1/23/2022

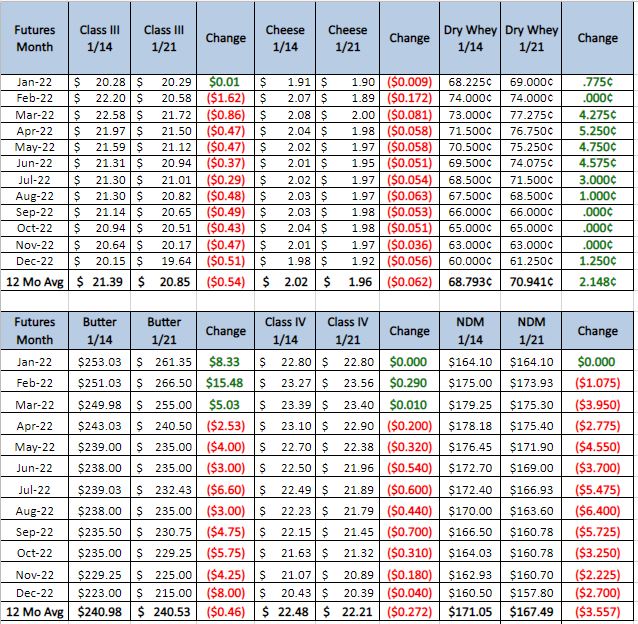

Big sell off in cash this week but class 3 futures are holding on. We were down 11 and 14 cents on blocks and barrels this week, while the price on February drop at the same rate the rest of the months had a more muted response. This shows a strong buy side to this market and any kind of strength in cash is likely to push the market back higher.

Weekly Spot Prices

Weekly Future Prices

Cheese: Milk availability continues to vary for cheese producers from region to region and plant to plant, but current reports do not show a tight milk market, at least right now. Spot milk prices ranged from $1 to $.50 under Class, while last year’s range during this week was $8.50 to $4 under Class. Retail cheese demand has quieted in the Western region, while international demand remains strong. Eastern contacts say retail demand is steady/strong during football’s playoff season. Staffing shortages continue to plague plant managers, with plant workers, but also with drivers and office employees. Cheese market tones are wavering. Last week’s barrel price bullishness met and lost to bears this week.

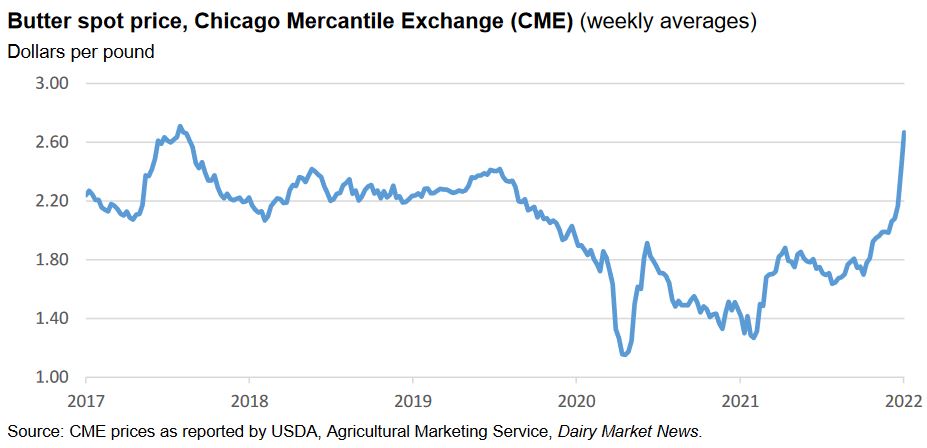

Butter: Cream supplies are available to butter makers. Some loads are traveling from the West to the Midwest. However, high freight costs, driver shortages, and inclement weather are reportedly posing some challenges to moving cream. Cream demand is firm, and butter production is active. Some Eastern manufacturers are increasing production and churning seven days a week to bulk up shrinking inventories. Microfixing is active to satisfy good retail print butter demand. In the West, operations at some butter plants are limited by labor issues and delayed production supply deliveries. Butter inventories are tight, and spot purchasers report salted is still easier to source than unsalted. Butter demand is strong in domestic and international markets. Bulk butter overages range from 8 to 19 cents above market throughout the country.

Dry whey price movements were subdued this week. The bottom of the dry whey price range increased, while the top was unchanged. Mostly there was upward movement on both ends of the range. Demand for dry whey is trending higher in domestic markets, while international demand has declined. Dry whey spot inventories are mixed. Some contacts say that that declining international demand has increased load availability, while others report that inventories are tight. Port congestion and a shortage of truck drivers are causing delays to load deliveries. Dry whey production is steady to lower. Contacts report that some drying operations are running reduced schedules due to delayed deliveries of production supplies, and labor shortages. Plant managers are focusing their schedules on higher whey protein concentrates and permeate, further limiting dry whey production.

Cracks in the class 3 bull market starting to show, but class 4 is still heading higher. With the export market still showing strength pull backs are going to be muted. With that said these prices are at multi year highs and therefore still can fall from where they are at. Recommendation this week for class 3 hedging is put spreads with selling a call. Buy at the money Put sell a Put 2 dollars lower sell the $23 call. Example April 2022 buy 2150 Put sell 1950 Put sell 2300 call, spend up to 20 cent to get it done. As always give us a call to get a more personalized hedge plan.