03/06/2020

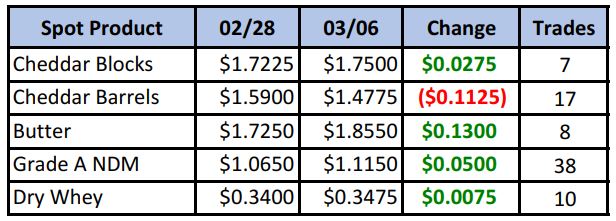

All it took was a relapse in spot barrels and ongoing coronavirus fears to drive futures lower, despite the other spot components all finishing the week higher. Trading was most active in NDM as buyers continued to see value at current prices. The switch from “old crop” to “new crop” butter also put a bid in that market.

Spot Market Recap

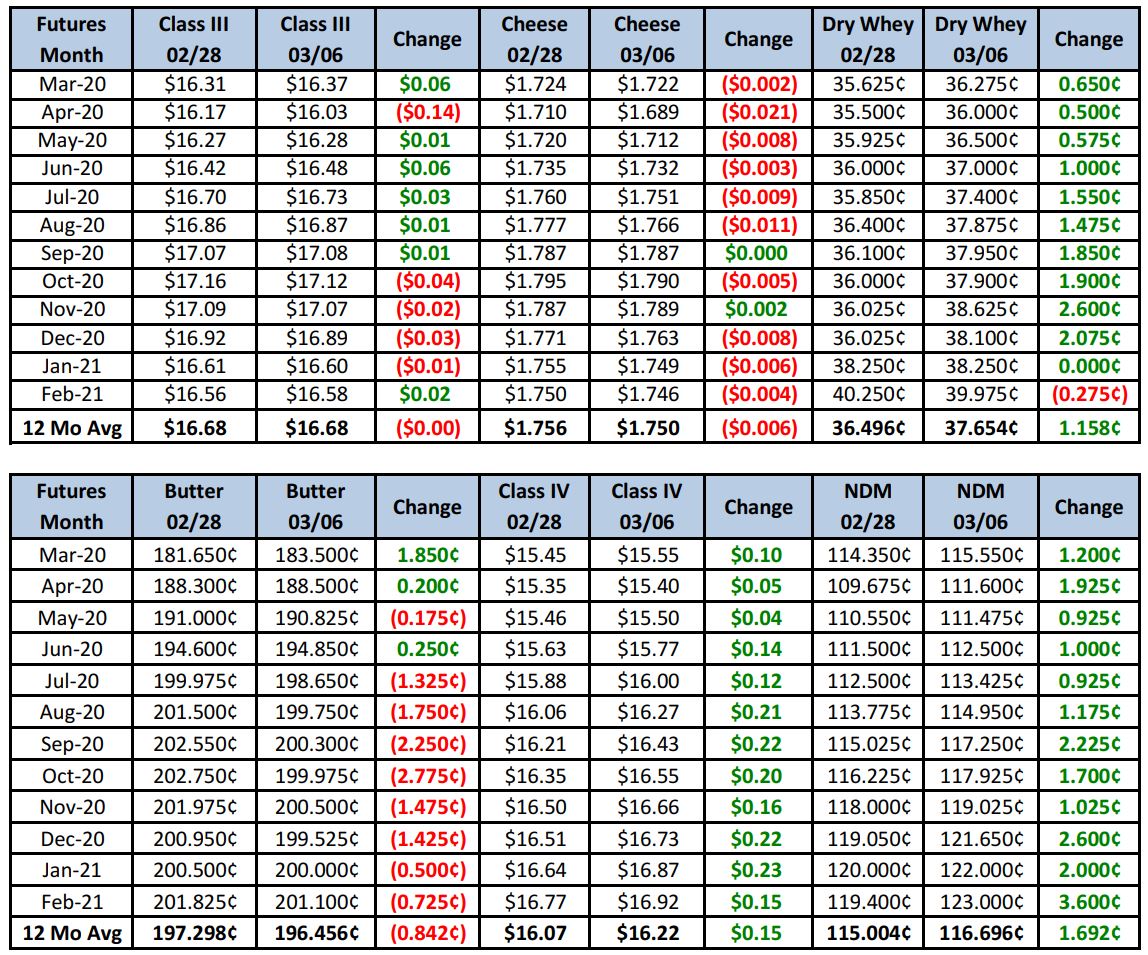

Futures Recap

Milk output in the Northeast continues to make weekly gains, according to Dairy Market News. Volumes are now heavy and balancing plants are receiving more loads, much of that into Class III manufacturing. Production is up slightly in the Mid-Atlantic, with processors there running at or close to capacity. In the Southeast, milk output is increasing, but most is going into Class I where sales have increased. Contacts in Florida say output is nearing its peak. Most farms in the Central region are reporting strong output, but cheese plants aren’t very interested in any spot loads as they have enough from internal sources. Heading West, output in California is abundant, surpassing expectations. Processors are running full, with some needing to find a home excess supply. Output in AZ is also higher as it heads into spring flush. Plants are taking discounted milk from out of state. Weather has been favorable in NM and the milk supply is plentiful. More milk is heading in to balancing plants this week than last. In the Pacific NW, milk production is heavy, with output in some areas above processing capacity. Heavily discounted spot loads are being reported, some for slightly more than freight, while some milk is being discarded. With all the milk currently being produced, there is also plenty of cream nationwide. Most butter plants are running at or near capacity, though a pickup in ice cream production is expected to help clear some of the current cream glut. The dry whey market has a steady tone, though coronavirus fears are hampering/delaying a previously bullish outlook. Supplies are generally available but not burdensome. However, international demands are starting to decline due to logistic issues. The same is true in the NDM market. Contacts had anticipated prices climbing, but the wild card remains the virus. That said, there are reports of many Q2 contracts being signed due to anticipation of a rapid price climb in the coming weeks. NE cheese makers say solid demand for soft type cheese is holding the cream market up. Without that, the heavy milk supplies would be an added weight to the market. Cheese plants continue to receive all the milk they can handle and cheese inventories are beginning to grow. Interest for specialty and aged cheeses is expected to pick up next month, and the overall feeling is that cheese prices will firm. Contacts in the Midwest report cheese sales are steady to slow. Barrel producers are attempting to limit output to just contracted obligations. The market sentiment in the region is quiet to bearish near term. Cheese output in the West remains active with the availability of low-cost milk. Domestic block sales have been increasing and some export sales are still moving. Current cheese prices are attracting more international buyers who want to take on more loads.

USDA released the Dairy Products Report this week. Cheddar cheese output in January was down 1.8% vs. a year ago, while total cheese output was up just 0.4%, both below expectations. Butter output in January increased just 0.6%, also below expectations. While those were price supportive to their respective markets, a 29.5% jump in January SMP output was decidedly bearish that market.

Overall, the coronavirus effect trumps all the data this week. The stock market continued to plummet despite solid economic data released this week. Until the spread slows, the disruption to spending patterns, travel, logistics and fear will continue. Producers should continue to prepare for a rebound with several strategies available:

- Buy call options against existing plant/futures contracts to cover potential upside risk July and beyond.

- Buy call options May-Aug and use them as “sell triggers” for any milk not yet marketed.

- Sell put options below the market to collect the premium and help offset DRP costs