are for Sep 1 through Oct 31. With an election Nov 4th, government spending on aid programs is likely to slow down or come to a halt afterwards. Current prices are encouraging herd and output growth. Recent numbers, as indicated earlier, are pointing to a larger milk supply heading into the end of the year. There are questions as to the long-term strength in our economy. Hedgers should take advantage of any future strength in the market to get up to 50% sold. The Q4 average settled at $17.60 today, with the first half of 2021 at a $16.45 average. Get something done. We can work with it after you’ve established the hedge to open it to upside using options.

Have a great weekend!