03/22/2019

Futures Recap

| Futures Month | Class III 03/15 | Class III 03/22 | Change | Cheese 03/15 | Cheese 03/22 | Change | Dry Whey 03/15 | Dry Whey 03/22 | Change |

| Mar-19 | $14.94 | $15.03 | $0.09 | $1.533 | $1.540 | $0.007 | 40.025¢ | 40.900¢ | 0.875¢ |

| Apr-19 | $14.88 | $15.29 | $0.41 | $1.539 | $1.586 | $0.047 | 38.275¢ | 37.675¢ | (0.600¢) |

| May-19 | $15.11 | $15.39 | $0.28 | $1.561 | $1.595 | $0.034 | 38.500¢ | 37.400¢ | (1.100¢) |

| Jun-19 | $15.44 | $15.58 | $0.14 | $1.600 | $1.610 | $0.010 | 37.750¢ | 36.900¢ | (0.850¢) |

| Jul-19 | $15.92 | $15.96 | $0.04 | $1.645 | $1.658 | $0.013 | 38.200¢ | 37.000¢ | (1.200¢) |

| Aug-19 | $16.15 | $16.13 | ($0.02) | $1.675 | $1.670 | ($0.005) | 38.025¢ | 37.300¢ | (0.725¢) |

| Sep-19 | $16.39 | $16.39 | $0.00 | $1.686 | $1.695 | $0.009 | 38.500¢ | 38.000¢ | (0.500¢) |

| Oct-19 | $16.35 | $16.34 | ($0.01) | $1.690 | $1.695 | $0.005 | 39.000¢ | 38.000¢ | (1.000¢) |

| Nov-19 | $16.24 | $16.28 | $0.04 | $1.676 | $1.682 | $0.006 | 39.000¢ | 38.000¢ | (1.000¢) |

| Dec-19 | $16.10 | $16.12 | $0.02 | $1.666 | $1.672 | $0.006 | 38.925¢ | 38.000¢ | (0.925¢) |

| Jan-20 | $15.81 | $15.80 | ($0.01) | $1.654 | $1.654 | $0.000 | 37.375¢ | 37.375¢ | 0.000¢ |

| Feb-20 | $15.75 | $15.78 | $0.03 | $1.657 | $1.658 | $0.001 | 38.000¢ | 38.000¢ | 0.000¢ |

| 12 Mo Avg | $15.76 | $15.84 | $0.08 | $1.632 | $1.643 | $0.011 | 38.465¢ | 37.879¢ | (0.585¢) |

| Futures Month | Butter 03/15 | Butter 03/22 | Change | Class IV 03/15 | Class IV 03/22 | Change | NDM 03/15 | NDM 03/22 | Change |

| Mar-19 | 227.525¢ | 227.625¢ | 0.100¢ | $15.79 | $15.79 | $0.00 | 96.825¢ | 96.100¢ | (0.725¢) |

| Apr-19 | 228.200¢ | 228.275¢ | 0.075¢ | $15.88 | $15.84 | ($0.04) | 97.100¢ | 96.250¢ | (0.850¢) |

| May-19 | 230.725¢ | 231.025¢ | 0.300¢ | $15.96 | $15.97 | $0.01 | 97.975¢ | 97.150¢ | (0.825¢) |

| Jun-19 | 231.775¢ | 233.700¢ | 1.925¢ | $16.27 | $16.19 | ($0.08) | 100.250¢ | 98.775¢ | (1.475¢) |

| Jul-19 | 232.775¢ | 234.900¢ | 2.125¢ | $16.48 | $16.42 | ($0.06) | 102.000¢ | 100.575¢ | (1.425¢) |

| Aug-19 | 233.000¢ | 235.700¢ | 2.700¢ | $16.64 | $16.62 | ($0.02) | 104.250¢ | 102.000¢ | (2.250¢) |

| Sep-19 | 232.925¢ | 235.150¢ | 2.225¢ | $16.75 | $16.68 | ($0.07) | 105.000¢ | 103.325¢ | (1.675¢) |

| Oct-19 | 231.800¢ | 233.550¢ | 1.750¢ | $16.72 | $16.72 | $0.00 | 106.025¢ | 104.300¢ | (1.725¢) |

| Nov-19 | 231.000¢ | 231.625¢ | 0.625¢ | $16.75 | $16.72 | ($0.03) | 106.800¢ | 105.400¢ | (1.400¢) |

| Dec-19 | 227.525¢ | 228.900¢ | 1.375¢ | $16.64 | $16.64 | $0.00 | 106.900¢ | 105.775¢ | (1.125¢) |

| Jan-20 | 225.000¢ | 223.000¢ | (2.000¢) | $16.55 | $16.55 | $0.00 | 108.425¢ | 107.800¢ | (0.625¢) |

| Feb-20 | 222.525¢ | 223.000¢ | 0.475¢ | $16.55 | $16.55 | $0.00 | 109.250¢ | 108.425¢ | (0.825¢) |

| 12 Mo Avg | 229.565¢ | 230.538¢ | 0.973¢ | $16.42 | $16.39 | ($0.02) | 103.400¢ | 102.156¢ | (1.244¢) |

Spot Market Recap

| Spot Product | 3/15 | 3/22 | Change |

| Cheddar Blocks | $1.5600 | $1.5700 | $0.0100 |

| Cheddar Barrels | $1.4925 | $1.5650 | $0.0725 |

| Butter | $2.2800 | $2.2650 | ($0.0150) |

| Grade A NDM | $0.9675 | $0.9575 | ($0.0100) |

| Dry Whey | $0.3200 | $0.3300 | $0.0100 |

Spot Market Trade Volume

Fluid Milk Output

Milk production continues to increase in the Northeast, but some contacts report output is down slightly from a year ago. Most processors are receiving the milk they need, but others are not at capacity. Mid-Atlantic milk output is also increasing seasonally, with a few operations there as well that are running under capacity. The Southeast is seeing incremental gains in milk production and is generally in balance with demand. Florida output has leveled off, and with stronger than expected Class I sales, no milk is leaving the state. Cream is available but is beginning to tighten up, while demand is increasing. Flooding is a concern in the Central region; everything from planting delays and future feed availability, to building/barn damage. Some milk handlers report a slippage in milk receipts vs. last year at this time. Ongoing farm closures heading in to the end of March and into the spring are all but assured to happen, giving processors some concern over their milk supply heading in to summer. Cream availability is tightening as ice cream production is slowly starting to pick up. California milk output continues to inch higher, keeping manufacturers busy and dryers running full schedules. Intakes are equal to year-ago levels. The same is true in Arizona, where better weather is allowing milk supplies to fulfill all end user needs. Milk production in New Mexico is generally flat, and Class II and III sales are up. Milk production is rebounding in the Pacific Northwest and most processing facilities have plenty of milk. Plants are near full capacity, though a few are reporting intakes are off a bit due to herd dispersal sales. As strong as milk output is, discounted milk loads are not widely available.

Butter

Churns are active in the East as both salted and unsalted butter is being produced. Inventories are growing but are destined for summer and fall use. Cream supplies appear to be tightening up a bit as Class II demand improves and holiday orders are being received. Butter output has slowed in the Midwest as supplies are nearing sufficient levels to spring demand. Butter sales are improving ahead of the holidays, and manufacturers expect cream supplies to tighten in the near future. Butter inventories remain manageable in the West, as stocks in warehouses haven’t built up as much as usual. Orders for both bulk and retail are strong, and food service requests for butter have improved. Ice cream production is expected to ramp up in the coming weeks, so butter makers are securing what cream they can to assure they will have adequate supplies for future use.

Dry Whey

Stocks are stable in the East, but both domestic and international sales are lower. Many buyers are waiting for lower prices before making additional purchases, however. In the Central region, prices slid lower this week, but sellers are attempting to hold prices by hanging on to their inventories. Output is beginning to increase, however, and the swine flue issue in Asia continues to put a drag on the market. Western dry whey export sales are below expectations as reduced demand from Mexico and Southeast Asia have pressured prices lower. Inventories are not burdensome yet, but there is concern that supplies could grow beyond desired as the region heads in to spring flush.

Nonfat Dry Milk

The NDM market is weak in the East as there is lower interest from both purchasers and end users. Manufacturers have plenty to offer and are actively seeking buyers. Some Central region bulk loads were found at discounts this week, though trading was slow. End users are finding deals, but some contacts suggest the bottom is near, with Mexican buying expected to pick up soon. Out West, the NDM supply is above current demand. Some processors expect the market to see improved demand soon, especially from the baking sector. Some are holding stocks, expecting to sell at a higher price later in Q2.

Cheese

Cheese output is active in the Northeast, but some contacts report milk output is down from a year ago. Supplies are stable to growing and keeping pace with demand. Spot prices of milk in the Central region can still be had for as low as $2 under Class III, but that may not last. Multiple reports of shuttering no later than this spring are coming to light, though milk is still expected to remain plentiful through the flush. Cheese demand reports are more positive this week, with both curd and barrel sales reporting upticks. The market tone continues to improve. In the West, demand is steady, but new business has been slow to develop. However, cheese prices are supported and the heavy inventories do not seem to be a major concern for processors. Demand is keeping pace with current production, and processors are hopeful that basketball tournaments and grilling season will soon improve demand even further.

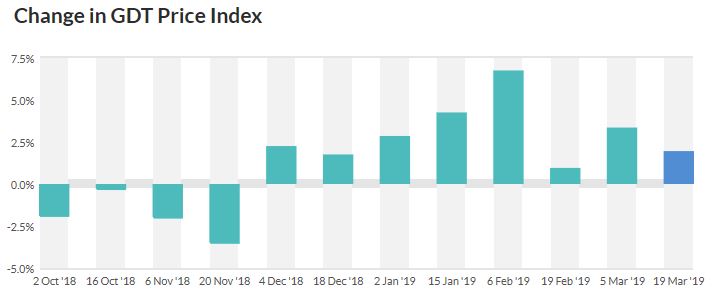

International

This week’s GDT auction saw the Dairy Price Index increase 1.9%. The index has moved higher with every auction since December 4th. Gains were led by butter up 9.3% to a U.S. equivalent$2.31/lb and cheddar cheese, up 3.9% to a U.S. equivalent$1.83/lb.

Source: Global Dairy Trade

Commentary

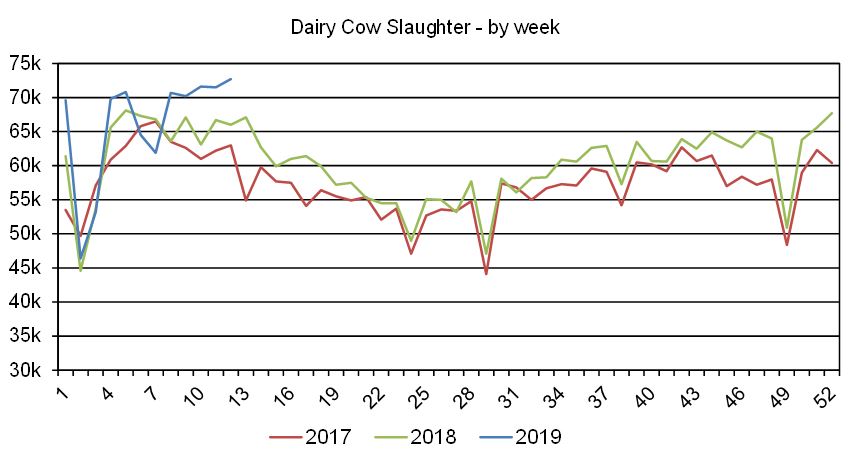

A lot of factors are starting to swing towards a more bullish outlook. This week’s dairy cow slaughter totaled 72,700 head, up 10.15% (6,700 head) vs. the same week a year ago, and the highest weekly total in more than 12 years.

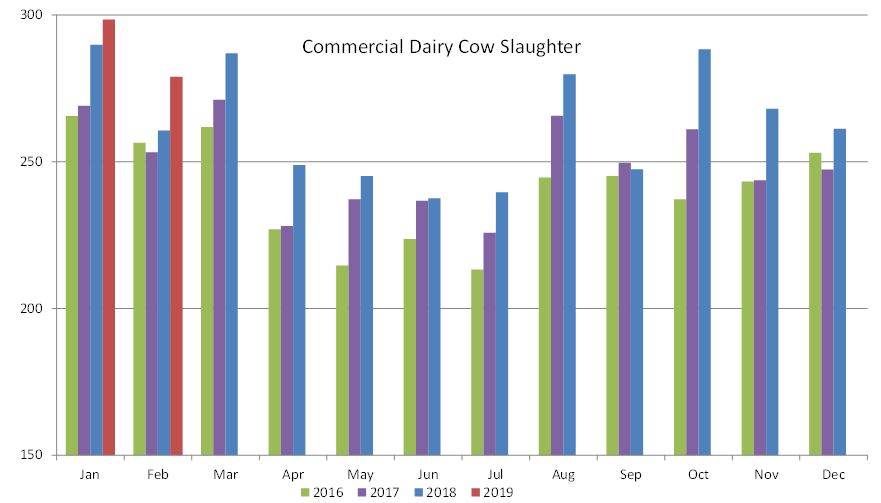

A monthly Livestock Slaughter Report was released this week. 278,900 dairy cows were removed from the herd, up a strong 7% (18,300 head) and the highest Feb total since before 2006.

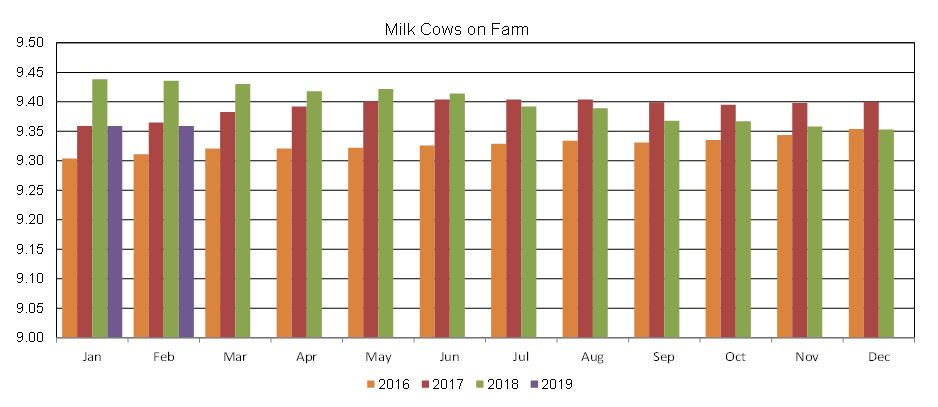

USDA caught up after the government shutdown, releasing the Milk Production Report. February output increased just 0.25%. Cow numbers were flat vs. Jan at 9.359 million head.

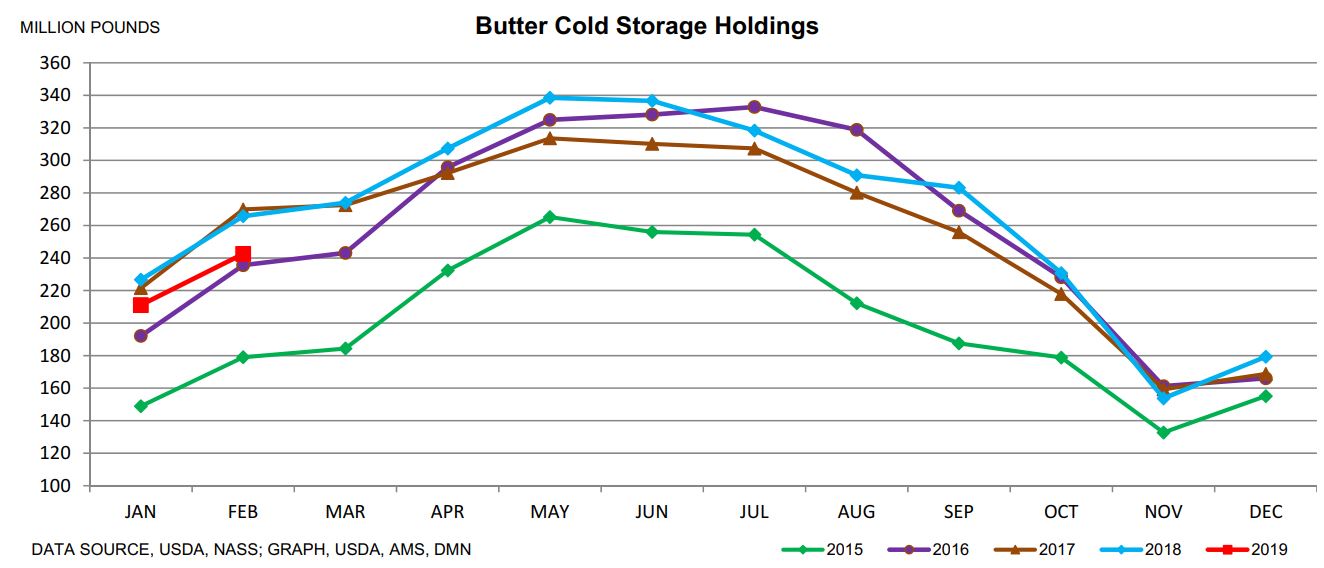

Finally, the Cold Storage Report was released today, just after the close. Sunday evening’s open could be interesting as there were several surprises. Butter stocks at the end of February were down 9% vs. a year ago, and increased less than expected from January.

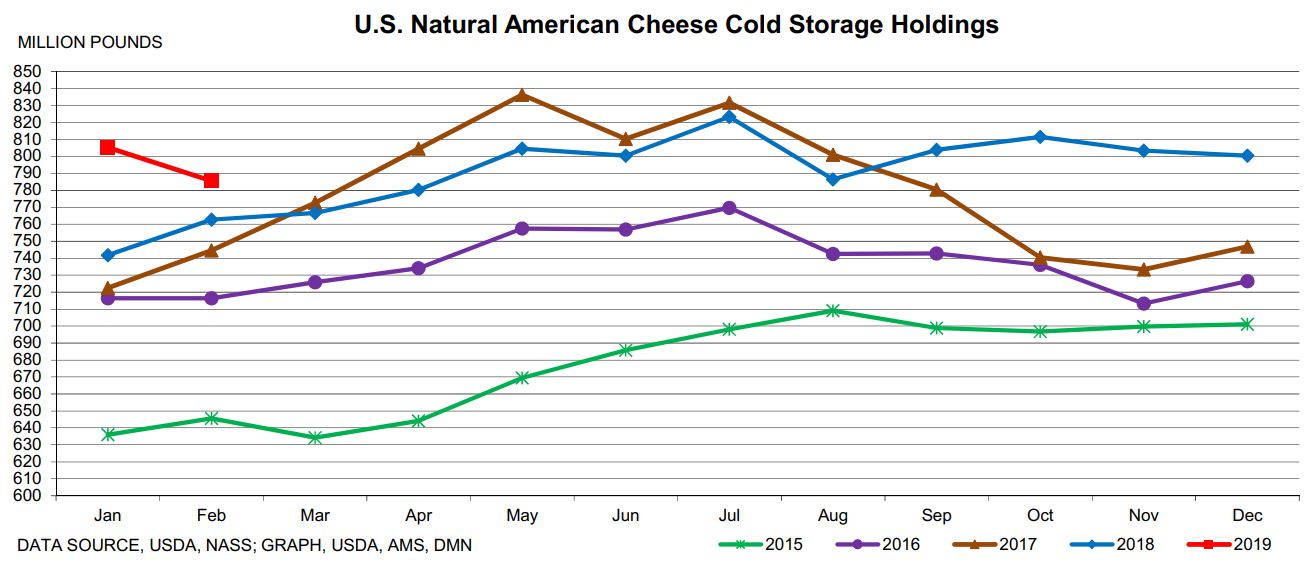

Secondly, American cheese stocks were up just 3% vs. Feb 2018, and declined anti-seasonally by 2% vs. Jan.

Weekly cold storage numbers indicate demand has continued to be good in March, with cheese stocks at USDA-selected storage centers down a further 3% (2.8 million lbs) over the period 03/01 through 03/11. With strong weekly slaughter numbers so far this month, we would not be surprised to see a negative number in next month’s Milk Production Report.

Last week we were scratching our head as to the price action in April. This week saw a substantial increase as spot cheese traded into new highs for the year. Grilling season is around the corner in many parts of the country, which may be why the barrel price was able to gain so much ground. The spread between blocks has narrowed to just 1½¢. Thought spring flush is still ahead of us, the prospect of improved demand and an uncertain milk supply leading in to summer has set the stage for higher prices. The surprise in the Cold Storage numbers and a Milk Production Report ready to flip negative should have dairy product end users hedging their upside risk if they haven’t already. That should bring more buyers into the market next week. Flooding over much of the grain belt has the potential to delay planting. Grains continue to find support, thus feed costs will not be going down. Despite Class III futures and the spot market finishing off their highs of the week, we believe it’s a temporary setback. Dairy operations that have fixed contracts should more urgently attempt to protect against higher prices if they are able, to open those contracts up to a potential rally.