5/6/2023

I am starting to feel like a broken record, but we continue to have an abundance of milk. With large discounts on spot loads of milk cheese continues to be brought to the CME. 65 loads of cheese were sold this week and 54 loads of dry whey. That is pretty high volume for the CME on class 3. Without a large drop in cow numbers it is going to take some heat this summer to finally tighten the milk availability for class 3 processing.

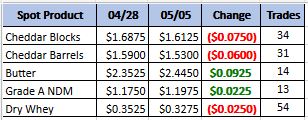

Weekly Spot Prices

Weekly Future Prices

Cheese: Cheese inventories range from tight to widely available in all regions, depending on cheese variety and end usage. There are ample amounts of milk for Class III processing throughout the regions, as spot milk prices range from $11 to $4 under Class III in the upper Midwest. To compare, last year during week 18, spot milk prices ranged from $3 under to $.50 over Class. As inflation has affected restaurant patronage, some cheesemakers who supply that sector of food service say demand has been slower in recent weeks, namely pizza style cheesemakers. Generally, cheese market tones remain under some bearish pressure. (USDA Cheese Highlights)

Butter: Plenty of cream is available for butter churning. Some eastern and western plants are running full production schedules to keep available cream volumes balanced. Butter manufacturing is busy overall, and inventories are growing in the East. Retail demand is firm throughout the country, and volumes are channeling steadily into contracted sales. Industry sources note that food service demand is less active in the East, while export demand from Canadian purchasers is more active in the West. There are upticks in salted butter demand in the West. This has prompted some manufacturers to shift production schedules from unsalted to salted butter production. Reported cream multiples are, for the most part, unchanged from previous weeks, as more Midwestern multiples into Class IV processing are in the low/mid 1.20s. Bulk butter overages range from 0 to 10 cents above market, across all regions. (USDA Butter Highlights)

Dry whey: Dry whey prices have moved lower across the range and mostly price series this week. The spot market had moderate activity. Although slower paces for Q2 booking are reported by some stakeholders, contract sales are steady. Loads are available to accommodate current spot market and contract sale demand. The latest price on the CME for dry whey is $0.3275, which represents a decrease of 2.5 cents since last week. Some manufacturers keep production schedules shifted into dry whey from high whey protein concentrates. Industry sources note pricing at the end user level and overall demand for high whey protein concentrates is contributing to the production shifts by a few manufacturers. Strong production schedules by cheese producers are leaving plenty of liquid whey available for drying. Market tones are neutral to slightly bearish. (USDA Dry Whey updates)

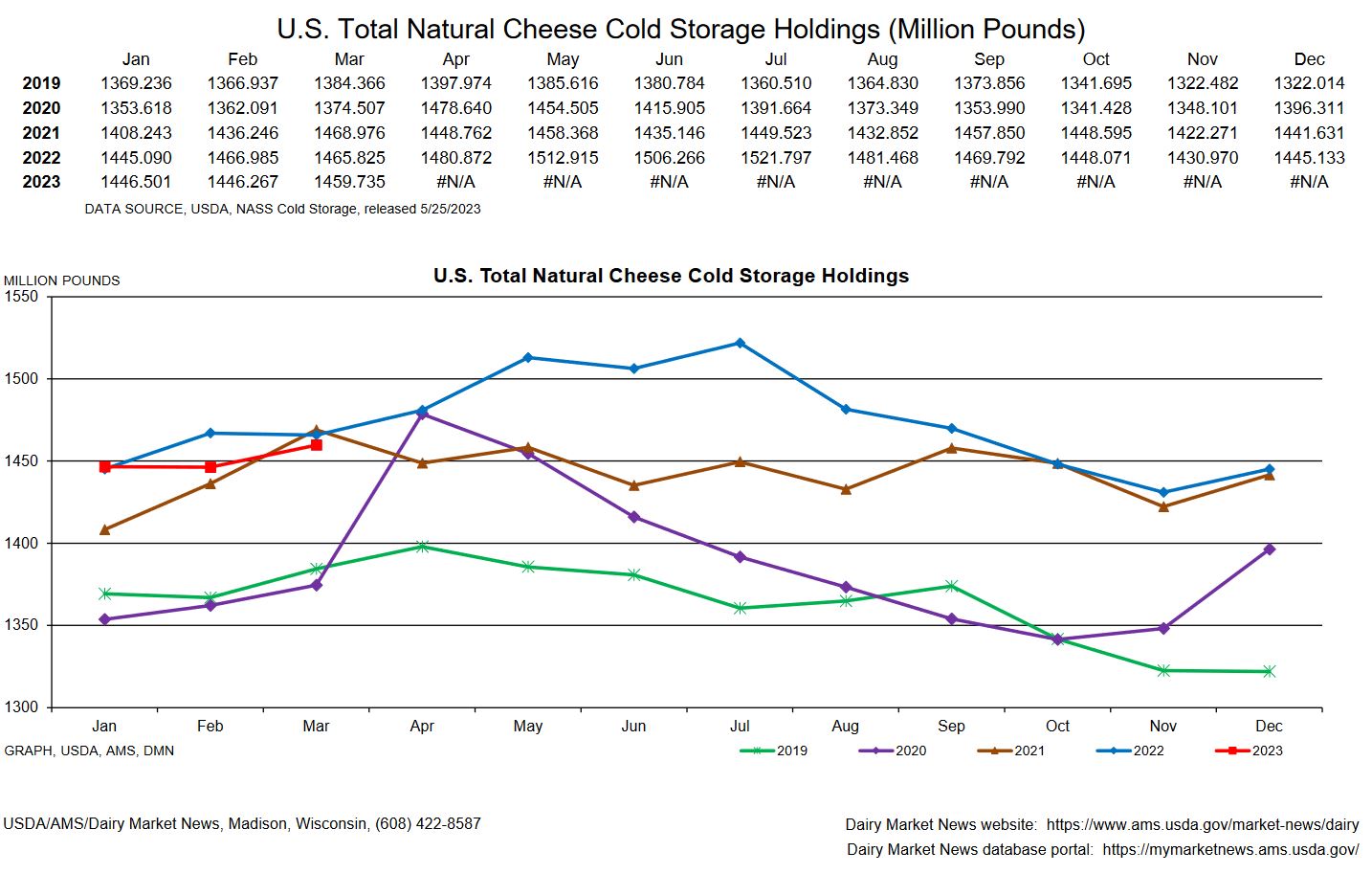

Cheddar cheese in cold storage notched closer to last year in March and looking at the weekly number for april it will continue to increase. That is not usual for this time of as 3 of the last 4 years it did increase in April. The bearish tone for class 3 is going to remain until milk production slows, which should happen when some heat moves into the Midwest. Look for July or August to be a tipping point for milk production and it may take that long for prices to rebound. Recommendation: for new coverage look at puts or put spreads; June to August 2023 buy at the market puts sell a dollar lower put for 35 cents, or step into the trade shooting for 10 to 15 cents.