10/29/2023

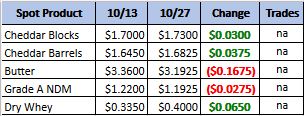

Spot prices have held steady the last couple of week as October comes to a close. The spot prices calculate out to a class 3 price of $17.12 and the last NDPSR comes in at $16.70. Both are bellow Novembers futures. Look for whey to rally to close that gap a little, but still need the buyers to step back into cheese to hit the futures prices.

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk output is increasing in the Northeast, and increased volumes are becoming available for Class III production. Milk availability in the Midwest has, reportedly, not edged lower much in recent weeks. Cheesemakers say Class III milk prices in the Midwest are higher than last year during the same period. In the West, contacts report strong to steady demand for Class III milk and say extra spot loads are somewhat limited. Cheese production is mostly steady in the West. In the Northeast, cheese production is increasing, but plants are

operating below capacity as labor shortages persist. Cheese inventories are said to be comfortable and growing in the region. Cheese inventories are comfortable in the West, though some manufacturers note spot availability is decreasing slightly. Midwest cheese inventories range from balanced to tighter, and demand is mixed from one plant to the other. Retail and food service demand for cheese is mostly steady in the West. In the Northeast, food service demand for mozzarella cheese is strong, and cheddar demand is reported as steady to stronger. (USDA Cheese Highlights)

Butter: Cream availability is increasing in the East and Central regions. Cream is tight in the West, and some butter makers in the region say current prices are causing them to limit their spot purchasing. Retail butter production is strong to steady in the West. Cream multiples are moving lower in the Central region, and butter makers are utilizing cream to run busier schedules. In the East, some processors say they are supplementing contracted loads of cream with spot orders to operate steady production schedules. Retail and food service demands are anticipated to remain steady through the holidays in the East. In the Central region, butter demand is mixed. Food service demand is strong to steady in the West, while retail demand is mixed. Stakeholders in the West say inventories are in good shape for the upcoming 2023 holiday demand. Butter inventories are steady in the East, while salted butter is somewhat tight in the Central region. (USDA Butter Highlights)

Dry Whey: Dry whey prices moved higher across all facets of the range and mostly price series. Activity from spot load buyers for nonpreferred brand loads is reportedly stronger. Both nonpreferred and preferred brand loads commanded some higher prices. A few manufacturers indicate tight inventories. Export demand is moderate. A few stakeholders relay sentiments that recent feed tenders from Asian purchasers and preparations for large yearly celebrations in Asia could garner more demand from Asian buyers. Dry whey production schedules are steady with cheese manufacturers making ample amounts of liquid whey. Market tones for dry whey are bullish. Some stakeholders note demand for proteins, in general, has improved (USDA Dry Whey)

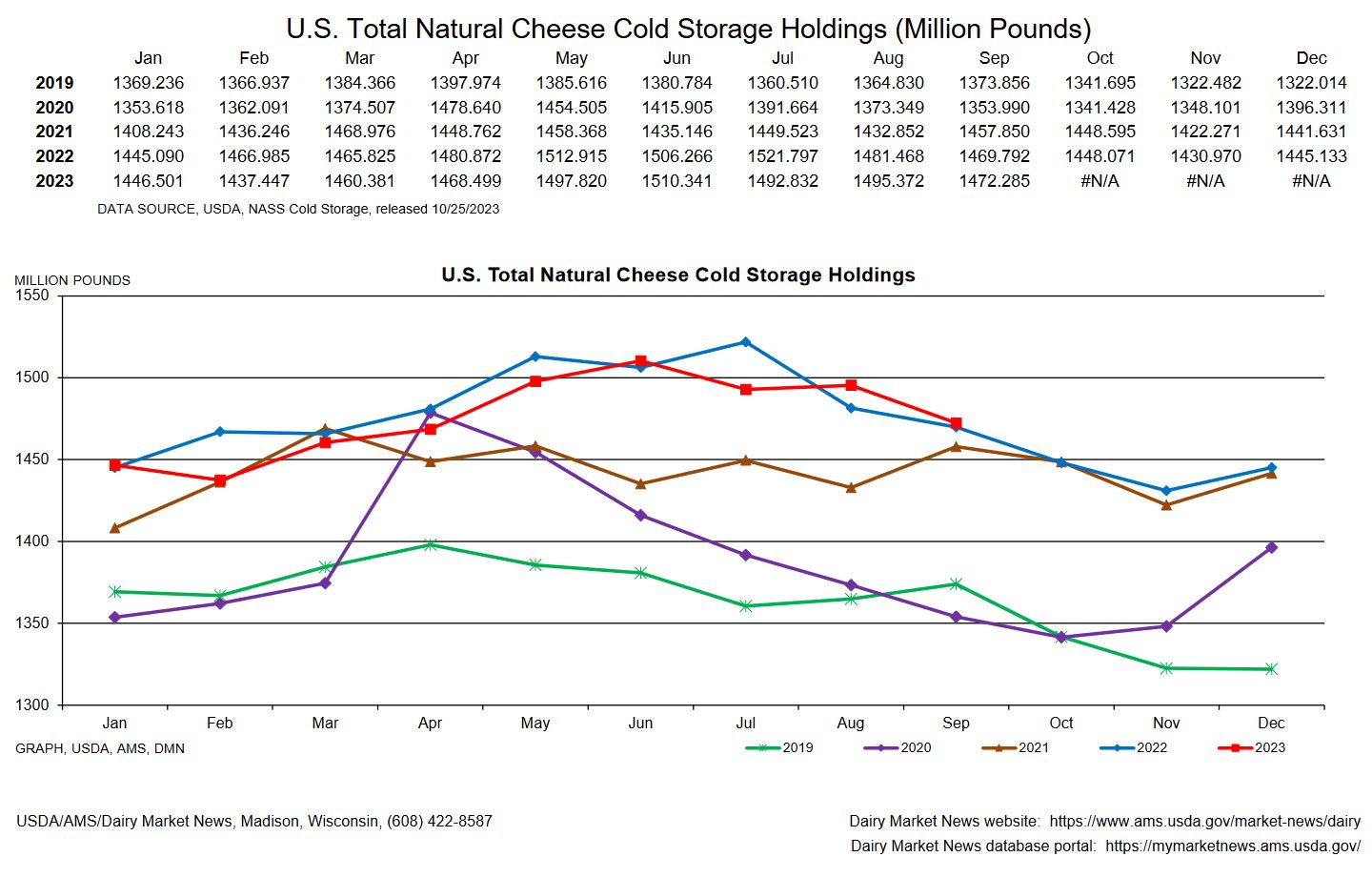

Cold storage was a mixed bag. If you look at the graph above there was a draw down from last month but it is also at the highest point for the last 5 years. That is with one of the hottest finishes to summer that we have had. Milk production is on the rise as the temperatures have dropped. Cull rate is down but with replacement heifers tight, and producers still breading toward beef, the dairy herd is unlikely to grow. Recommendation, put spreads tight to the market. Look to collect the first dollar drop as the current prices are close to cost of production. If there is a rally look to roll the puts higher still leaving the upside open.